This unorthodox measure of a market top may lead investors astray

Over the past few weeks, investors have been concerned about potential headwinds to the recent bull market.

Many pundits have raised fears about high inflation or rising rates bringing the recent rally to a screeching halt. While we have broken out over the past few weeks why these fears are overblown, there is a new concern gripping the financial media.

Today, we will talk about the risk of management sell-offs to market health, and if you should be worried.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Just last week, we talked about how many investors are putting the cart in front of the horse and growing skittish around potential rate hikes.

Higher tax rates could mean companies have less money to invest in growth. Higher rates could also push the market discount rate higher. Both of these actions risk pushing the market lower.

With high tax rates, investors can theoretically put their money in high return bonds or savings accounts, only accepting more attractive prices to invest in the market.

After all, the argument goes, with a heightened risk of inflation coming in 2021 and beyond, the Fed’s best tool for keeping prices in line is raising rates.

Raising rates now also gives the Fed “ammunition” for the next crisis. By having high rates before a crash, the Fed can aggressively cut rates to encourage spending.

Many op-eds, news anchors, and pundits are looking to chase a story on potential rate increases and creating lots of fear about the market.

The reality is they’re missing the point.

With rates near all-time lows, any modest short term rate hikes won’t cause the stock market to come crashing down. Historical analysis shows the exact opposite to be the case.

The Fed raises rates when it expects strong economic growth, which drives corporate earnings growth. The Fed raising rates is actually an incredibly bullish signal for the stock market in the short-term.

Barron’s recently published a piece on why an increase in interest rates will not cause the economy to come screeching to a halt.

However, the article substituted interest rates with another concern explaining why they believe the stock market is a bubble about to burst.

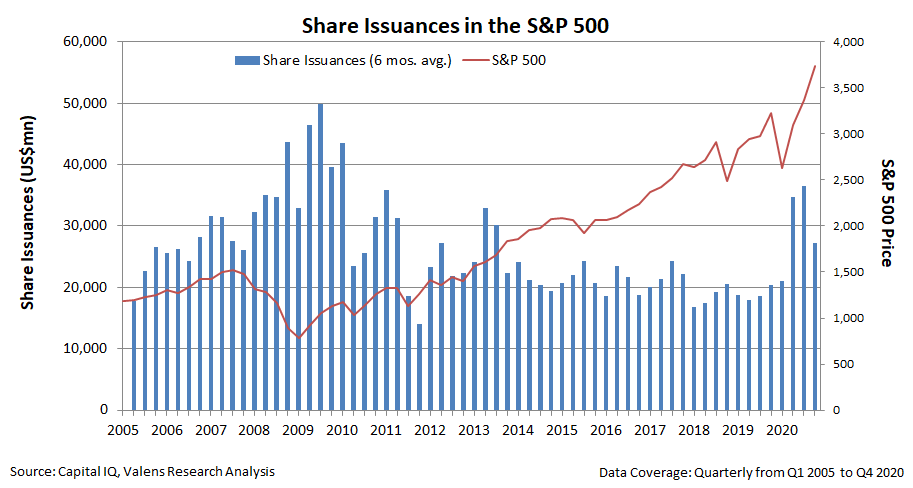

The article highlights that investors should be spooked as corporate management teams are issuing large amounts of equity. The article uses companies like QuantumScape (QS), Nikola (NKLA), and Canopy Growth (CGC) as three names, which have used the recent rally to raise capital at attractive prices.

Barron’s argument is that traditionally, management teams love to try and time the top of a market to secure the best possible price for an equity issuance. If they issue stock at what they think are inflated values and turn it to cash, they can “lock in” their position.

As management teams know the most about their companies, this could be the first sign that the market could be turning.

Now the reality is rather different. As any analysis of share buybacks and share issuances would show you, management teams really have a habit of buying back shares at peak valuations, and selling shares at trough valuations. But leaving that aside, this is still no reason to panic.

While management looking to raise equity can be a powerful signal when studied with context, those companies raising massive amounts of equity means little for stock market valuations today.

While there has been a noticeable jump in equity issuances on a six-month rolling average in the past year, this isn’t because management teams are seeing the end.

The first spike in equity issuances in fact came during March and April, right at the bottom of the market, not the top. When government stimulus was still in the works, companies needed to source money any way they could to simply stay afloat.

Furthermore, the current low-rate environment has made special purpose acquisition companies (SPACs) a popular choice for investors over the past few months. Sizable equity raises for new SPACs have driven up this number as well, as have secondary raises for these companies when they undertake acquisitions.

The biggest among the S&P 500 are not running to source new equity raises. The Procter & Gambles (PG) of the market are not the ones conducting equity raises today.

Barron’s has picked three specific stocks with equity raises, which have seen recent speculative runs.

These stocks have little correlation with the market as a whole. Perhaps instead of calling the top of the market, these management teams are just calling the top of their own stocks…

QuantumScape is currently working to develop a next-generation solid-state lithium battery. However, the company doesn’t predict seeing profitability for years to come. So the company needs a lot of capital to fuel its investment.

Meanwhile, the zero-emissions vehicle company Nikola is currently being investigated by the SEC and the Department of Justice over securities fraud allegations. It also is an early lifecycle company starved for capital.

Finally, Canopy burned through an eye-watering $3.3 billion of cash in 2019 and 2020 looking to turn profitable. Rather than looking for a top, Canopy is looking for any means it can to stay afloat.

Instead of a warning to heed, Barron’s is barking up the wrong tree. This is just another example of the financial media looking for a story without providing the context to anchor the data.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research