ServiceNow is automating the corporate world, but investors shouldn’t panic

When many people think of automation, they think of trends like robotic factories, computer aided design, or self-driving cars. While all of these are happening, the automation movement is also happening a lot closer to home.

Corporations are becoming more automated by the day, thanks to softwares by companies like ServiceNow. While some are scared this type of business automation will destroy jobs, companies are using it as a way to let workers focus on more value-add activities.

And yet, with such a valuable offering in place, Wall Street is under the impression that automation is a losing business to be in. Today, we’ll take a look at ServiceNow’s real financials to understand what Wall Street may be missing.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Workforce automation has been a long time coming. You’ve likely read articles about the most and least automatable jobs and worried that it was only a matter of years until a computer program could do your job for a fraction of the cost.

This has already started happening in factories thanks to companies like Brooks Automation (BRKS), but the truth is, automation is coming for us all. And yet, that might not be the bad thing you think it is.

Yes, some folks will be out of a job thanks to automation. The good news is, we have centuries of automation history behind us, and we still have jobs to do. Over time, we’ve been able to move our workforce into more value-add fields with each new wave of automation.

Consider when we had to hand-weave all of our fabrics or print each page of a book by hand. Now, there’s more time for fashion designers and writers to do what they do best.

Our factories have become more efficient and automatic, and that’s had the effect of moving people into office buildings. The services sector has never been bigger.

That said, as we mentioned, automation will eventually come for us all. The services sector is ripe for automation, and that’s exactly what ServiceNow (NOW) is accomplishing.

ServiceNow is at the core of the services automation movement, offering businesses tools like virtual help desks, automated IT solutions, and even streamlined accounting processes.

Over the last 10 years, ServiceNow has helped countless companies focus on what they do best, and as part of that, it has helped employees automate the drudgery in their workflows.

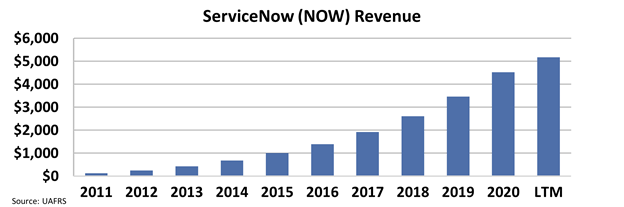

Automation can make or break businesses, and that’s why ServiceNow has grown exponentially since 2011. Revenues have grown roughly 50 times from just over $100 million to over $5.2 billion in the last 12 months.

Surprisingly though, looking at ServiceNow as an investment shows a completely different story.

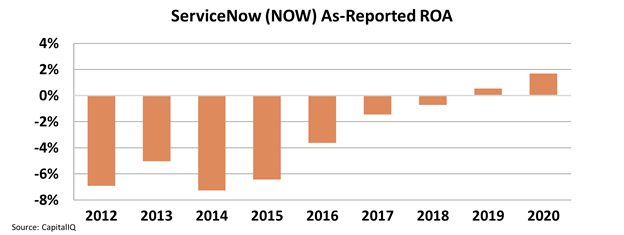

Despite its rapid growth, it looks like the company had to pay dearly to acquire all of its customers. On an as-reported basis, ServiceNow’s ROA was wildly negative until 2019, and it has only improved to 2%, well above cost-of-capital levels.

This type of return profile makes it look like the automation business is an unprofitable one. ServiceNow appears like it has unsustainably high customer acquisition costs and no differentiator to keep existing customers paying in the long-term.

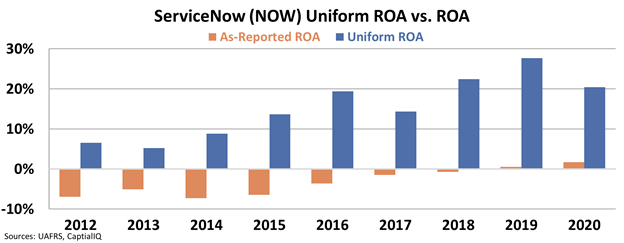

Yet, taking a deeper look with Uniform Accounting, it is clear the company’s true ROA has been comfortably above cost of capital levels since 2012, and as its services have grown more popular, so has its profitability.

ServiceNow’s Uniform ROA reached a peak of 28% in 2019 before pulling back slightly to 20% last year.

This is closer to what we’d expect for a company at the center of the corporate automation movement. With the exception of the pandemic year, the automation trend is clearly accelerating, and that trend carries over to ServiceNow’s profitability.

As companies continue working to make themselves more efficient, this is likely to continue in the future. While Uniform Accounting helps show how this trend translates into real profitability, investors stuck using as-reported metrics might miss the bigger point.

SUMMARY and ServiceNow, Inc. Tearsheet

As the Uniform Accounting tearsheet for ServiceNow, Inc. (NOW:USA) highlights, the Uniform P/E trades at 138.8x, which is above the global corporate average of 24.3x and its historical P/E of 98.9x.

High P/Es require high EPS growth to sustain them. In the case of ServiceNow, the company has recently shown a 22% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ServiceNow’s Wall Street analyst-driven forecast is for a 15% and 18% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ServiceNow’s $622 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 60% annually over the next three years. What Wall Street analysts expect for ServiceNow’s earnings growth is below what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power in 2020 is 3x the long-run corporate average. Moreover, cash flows and cash on hand are more than 3x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

Lastly, ServiceNow’s Uniform earnings growth is below peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research