This company is walking on the edge of bankruptcy

Some companies are getting increased attention from a catalyst and benefiting from it as long as it takes. But once the tailwinds stop, the reality comes up.

That is exactly what has been happening with the infamous online used car retailer Carvana (CVNA). The company and its investors enjoyed soaring stock prices in 2021 but lost almost everything in 2022.

Equity investors are disappointed with the company’s performance, and its creditors are concerned about the possibility of default.

Let’s have a look at the company from the Uniform Accounting lens and see how close the company is to bankruptcy.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Carvana (CVNA) is all over the headlines recently. The company operates an e-commerce platform for buying and selling used cars in the United States.

It is one of the few that enjoyed the pandemic economy. People were stuck in their homes due to lockdowns or restrictions and the ones who wanted to buy a car had to go online for their search.

Many car dealerships were closed and the supply chain problems affected new car sales. This is where Carvana came into play, as an innovative solution for people to buy a car.

The company offered a seamless and fast opportunity for customers. You could just search for a used car through the app and have it delivered to your footstep.

Thanks to this intelligent strategy, the company experienced massive demand and its stock price increased by 330% from the beginning of 2020 to its all-time high in August 2021.

Unfortunately, this happiness did not last very long. Since then, Carvana’s stock fell approximately 98%, meaning all the gains have been lost in that period.

The company has been hit by declining used car prices and rising interest rates, while it was already unprofitable.

Since its inception, the company has never managed to become profitable. Even in 2021 when the demand soared, it had a Uniform return on assets (“ROA”) of -2%.

Rising interest rates, Carvana’s unprofitable history, and its near-term debt maturities are making credit investors scared of the possibility of default.

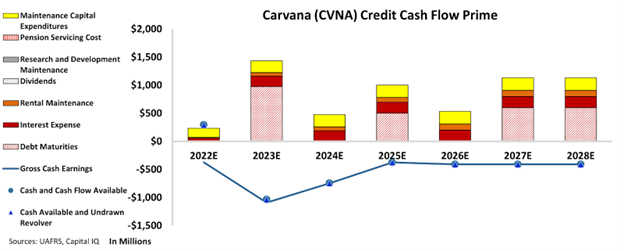

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Carvana’s cash flows are much below its obligations going forward. In fact, it does not even have positive cash available to cover its operating obligations through 2028.

CCFP chart indicates that the company would have negative Gross Cash Earnings in the next 5 years.

It is basically walking on the edge of bankruptcy if it cannot manage the debt loads. Also, the company is now considering possibilities of negotiation with creditors as a bloc.

This means the creditors’ $4 billion unsecured debt in the company might be at risk. That is why, we are giving the company an HY2 rating, which is the lowest credit rating at Valens.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Carvana (CVNA:USA) Tearsheet

As the Uniform Accounting tearsheet for Carvana (CVNA:USA) highlights, the Uniform P/E trades at -4.6x, which is below the global corporate average of 18.4x, but above its historical P/E of -58.7x.

Low P/Es require low EPS growth to sustain them. In the case of Carvana, the company has recently shown a 28% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Carvana’s Wall Street analyst-driven forecast is for a 885% and -27% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Carvana’s $5 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2021 was below the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 520bps above the risk-free rate.

Overall, this signals a high credit risk.

Lastly, Carvana’s Uniform earnings growth is above its peer averages and is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research