This business serves sleepy people, but stays wide awake for its investors

Behind many of your favorite breakfast brands, massive conglomerates have been consolidating smaller brands into their fold.

But among them, one stands out. Let’s use Uniform Accounting to see what many investors will miss.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

It’s easy to think that just because an industry never makes the news, it must be sleepy and of little value to investors.

We at Valens beg to differ. The sleepy and boring businesses can often be interesting investment opportunities, thriving in the shadows, far from the threat of new incumbents, and enjoying age-old legacies.

Today, let’s take a look at the breakfast business.

The big brands are more or less entrenched, from Rice Krispies, Cheerios, Honey Bunches of Oats, and Raisin Bran for cereals, to Bob Evans for breakfast meats and Eggos for waffles.

One company, however, has been doing a great job at creating value underneath the top layer of brands we are all familiar with.

Since it was spun off from Ralcorp a decade ago, Post Holdings (POST) has been consolidating many of the brands we think of. These brands include half of those mentioned above, along with PowerBars, Raisin Bran, Barbara’s, and a dozen more.

Its niche is to sell products that are, in the company’s words, “ready to eat” and “ready to drink.”

This past Friday, we wrote about how railroad companies use consolidation to grow because, for them, organic growth into other regions is already dominated by other players, making it next to impossible.

Said otherwise, consolidation there is important because each individual company has an impenetrable economic moat.

But in the case of breakfast foods, it appears the exact opposite is true: aside from a certain degree of brand “stickiness,” the market is fragmented between hundreds of foodmakers, none of whom have a significant moat or share. This makes Post’s acquisitive movements all the more interesting.

In the world of Amazon (AMZN), Apple (AAPL), and Tesla (TSLA), organic growth is all the rage. But it is important not to discount acquisitive growth, which can also be lucrative if executed correctly.

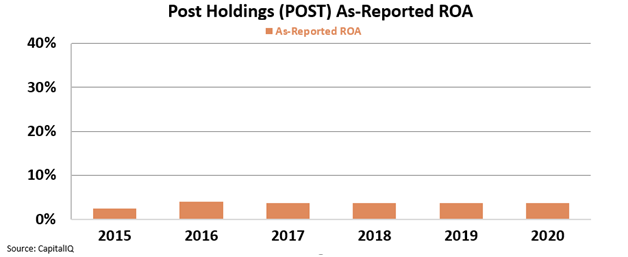

But if you looked at Post’s as-reported metrics, you’d wonder if they are doing it right. After rolling up all these brands, they are still only a 3%-4% ROA business, returning below the cost of capital. See for yourself:

This, however, is a total misrepresentation of how Post has leveraged the power of acquisitive growth.

Due to distortions inherent to the Generally Accepted Accounting Principles, or GAAP, which is the rulebook by which American companies report their financial results, earnings are often bled away by “expenses” that have little to do with a company’s true earning power. We correct for this, and dozens of other inconsistencies, to truly understand how companies earn.

Better yet, our framework is consistent across the board, enabling true apples-to-apples comparisons.

When you look at Post’s real profitability, the picture drastically changes. Not only is Uniform ROA far stronger than as-reported metrics suggest, but it is well above the U.S. corporate Uniform ROA average of 12%.

Take a look:

Post has been generating Uniform ROA in excess of 20% for the past 5 years. Thanks to bringing together multiple strong brands under one roof, it has been able to charge a premium for its high strength names.

Moreover, those who bet on Post five years ago would have been seeing mostly green as the stock price has doubled over that period. The same can’t be said for its stablemakes Kellogg Brands (K) and General Mills (GIS), which have been notably stagnant.

By consolidating good businesses, gaining more reach with retailers and more effectively managing costs, we see no reason for the Post victory lap to end.

But to unlock alpha, investors need to do more than just find companies with good strategic initiatives leading to strong ROA. They need to find companies that are strong but underappreciated by the market.

Each month, we assemble a list of the fifty best companies by quality, growth, and crucially, value. Hence, we call it the QGV 50, and it has handsomely outperformed the market for the past decade. Learn how to gain access here.

SUMMARY and Post Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for Post Holdings, Inc. (POST:USA) highlights, the Uniform P/E trades at 17.4x, which is below the global corporate average of 21.9x but around its own historical average of 16.6x.

Low P/Es require low EPS growth to sustain them. In the case of Post, the company has recently shown a 45% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Post’s Wall Street analyst-driven forecast is a 54% and 60% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Post’s $111 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 1% over the next three years. What Wall Street analysts expect for Post Holdings’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 4x the long-run corporate average. Moreover, cash flows and cash on hand are above its total obligations—including debt maturities and capex maintenance. However, intrinsic credit risk is 210bps above the risk-free rate.

All in all, this signals moderate credit risk.

To conclude, Post’s Uniform earnings growth is above its peer averages, but the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research