This fund has put up impressive returns by being in strong disagreement with Buffett, Uniform Accounting shows what to expect going forward

Value investing has not been in vogue for some time, and this fund has benefited by deprioritizing value in its investment process.

But that doesn’t mean its team has completely forsaken all the valuable insights Warren Buffett’s investing philosophy can offer. The firm has just stated it wants to selectively apply some of Warren’s rules, while saying it strongly avoids others.

Using as-reported numbers though, it appears the firm is ignoring all Buffett’s rules. In reality, UAFRS-based financial metrics help make sense of the stocks the fund is buying, and how they line up perfectly.

In addition to examining the portfolio, we’re including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Warren Buffett is widely respected as not just the greatest value investor of modern times, but the greatest investor.

Berkshire Hathaway’s returns, both how strong they are and for how long, certainly warrant that title.

Some though have been wondering if his lack of action during the pandemic-driven panic in the market is a sign he is starting to “lose his fastball.”

Those arm-chair quarterbacks wonder if he’s become less open to the opportunities in the market, and how the market works today.

There are some parts of Buffett’s philosophy that these investors think are solid core parts of the right kind of investment approach.

His focus on buying high-return businesses with strong economic moats means high visibility for cash flows. Similarly, his focus on quality management teams can give investors confidence that they aren’t investing in a melting ice cube where management mis-steps could disrupt a cash cow.

But these investors appear to question his focus on value, or as Ben Graham and Seth Klarman would say, his focus on “margin of safety,” when making investments.

Quantitative investors have been highlighting how value is “broken” right now too. Quant research greats like Cliff Asness aren’t saying value is dead, but that it is not a factor the market is paying attention to right now.

In an environment like this, it is no wonder a company that de-prioritizes value would have been a big winner the last few years.

Akre Capital Management is a top 3 hedge fund in terms of 3 year performance according to TipRanks.

The team has built this performance on a strong belief in Buffett’s focus on quality companies and management teams. But the “three-legged stool” of the key characteristics the team focuses on differs from Buffett on the third.

Akre cares about finding high-return firms with economic moats, strong management teams and culture they can trust to continue to create value, and the ability for these companies to compound growth over long periods of time.

Buffett also pays attention to companies with growth opportunities, but it is a distant focus relative to finding value. For Akre, growth is far more important than the value you’ll be paying for that growth.

Looking at Akre’s portfolio though, it’s not obvious that the fund invests in either high quality companies or growth opportunities using as-reported metrics.

We’ve conducted a portfolio audit of Akre’s top holdings, based on its most recent 13-F.

We’re showing a summarized and abbreviated analysis of how we work with institutional investors to analyze their portfolios.

Unsurprisingly, while as-reported metrics of Akre’s investments make it look like Akre doesn’t care at all about quality, in reality these investments appear to be higher quality names, once Uniform Accounting metrics are reviewed.

It’s clear that when Akre is making its investment decisions, the team is making decisions based on the real data.

See for yourself below.

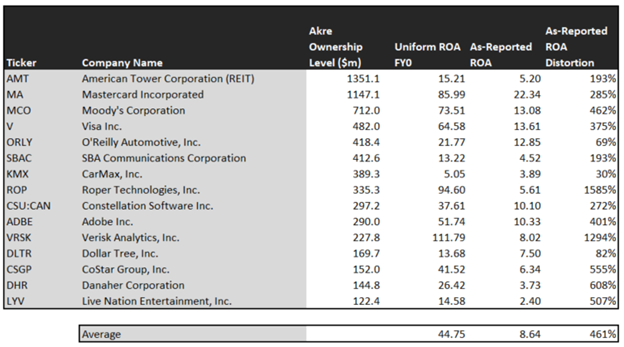

Using as-reported accounting, investors would think Akre was buying anything other than the “forever” businesses like they talk about.

On an as-reported basis, many of these companies are poor performers with returns below 6%, and the average as-reported return on assets (ROA) is right at 9%.

In reality, the average company in the portfolio displays an impressive average Uniform ROA at 45%.

Once we make Uniform Accounting (UAFRS) adjustments to accurately calculate earning power, we can see these are the kind of high return compounders that Akre would be expected to invest in.

Once the distortions from as-reported accounting are removed, we can realize that American Tower (AMT) doesn’t have a 5% ROA, it is actually at 15%.

Similarly, Mastercard’s’ (MA) ROA is really 86%, not 22%. While as-reported metrics are portraying the company as a decently profitable business, Uniform Accounting shows the company’s real robust operations.

Verisk Analytics (VRSK) is another great example of as-reported metrics mis-representing the company’s profitability.

