Diamonds are a lender’s best friend

Highly collateralized companies are attractive to lenders because they have valuable assets that can be used to secure loans. This makes it more likely that the lender will be repaid in the event of a default.

Real estate investment trusts (“REITs”) are a prime example of this. REITs own properties, which are valuable and can be easily liquidated. As a result, REITs are able to refinance with ease.

The same is true for companies that own precious metals, such as diamonds. Signet Group (SIG) is the largest diamond retailer in the world, and its portfolio of diamonds provides significant collateral.

However, rating agencies do not see it this way, as they expect the looming recession and falling demand for diamonds to squeeze retailers into more precarious positions.

Today, we’ll take a look at Signet using Uniform Accounting and see if rating agencies’ concerns are in line with the company’s true credit risk profile.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

One of the best things a creditor can look for is collateral.

It’s risky to lend to companies that don’t have assets. For instance, if a software company goes bankrupt, lenders don’t have much to liquidate to make their money back.

That’s why real estate investment trusts (“REITs”) tend to be able to refinance almost whenever they want. They have some of the most liquid assets out there for lenders to deal with.

However, the Fed is penciling in two more rate hikes for 2023 and recessionary prospects are putting pressure on the real estate market.

Because of that, some REITs are starting to come into trouble and some are even starting to mail the keys directly to the banks.

Though some REITs are facing debt headwalls, highly collateralized companies will continue to have an advantage over companies with less tangible backing.

This holds true for another asset class lenders should be excited to get their hands on: diamonds.

Signet Jewelers (SIG) is a great example of this. Just like with real estate, precious gems hold their value quite well.

Signet is the largest retailer of diamond jewelry in the world, operating approximately 2,800 stores primarily under household names such as Kay Jewelers, Zales, and Jared.

Signet has undergone a major restructuring over the past few years, with a focus on omnichannel design and e-commerce penetration. These initiatives have helped the company to generate substantial returns and maintain its place as an industry leader.

However, the rating agencies are worried that with a recession looming and the demand for diamond jewelry falling, the company will struggle to pay off its obligations going forward.

For this reason, S&P has rated the company “BB-”, implying a 10% probability of bankruptcy and placing it in the risky high-yield basket.

However, this is seriously overstating the company’s credit risk.

The company barely has any debt in the next five years and it also has stable cash flows. This means it should have no problems meeting its obligations.

Accordingly, it should have a much safer credit rating, especially when taking into account its precious assets to use as collateral.

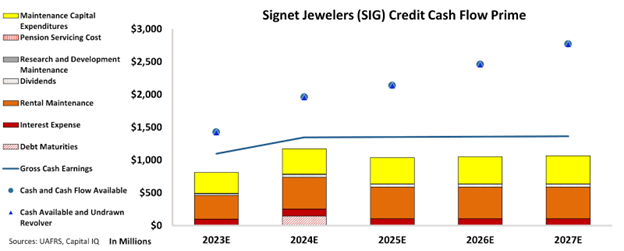

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Signet Jewelers’ cash flows are more than enough to serve all its obligations going forward.

The chart shows that the company’s financial position is strong. Its only debt maturity is in 2024, and it has significant cash flows that could easily pay down that debt and cover all other obligations.

Additionally, the huge spread between its cash flows and obligations provides the company with breathing room in the case of an economic downturn.

Signet’s asset base is also liquid, which means any additional financing needs should not be an issue. This provides the company with further financial security. In the unlikely event of an operational crisis, Signet could lean on its assets as backing.

Due to these factors, we think that Signet shouldn’t be treated like a high-yield name and should be placed within the investment-grade basket.

Hence, at Valens, we are giving an IG3+ rating to this company. As opposed to rating agencies’ unreasonable 10% probability of default, this rating only implies a probability of default of around 1%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Signet Jewelers (SIG:USA) Tearsheet

As the Uniform Accounting tearsheet for Signet Jewelers (SIG:USA) highlights, the Uniform P/E trades at 11.4x, which is below the global corporate average of 18.4x and its historical P/E of 12.3x.

Low P/Es require low EPS growth to sustain them. In the case of Signet, the company has recently shown a 167% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Signet’s Wall Street analyst-driven forecast is for a -19% and 14% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Signet’s $72 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 3x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 140bps above the risk-free rate.

Overall, this signals a moderate credit risk and a low dividend risk.

Lastly, Signet’s Uniform earnings growth is below its peer averages and is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research