Credit Rating Agencies Fail to Recognize the Strength of Sovos Brands Despite Strong Cash Flows and Market Demand

The COVID-19 pandemic has brought on lots of changes, some temporary and others more permanent. One trend that appears to be continuing well past the lockdowns is eating more at home compared to restaurants.

One company benefiting from this is Sovos Brands (SOVO), but credit agencies fail to see its value in the space and think there is a 25% chance it will go bankrupt.

We can use Uniform Accounting to compare the company’s obligations with its cash flows to determine how risky it is in reality.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

One lasting effect of the COVID-19 pandemic was that people continue to spend more time at home.

Even though restaurants have reopened, more people still prefer to eat at home than in past years. A 2021 study from Supermarket News showed that 91% of consumers planned on eating as many if not more meals at home with their families as they did during the pandemic.

Even though more people are cooking at home, convenience is still a priority for many. The solution has been simple meals that can be prepared quickly. Demand for pre-made sauces and frozen foods has risen as a result.

One company that stands to benefit from this market shift is Sovos Brands (SOVO). Sovos has a wide range of packaged food brands that covers breakfast, lunch, and dinner. Pasta, soups, waffles, and sauces are just a few of the goods they offer.

Sovos is taking advantage of this demand and offering products that consumers clearly want. The company has consistently posted positive revenue growth figures since its IPO in 2021.

Despite this, S&P gives the company a B-rating. This translates to a 25% chance of Sovos defaulting according to the rating company.

Given Sovos’ recent success and its current position in the prepared foods industry, this rating seems overly pessimistic.

We can determine if there is a real risk of default for this company by utilizing the Credit Cash Flow Prime (CCFP) to understand the company’s obligations compared to its cash and cash flows.

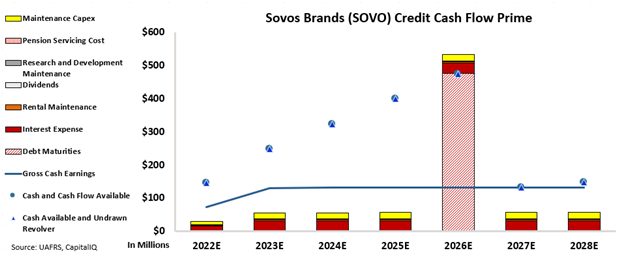

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The chart proves that Sovos has a much safer credit profile than the credit agencies suggested. The CCFP shows that the company’s cash flows consistently exceed operating and financial obligations for the next 6 years.

Sovos has no debt maturities until 2026, when they have a significant debt headwall. Despite this headwall, there is little need for concern.

Sovos has strong cash flows which may get even stronger with improving demand and healthy cash balances. Furthermore, with so much time left to refinance, Sovos will be able to spread out this debt obligation into multiple years.

This is also a company that only recently went public and it will continue to improve, so it is unlikely that this headwall will pose a significant issue.

Because of these factors, Sovos gets an IG3- rating from Valens. This corresponds to a default risk of less than 2%.

The CCFP shows that credit investors should be far less worried about this name than the rating agencies would lead you to believe.

With the power of Uniform Accounting, we hope to highlight the true creditworthiness of companies that are wrongfully judged.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Sovos Brands, Inc. Tearsheet

As the Uniform Accounting tearsheet for Sovos Brands, Inc. (SOVO:USA) highlights, the Uniform P/E trades at 32.9x, which is above the global corporate average of 19.3x and its historical P/E of 18.1x.

High P/Es require moderate high growth to sustain them. In the case of Sovos, the company has recently shown a 61% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Sovos’ Wall Street analyst-driven forecast is for a 68% EPS shrinkage in 2022 and a 679% EPS growth in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sovos’ $14 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 18% annually over the next three years. What Wall Street analysts expect for Sovos’ earnings growth is below what the current stock market valuation requires in 2022 but above in 2023.

Furthermore, the company’s earning power in 2021 is 5x the long-run corporate average. Also, cash flows and cash on hand are almost 4x its total obligations—including debt maturities and capex maintenance.

Overall, this signals a low credit and dividend risk.

Lastly, Sovos’ Uniform earnings growth is well below its peer averages, but the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research