Verisk doesn’t have an 8% ROA, it is actually at 112%. Akre appears to understand that market expectations for the company, thinking it’s a weak business, is completely incorrect.

The list goes on from there, for names ranging from Moody’s (MCO) and Visa (V), to SBA Communications (SBAC), Constellation Software (TSX:CSU), and Live Nation (LYV).

If Akre were focused on as-reported metrics, it would never pick most of these companies because they look like anything but companies with strong economic moats, sound operations, and significant growth opportunities.

But it appears that Akre is making a broader bet than just on high-quality firms. It has put a stake in the ground, saying that quality and growth matter, but that valuation doesn’t.

It wouldn’t necessarily be apparent when looking at the as-reported metris, but Uniform Accounting metrics paint a complete picture of the fund’s investment philosophy.

This chart shows three interesting data points:

- The 2-year Uniform EPS growth represents what Uniform earnings growth is forecast to be over the next two years. The EPS number used is the value of when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market expected Uniform EPS growth is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily analyses and reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for uniform earnings growth.

- The Uniform EPS growth spread is the spread between how much the company’s Uniform earnings could grow if the Uniform earnings estimates are right, and what the market expects Uniform earnings growth to be.

The average company in the US is forecast to have 5% annual Uniform Accounting earnings growth over the next 2 years. Akre’s holdings are forecast by analysts to grow slightly more than that, growing at 6% a year the next 2 years, on average.

But Akre appears to be betting the market knows more than analysts, and is expecting stronger fundamental tailwinds going forward. And it is willing to pay up for this higher expected growth.

On average, the market is pricing these companies to grow earnings by 13% a year. The market is pricing these companies for growth to be 7% higher than analysts are forecasting. For Akre to see these stocks appreciate, it is going to need to see them grow significantly more than analysts are expecting.

This appears irrational initially, but it may be exactly in line with Akre’s three part process of focusing on high quality companies with strong management teams and growth compounding opportunities.

One example of a company in the Akre portfolio that the team is expecting to have stronger growth than analysts are forecasting is Visa (V). Visa’s Wall Street analyst forecasts have 3% Uniform earnings growth built in, but the market is pricing the company to have earnings grow by 13% each year for the next two years. Akre is expecting management can deliver that above trend growth, and that’s what they’re investing in.

Another company with similar dislocations is CarMax (KMX). The company is forecast for Uniform EPS to shrink by 5% a year. But Akre and the market are expecting the company management team can deliver growth of 8% a year.

Yet another is Adobe (ADBE), priced for 21% growth in Uniform earnings, when the company is forecast to grow by earnings by 14% a year.

There’s really only one company in the fund’s top holdings that would be defined as traditionally “undervalued” and that is Danaher (DHR). Danaher is forecast to see Uniform earnings grow by 17% a year going forward. However, the market is pricing the company for only 9% annual earnings growth.

But even Danaher isn’t a “value” stock, as it’s trading at a 33x Uniform P/E. The company’s growth is being undervalued, but the market is still paying a premium for this name.

Overall, it is clear Akre is all in on quality growth, and throwing valuation cares to the wind. It wouldn’t be clear under GAAP, but unsurprisingly Uniform Accounting sees the same signals that Akre says it is investing in.

American Tower Corporation Tearsheet

As one of Akre Capital’s largest individual stock holding, we’re highlighting American Tower Corporation’s tearsheet today.

As our Uniform Accounting tearsheet for American Tower Corporation (AMT:USA) highlights, American Tower’s Uniform P/E trades at 36.1x, which is above average valuation levels and historical average levels.

High P/Es require high EPS growth to sustain them. In the case of American Tower, the company recently had a 15% Uniform EPS growth in 2018.

While Wall Street stock recommendations and valuations poorly track reality, Wall Street analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

As such, we use Wall Street GAAP earnings estimates as a starting point for our Uniform earnings forecasts. When we do this, we can see that American Tower is forecast to see Uniform EPS growth of 4% in 2019, followed by 8% EPS growth in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $242 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of American Tower, the company would have to grow Uniform EPS by 13% each year over the next three years.

What Wall Street analysts expect for American Tower’s earnings growth is below what the current stock market valuation requires.

Furthermore, based on Uniform return on assets calculation, the company’s earning power is at 15%, which is 3x the corporate average. However, with cash flows and cash on hand that are below total debt obligations, American Tower has high credit and dividend risk.

To conclude, American Tower’s Uniform earnings growth is above peer averages but is currently trading in line with peer averages.

Best regards,

Joel Litman

Chief Investment Strategist

at Valens Research