This bigtime At-Home Revolution winner may be escaping the market’s attention once again

When the U.S. imposed lockdowns in mid-March 2020 to combat the rapid spread of COVID-19, many believed the recession that followed would be severely damaging.

Few seemed to understand that our credit system remained healthy, lowering the odds of a catastrophic recession, and many were surprised to see a rapid surge of spending in typically discretionary areas such as outdoor recreation, which tend to be hurt by economic downturns.

Nevertheless, one company we specifically highlighted back during the thick of lockdowns is still riding high on strong demand, even though the market seems to be pricing in a return to historical lows.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

On March 26, 2020, when much of the world was in a state of panic at the rapidly evolving COVID-19 situation, we here at Valens were already seeing an inkling of the brewing “At-Home Revolution.”

Our insight was guided by two factors.

The first was we could see that consumer balance sheets going into the crisis were much healthier than during normal recessions.

Aside from student debt, most metrics measuring household debt showed much lower levels than the heightened period leading up to the financial crisis of 2008.

Secondly, it was clear that the pandemic and related lockdowns were going to have a meaningful impact on how people spent their time and money.

We were so confident in our thesis that we highlighted a poster child for discretionary at-home spending to our clients, certainly not the kind of company you’d recommend heading into a normal recession with battered consumer spending.

In that Investor Essentials Daily back almost a year and a half ago, we pointed the spotlight on Polaris Inc. (PII), a leading manufacturer of motorcycles, snowmobiles, ATVs, and other off-road vehicles.

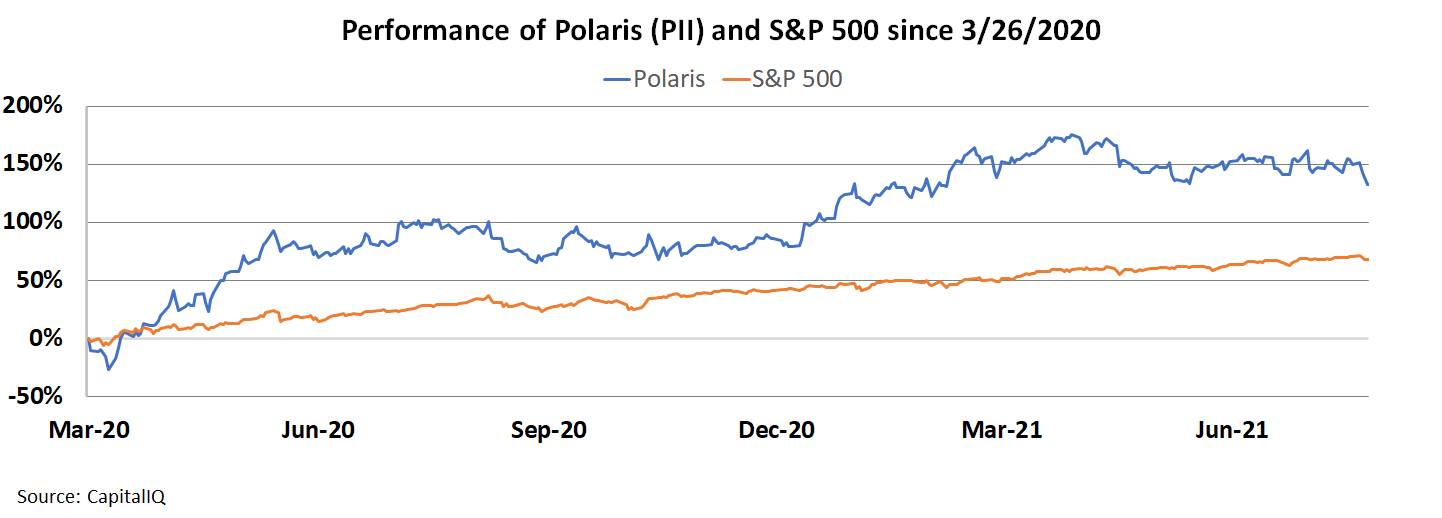

Since that recommendation, Polaris stock has risen nearly twice that of the S&P 500.

