A safer credit rating is a fair game for this business model

Rating agencies are frequently cautious when analyzing companies in volatile markets, particularly those involved in acquisitions due to the uncertainty these factors introduce into financial stability and growth expectations.

The oil and gas industry, which is notorious for its volatility, is typically on the receiving end of this cautious approach.

Companies in this sector bear the brunt of pricing fluctuations caused by geopolitical tensions, regulatory changes, and global economic health, which affect their credit ratings.

Furthermore, the cyclical returns that are characteristic with this industry do little to alleviate rating agencies’ concerns. Acquisitions merely increase the perceived risk, painting a less-than-favorable image for credit evaluators.

This cautious narrative by rating agencies includes Northern Oil & Gas (NOG), a business aggressively engaged in acquisitions in a sector noted for its cyclical character.

Today, we’ll examine the credit risk profile of Northern Oil & Gas using Uniform Accounting to determine whether rating agencies are overly wary of the company or not.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The cyclical nature of the oil & gas sector is often a subject of scrutiny by rating agencies. The fluctuating global demand and supply, geopolitical issues, and regulatory changes often lead to significant price volatility in this sector.

This cyclical behavior can result in inconsistent revenues for companies involved, making them less appealing to ratings agencies.

The unpredictability becomes a concern for credit evaluators, who prefer stable and predictable cash flows to ensure that debts will be serviced promptly.

In this landscape, Northern Oil & Gas (NOG) emerges as a notable player. It is a company that specializes in acquiring leasing and funding drilling opportunities.

Its involvement in acquisitions in a sector known for its cyclical tendencies tends to raise eyebrows among ratings agencies.

However, these agencies might be missing out on some crucial points regarding the company’s business strategy. Unlike many of its peers, Northern Oil & Gas operates as a non-operated working interest franchise in prominent shale basins across the US.

This means that while the company holds financial interests in various drilling operations, it does not participate in the day-to-day operational management of these wells and rigs.

Instead, it partners with operators who manage the daily operations, which allows it to benefit from the revenues generated from these operations without incurring the operational costs and risks.

This business model is distinctive as the company doesn’t operate wells or rigs, which is the usual practice among oil and gas exploration and production (“E&P”) firms. Instead, it focuses on acquiring interests in these operations, which allows for a lean operational structure.

The effectiveness of this business model is underscored by other metrics such as the growth in the number of assets, and an increase in production over the years.

By focusing on acquiring interests, the company can rapidly scale its operations and benefit from the operational efficiencies of other established operators.

Its strategy has led to a diversified portfolio that spans across multiple geographic areas, thus spreading the inherent risks associated with each region.

Furthermore, the firm’s acquisition strategy isn’t just about expanding its portfolio; it’s about diversifying and mitigating risks associated with cyclical downturns.

By acquiring interests in different geographic areas and operations, it can spread out its risks and maintain a steady flow of revenue, even when some areas or operations are underperforming.

The overlooked aspect by rating agencies is that Northern Oil & Gas’ business model and acquisition strategy have placed it in a position where it better manages the cyclical nature of the industry than an average E&P company.

Nevertheless, rating agencies only classify it as an average risky player with cyclical returns.

That’s why S&P gives Northern Oil & Gas a “B” rating. This rating hints at a 24% chance of default over the next five years, putting the company in the high-risk category.

Considering its effective business model and present financial stability, we believe it warrants a substantially safer credit rating.

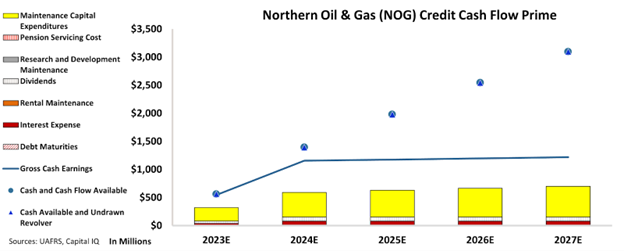

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Northern Oil & Gas’ cash flows are more than enough to serve all its obligations going forward.

The chart shows that the company is in a solid financial position and will be able to satisfy its obligations in the near future.

Notably, no debts are due within the next five years. The company’s massive cash flows allows it to easily handle any debts it may have.

Furthermore, the company’s well-established business model has the ability to increase earnings through the newly acquired firms.

In contrast to the rating agencies’ assessment, we believe Northern Oil & Gas has a minor risk of default.

As a result, we’ve assigned the company an “IG3+” rating. This rating places it in the safer investment category, with just 1% risk of default.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Northern Oil & Gas (NOG:USA) Tearsheet

As the Uniform Accounting tearsheet for Northern Oil & Gas (NOG:USA) highlights, the Uniform P/E trades at 9.1x, which is below the global corporate average of 18.4x, but above its historical P/E of -1.7x.

Low P/Es require low EPS growth to sustain them. In the case of Northern Oil & Gas, the company has recently shown a 473% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Northern Oil & Gas’ Wall Street analyst-driven forecast is for a 3% EPS growth and a 9% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Northern Oil & Gas’ $41 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 2x the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 210bps above the risk-free rate.

Overall, this signals a moderate credit risk risk.

Lastly, Northern Oil & Gas’ Uniform earnings growth is above its peer averages, but is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research