Two economic indicators recently touched 20-year lows, which may be a surprisingly strong growth signal

Understanding business capacity is necessary to know where we are in the business cycle. It’s more than a measure of efficiency–it also provides valuable insights on growth prospects.

Today, we will look at how efficiently the economy is operating. Through the use of two important economic indicators, we can gain an understanding of where the economy goes from here as we approach the year end.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Cruise operators have been devastated by the pandemic. Concerns over coronavirus have halted cruise ships for much of the year. This has caused revenue to collapse for major cruise line operators like Carnival (CCL). And since cruise ships haven’t been operational, most people still consider them too dangerous as they remember stories from the beginning of the pandemic.

When the pandemic had just begun, one of the first major outbreaks was on a cruise ship. The Diamond Princess ship saw over 700 passengers and crew members test positive for coronavirus. Crew and passengers were stuck on board for nearly a month and they had to quarantine before returning to their respective home countries.

Stories about the Diamond Princess and another ship in Hong Kong were some of the first articles Americans read about the pandemic.

Naturally, with the headline risk and diminished demand, cruise ship companies have faced tough decisions. For some ships, this has meant a final voyage to a scrap yard.

As this Bloomberg article highlights, some cruise ship operators are sending their older ships to Turkey. There, the exhaustive and dangerous 9-month process of salvaging a ship’s parts take place.

Everything from a ship must go. This includes artwork, kitchen equipment, and copper wires. Yet, nothing is more valuable than the steel. The steel alone can be worth north of $4 million per ship.

This is part of the natural life cycle of a ship. However, the pandemic has ended some ships’ lives earlier than expected.

While the process is not pretty, it is the only choice for struggling cruise lines. It costs money to store and maintain any large ship. With no demand for cruises, salvaging is the only income source for management. The cruise lines are hoping to stay solvent long enough to last through the pandemic. Then, spending can also return to normal levels.

Additionally, spending cuts today can actually set companies up for future growth. Changes in spending correlate to changing the total capacity of the economy. Reduced investment means supply doesn’t grow as fast. As demand starts to pick up, capacity gets tighter, and prices rise. Higher prices mean higher profits for businesses. Those higher profits make it likely companies will reinvest more to grow. To do this, companies will need to invest in capital expenditures.

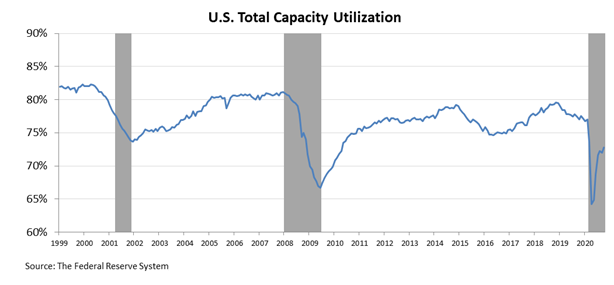

To understand how companies can grow through investments, we like to look at the capacity utilization rate.

Essentially, the capacity utilization rate measures the extent to which companies are putting their capacity to work. A higher rate means more of the economy is running near total capacity, a lower rate means there is room to grow.

We last looked at the metric over the summer. At the time, the utilization rate had collapsed. Lockdowns and other measures to slow the spread of the coronavirus pandemic resulted in a lower total capacity utilization rate than during the Great Recession.

The rate bottomed out, briefly hitting 65%. However, as parts of the economy have opened, the total capacity utilization has as well. Currently, it sits above 70% and it has been improving since the summer.

This is a bullish sign for the economy, as the recoveries in past recession were far slower. After the dot com bubble, it took three years for total capacity utilization to rise just over 6%. After the Great Recession, the rebound was similarly slow.

As is the case with many economic norms during recession, this pandemic-fueled downturn breaks the mold for standard patterns. Both the crash and recovery for capacity utilization rate have been more rapid than previous downturns.

Without serious credit issues in the broad economy, utilization has been able to bounce back with little delay. However, until capacity utilization gets tighter, growth in capex will be hard to sustain. Companies can see sales growth without having to build new plants if they have idle ones.

The good news for capex is vaccine distribution has begun. When the economy opens back up, the total capacity utilization rate can bounce back even further. At that point, there will be plenty of room for investment in capex.

The need for further capex is acute because assets are old right now. Companies had been under-investing for a while, even before the pandemic.

This can be seen in the ratio between gross property plant and equipment (PP&E) and net PP&E. This ratio continues to fall, which means companies’ assets are older, or further depreciated. Companies have been putting off necessary investments to update equipment due to the recession.

The current ratio is at its lowest level this century, making opportunities for capex ripe for the picking.

The combination of strongly recovering capacity utilization and old assets should have investors excited about the potential for strong reinvestment for companies as the recovery gains steam.

If capacity utilization rate continues to rise, the virtuous cycle of business growth can then continue. Management teams will begin investment in their businesses, which spurs spending in other parts of the economy.

While there is still a way to go for a full recovery, the path is becoming clearer.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research