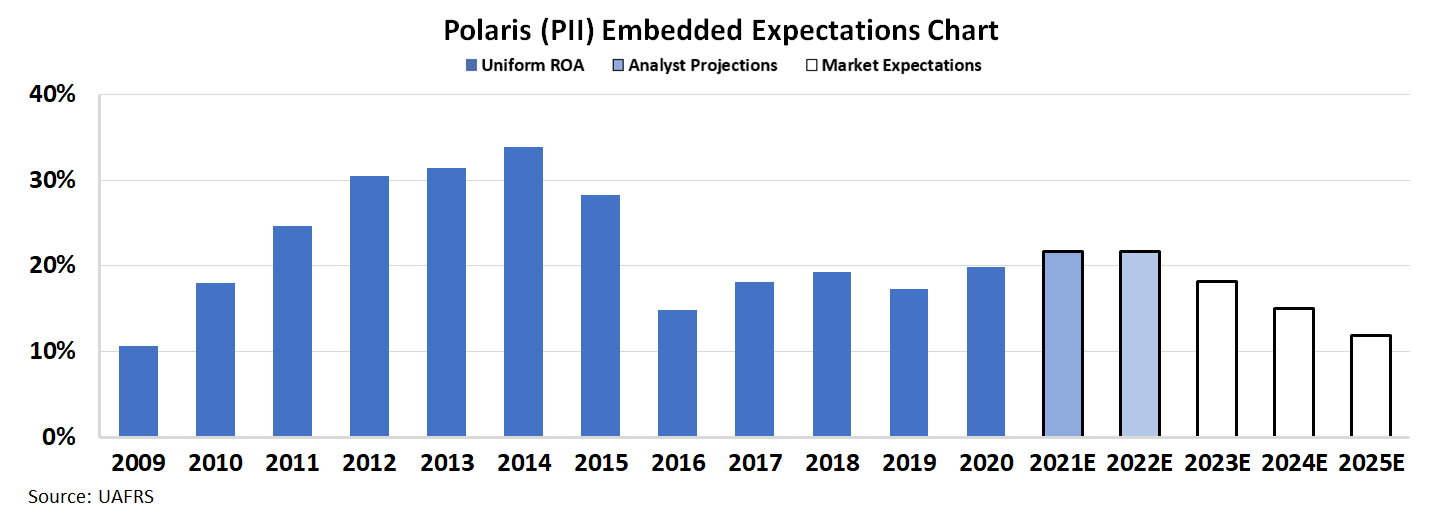

A big reason for our confidence last year was that after we looked through the accounting noise, we could see that the Embedded Expectations for the company’s return on assets (ROA) were far too pessimistic.

Considering the stellar run it has had, we thought it would be relevant to check back in to see what the Medina, Minnesota-based company’s valuation looks like today.

Once again, using our Uniform Accounting framework we can see that market expectations are currently for Uniform asset growth to remain around decade lows of 5% and Uniform ROA to fade to 13%, levels last seen in 2016 and 2009.

In the chart below, the dark blue bars represent Polaris’ historical corporate performance levels in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how the company’s ROA will shift over the next five years.

Considering the continued tailwinds this business enjoys in outdoor recreation, on the surface, it appears the market is being overly pessimistic.

With the possibility of the delta variant rearing its head, and continued demand for outdoor activities going into the winter, it looks like the At-Home Revolution still has some momentum to it a full year and a half later.

SUMMARY and Polaris Inc.

As the Uniform Accounting tearsheet for Polaris Inc. (PII:USA) highlights, the Uniform P/E trades at 12.5x, which is below the global corporate average of 23.7x but around its historical average of 12.7x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Polaris, the company has recently shown a 37% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Polaris’ Wall Street analyst-driven forecast is an EPS growth of 17% and 7% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Polaris’ $125 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 6% annually over the next three years. What Wall Street analysts expect for Polaris’ earnings growth is well above what the current stock market valuation requires through 2022.

Furthermore, Polaris’ earning power is 3x the corporate average. Also, cash flows and cash on hand are over 2x above its total obligations—including debt maturities, capex maintenance, and dividends. This signals a moderate credit and low dividend risk.

To conclude, Polaris’ Uniform earnings growth is below its peer averages and the company is trading in line with its peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research