Stable demand isn’t enough to keep this toolmaker safe

When assessing the creditworthiness of a company, being a leading force in the sector often works in its favor. Rating agencies tend to trust that key players in an industry have a competitive edge that can weather economic downturns.

These top firms are often seen as safe bets in categories such as industrial tools and household items, where constant demand supports market stability.

The idea is that their established presence and brand supremacy protect companies against market volatility.

Yet, this perspective might overlook the details of a company’s finances — how much cash they actually have on hand, and how well they’re managing what they owe.

For instance, Stanley Black & Decker (SWK) is a big name in its field, and its strong position might make it look better in terms of credit than a closer look at its finances would suggest.

Today, we’ll look into Stanley Black & Decker’s credit risk using Uniform Accounting to see if rating agencies are accurately analyzing the company.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Rating agencies often view industry leaders with a favorable lens, attributing their established market presence to potential financial stability and resilience.

This outlook is rooted in the belief that companies dominating their sectors have the strategic advantage to sustain operations even during tough market conditions, warranting them stronger credit ratings.

Stanley Black & Decker (SWK), a well-known company in the industrial tools and hardware business, is an example of a market leader.

The brand has earned a reputation for quality and dependability over the years due to its vast product line, which includes anything from power equipment to garden accessories.

It has not only equipped professionals across various industries but also catered to the do-it-yourself (“DIY”) needs of consumers globally, establishing a broad customer base.

However, despite its size, Stanley Black & Decker has not been immune to adversity.

In recent years, the company faced hurdles ranging from supply chain disruptions to changing consumer behavior.

As a result, the company’s Uniform return on assets (“ROA”) took a dip from the historically stable 28% levels to 10% last year.

In response to these pressures, the company made the significant decision to divest itself of certain assets, selling its Electronic Security Solutions and Healthcare Solutions Businesses for $3.2 billion.

This move was intended to streamline its focus on its core businesses and improve its financial position.

However, the strategy took an unexpected turn when Stanley Black & Decker decided to reinvest $2 billion of the proceeds from these divestitures into share buybacks.

Given that the company’s cash flows are not especially robust as we’ll discuss later on, this was a hard decision.

While share buybacks can be a sign of confidence to investors, they can also signal that the company might not have better growth opportunities to invest in.

Furthermore, this financial strategy emerges at a time when the global economy is witnessing volatility, with consumer spending habits shifting and interest rates on the rise.

The macro headwinds make the balancing act between returning value to shareholders and maintaining a healthy cash reserve even more delicate. Thus, the move becomes riskier.

Even with these tough spots and tricky decisions, rating agencies usually still think well of big, well-known companies.

They seem to be paying less attention to the complexities since they are more concerned with the company’s reputation and market position.

Therefore, S&P gives Stanley Black & Decker an “A-” rating. This rating indicates that there is a very low credit risk in the next five years, solidifying the company as a safe investment-grade option.

We think a riskier credit rating is more appropriate considering its current financial status and looming debt maturities.

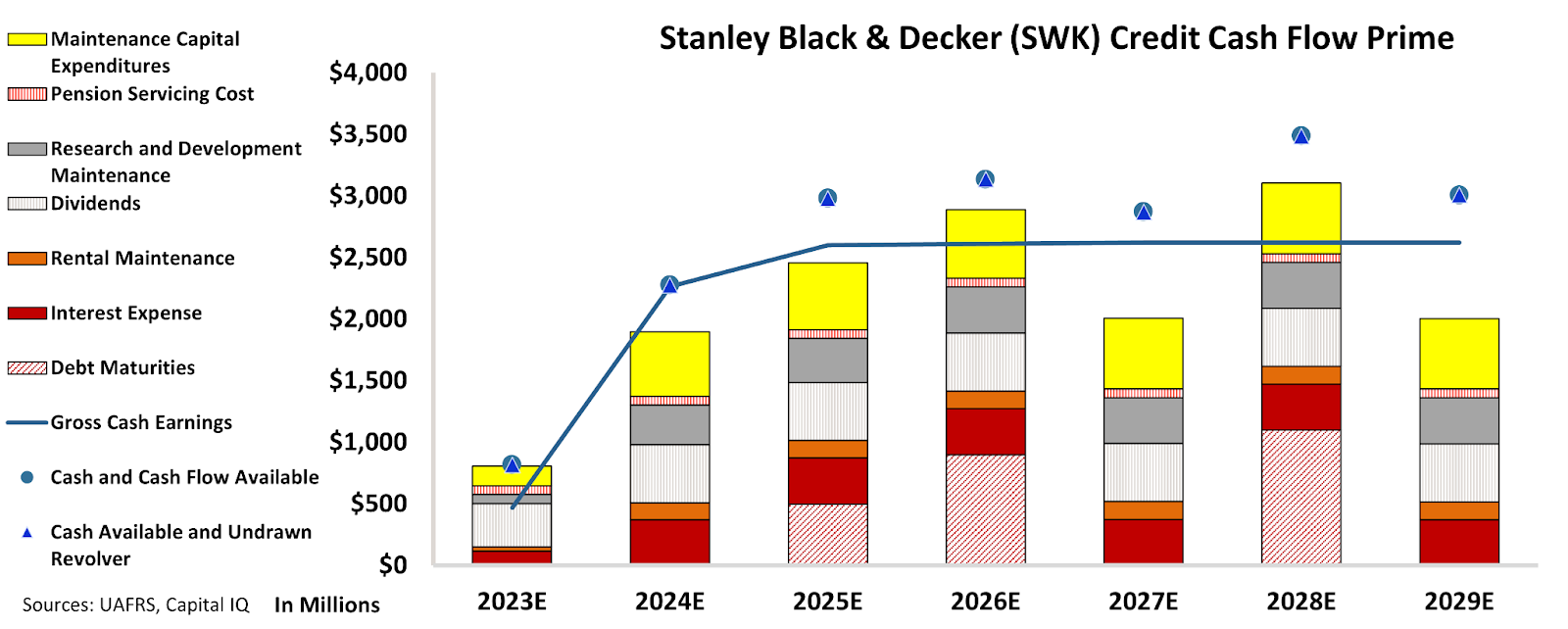

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Stanley Black & Decker’s cash flows are barely enough to support its obligations going forward.

The chart shows that the firm has some significant debt maturities over the next five years and that its cash flows may not be sufficient for its obligations next year. Also, it seems that the company may have difficulties with that limited buffer in case of an economic downturn.

Additionally, with the current high interest rate environment, refinancing these debt maturities may become more expensive.

Furthermore, given the company’s risky practice of repurchasing shares under these conditions, we feel the credit risk is worse than what the rating agencies acknowledge.

Therefore, we assigned the company a “HY1-” rating, placing it in the high-yield category and acknowledging its higher credit risk.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Stanley Black & Decker (SWK:USA) Tearsheet

As the Uniform Accounting tearsheet for Stanley Black & Decker (SWK:USA) highlights, the Uniform P/E trades at 22.6x, which is higher than the global corporate average of 18.4x, but below its historical P/E of 27.5x.

High P/Es require high EPS growth to sustain them. In the case of Stanley Black & Decker, the company has recently shown a 56% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Stanley Black & Decker’s Wall Street analyst-driven forecast is for a 76% EPS shrinkage and a 428% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Stanley Black & Decker’s $86 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 2x the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 210bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, Stanley Black & Decker’s Uniform earnings growth is below its peer averages, but is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research