Rating agencies think this pool equipment maker is doomed in a recession

We have been mentioning the “At-Home Revolution” numerous times and how it has structurally changed people’s lives, economies, and policies.

One example would be the shift in our choice of homes. With the emergence of the pandemic, people started to move away from big cities to suburbs with the desire of living in bigger or more comfortable homes.

Most people started working remotely, shopped online, got online education, and suddenly, the need of living in big cities waned. This shift has benefitted many sectors and companies, and one of them was Hayward Holdings (HAYW).

However, credit rating agencies seem to be highly concerned with a possible recession in the near future and rate this company with a significant chance of bankruptcy.

Let’s have a look at the company under the Uniform Accounting framework and evaluate its credit risk to see if rating agencies should be as concerned as they already are.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The economic tides are turning fast. Back in 2021, we were experiencing economic euphoria. We saw that the pandemic didn’t really slow the economy down, and people got used to remote working.

That led to a ton of “At-Home Revolution” investments, where people upgraded their homes to be better living spaces. They got better workspaces, better security, and better entertainment.

A lot of people moved out of cities into the suburbs and beyond, and with that came a ton of investment in pools and related equipment.

That was great for Hayward Holdings (HAYW), which sells all kinds of parts for pool improvement and maintenance. The company’s profitability jumped from 30% return on assets (ROA) in 2019 to around 55% in 2020.

However, 2023 is shaping up to be quite different…

The housing market is slowing down, we are on the verge of a recession, and pools are probably the last thing on many people’s minds.

That has a lot of people, including the rating agencies, nervous for a company like Hayward.

They think it’ll have a possible credit risk, giving it a “BB” credit rating, which implies around a 10% chance of default.

But we can see that it’s not the case. 80% of the company’s sales are aftermarket, meaning upgrade and maintenance related tools and equipment.

That is why, the company’s revenues and profitability are not tied to new pool investments, as rating agencies think.

Aftermarket sales provide recurring revenue to the company, which helps its cash flows to be more stable.

Yet, rating agencies seem to be too concerned with the possibility of a recession and cannot see the picture clearly.

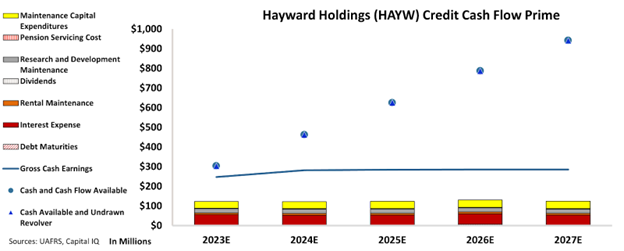

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart clearly shows that Hayward Holdings’ cash flows are more than enough to cover its obligations going forward.

CCFP chart indicates that the company does not have any concerning debt maturities in the next 5 years.

Additionally, we can see that the company could easily cover all its obligations with its cash earnings alone and that recurring revenues help Hayward to have stable cash flows going forward.

Taking these factors into account, there is no significant credit risk for the company. We think that Hayward deserves a much safer rating and should be placed among the investment grade basket.

That is why, we are giving an “IG3” rating to the company, which implies around a 1% chance of default.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click click to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Hayward Holdings (HAYW:USA) Tearsheet

As the Uniform Accounting tearsheet for Hayward Holdings (HAYW:USA) highlights, the Uniform P/E trades at 19.6x, which is above the global corporate average of 18.4x and its historical P/E of 17.1x.

High P/Es require high EPS growth to sustain them. In the case of Hayward, the company has recently shown a 26% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Hayward’s Wall Street analyst-driven forecast is for a -38% and 25% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Hayward’s $11 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2022 was 6x the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities and capex maintenance.

Overall, this signals a low credit risk.

Lastly, Hayward’s Uniform earnings growth is below its peer averages and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research