Offshore expertise keeps this company solid in a volatile market

In today’s fluctuating oil and gas market, rating agencies often look closely at these companies.

This sector, known for its ups and downs, always gets extra attention.

Companies face challenges with changing oil prices, which can be affected by things like international politics, new rules, and how well the world’s economy is doing. These changes can make a big difference in their credit ratings.

Also, the oil and gas industry is known for its roller-coaster-like pattern of highs and lows, which doesn’t help in easing the worries of rating agencies.

Offshore drilling adds another layer of complexity to this, making it tougher for those who evaluate a company’s creditworthiness.

Noble Corporation (NE) is right in the middle of all this. They focus on offshore drilling, which is a challenging part of a market that goes through a lot of changes.

Today, we’re going to explore Noble Corporation using Uniform Accounting to determine if the caution shown by rating agencies is justified or not.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The oil and gas exploration and production industry, particularly in the realm of offshore drilling, is an area that often draws close examination from rating agencies.

This sector is marked by its cyclical nature due to varying global demand and supply, geopolitical factors, and regulatory shifts, leading to notable price changes.

Such cyclical patterns can lead to inconsistent earnings for companies in this field, which tends to worry credit evaluators who prefer predictable cash flows to ensure debts are managed properly.

Offshore drilling contracts, often large-scale and long-term in nature, add another layer of complexity.

These contracts are typically awarded through competitive bidding processes and involve detailed operational and financial planning due to the significant investment and time required.

In this context, Noble Corporation (NE) stands out as a significant player. As one of the largest offshore drilling contractors in the United States, Noble Corporation has established a strong foothold in this challenging environment.

However, rating agencies often view the company through a lens of caution due to the industry’s cyclicality. And right now, oil prices are struggling. They’re down more than 13% since the beginning of November.

Unlike many of its competitors, Noble Corporation has a robust portfolio of drilling contracts and a record of operational excellence in offshore drilling.

The company benefits from long-term contracts that provide a more stable revenue stream, even in an industry known for its fluctuations.

This stability is crucial, especially when considering the high operational costs and investment risks associated with offshore drilling projects.

Moreover, Noble Corporation’s operational strategy in managing these projects is noteworthy.

It involves detailed planning and execution, ensuring efficiency and cost-effectiveness. This approach not only mitigates the risks associated with offshore drilling, but also positions the company to capitalize on market opportunities when they arise.

Despite these strengths, rating agencies often categorize Noble Corporation as an average risk entity, focusing on the industry’s inherent cyclicality.

They may not fully recognize how Noble Corporation’s strategic approach to offshore drilling and contract management sets it apart from typical exploration and production companies.

Thus, S&P has given Noble Corporation a “B+” credit rating. This rating suggests there’s about 24% the company might not be able to pay its debts in the next five years, which places it in a category of higher risk.

When we look at how well Noble Corporation runs its business and its current financial health, we think it should be seen as much less risky.

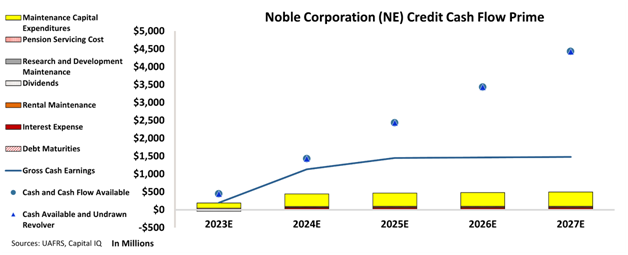

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Noble Corporation’s cash flows are more than enough to serve all its obligations going forward.

The chart shows that the company is in a firm financial ground and will be able to satisfy its obligations in the near future.

Remarkably, the company has no debt maturities going forward. Thanks to its strong cash flow, the company could manage its debts without trouble, if it had any.

Additionally, the company’s proven business approach is set up to boost its profits through its stable offshore drilling contracts.

That’s why we think that Noble Corporation deserves a much safer credit rating.

Here at Valens, we’ve assigned the company an “IG4” rating. This rating places it in the safer investment category, with 2% risk of default.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Noble Corporation (NE:USA) Tearsheet

As the Uniform Accounting tearsheet for Noble Corporation (NE:USA) highlights, the Uniform P/E trades at 11.6x, which is below the global corporate average of 18.4x, but above its historical P/E of -69.7x.

Low P/Es require low EPS growth to sustain them. In the case of Noble Corporation, the company has recently shown a 148% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Noble Corporation’s Wall Street analyst-driven forecast is for a 1027% EPS growth and a 68% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Noble Corporation’s $46 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was below the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance.

Overall, this signals a low dividend risk.

Lastly, Noble Corporation’s Uniform earnings growth is above its peer averages, but is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research