This expected transaction could change the fate of Italy’s largest telecom operator

Some companies rely highly on debt to continue their operations or to drive growth. But when the debt repayments come due, problems start to arise.

This is what Italy’s largest telecom operator, Telecom Italia S.p.A. (TIT:ITA) also known as “TIM”, has been dealing with for a long time.

Now, the company is looking for ways to get rid of the massive debt pile and to reach a healthier capital structure. To do so, it’s planning to sell some of its assets.

Let’s take a look at the company from the Uniform Accounting perspective and evaluate if the expected transaction can help it achieve its goals.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Some companies are taking on massive debt and have difficulties when the maturities come.

Telecom Italia has been dealing with debt problems for a very long time. Now, it wants to get rid of these issues and clean up its capital structure.

The company found a way to do that by selling its grid assets.

These assets, including the company’s landline network and submarine cable unit, are expected to bring somewhere between 20 to 25 billion Euros to the company.

The well-regarded U.S. based private equity firm KKR (KKR) has already made a proposal to acquire these assets for 20 billion Euros.

If completed, this transaction would significantly help the company to pay down its debt pile and reshape its capital structure.

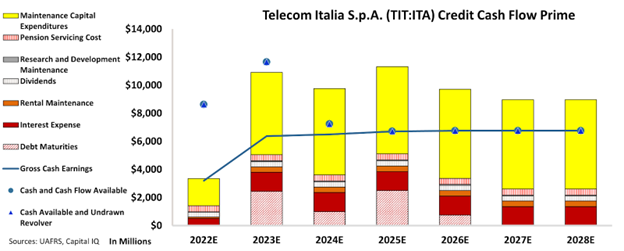

Let’s have a look at the company’s current capital structure by leveraging Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart clearly shows that Telecom Italia’s cash flows are not sufficient to cover its obligations going forward.

CCFP chart indicates that the company has significant debt maturities in the next few years and its operating obligations make it challenging to handle them.

The company’s current capital structure is not sustainable and it clearly shows why Telecom Italia has been pushing to sell its grid assets.

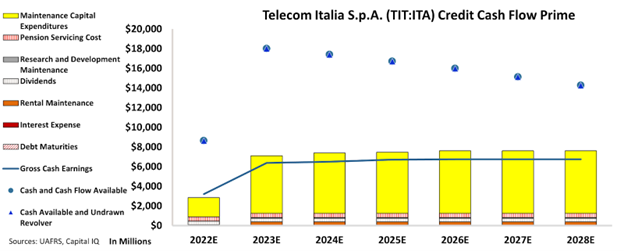

In light of this, let’s take a look at the company’s adjusted CCFP to understand how its capital structure might change if the transaction is successfully completed.

We’re not expecting that the company will use all of the proceeds from the transaction to pay off its debt maturities.

But if it did, that could clean up its entire capital structure and look much safer and healthier.

The adjusted CCFP clearly shows that the company would have no significant debt maturities remaining and its cash flows would be more than enough to serve its obligations going forward.

Hence, it could achieve its goal of a healthier balance sheet and have a chance to reshape its capital structure.

That is why this transaction is highly critical to the company’s future and it has the potential to make or break Italy’s largest telecom operator.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Telecom Italia S.p.A. (TIT:ITA) Tearsheet

As the Uniform Accounting tearsheet for Telecom Italia S.p.A. (TIT:ITA) highlights, the Uniform P/E trades at 52.3x, which is above the global corporate average of 18.4x and its historical P/E of 36.9x.

High P/Es require high EPS growth to sustain them. In the case of Telecom Italia, the company has recently shown a 808% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Telecom Italia’s Wall Street analyst-driven forecast is for a -100% EPS decline in 2022 and an immaterial EPS growth in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Telecom Italia’s €0.31 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2021 was below the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 150bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, Telecom Italia’s Uniform earnings growth is below its peer averages and is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research