One semiconductor firm has stayed out of the headlines during the current shortage, and that’s for the best

While many companies have faced significant headwinds in the technology sector given the material shortages in semiconductors, this firm has thrived.

Combining its ability to conduct smart operational strategies on its supply chain with its highly differentiated brand in the market, this firm is printing cash.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

One of the biggest headlines for the past several months in the technology industry has been in the world of hardware.

Historically, the hardware space within the tech industry has been a component less recognized by individuals.

Everyone is more focused on cloud and social media as well as software as a service (SaaS) models, which we highlighted recently. They tend to pay less attention to the hardware aspect within the industry.

These problems start from the supply chain constraints in the semiconductor industry and how companies are trying to source their much needed chips for their products.

The problem also highlights how these semiconductor shortages impact various industries around the world, from automotive products to more traditional semiconductor consuming industries such as smartphones.

While many companies have faced these challenges head on throughout the order of events, there are companies that have bypassed these obstacles.

One company that has not been caught up in recent headlines is Texas Instruments (TXN).

Texas Instruments has stayed out of the headlines for two specific reasons.

First, the company has been much more active in controlling its whole supply chain as well as manufacturing its semiconductor chips in house.

Consequently, the company has not faced the same issues of getting outsourced semiconductor fabrication plants to prioritize its chips production.

Secondly, Texas Instruments has spent the past ten years focusing on specialized segments within the semiconductor market where it believes it can differentiate itself from peers.

For example, the company is the leader within the analog chips segment of the market.

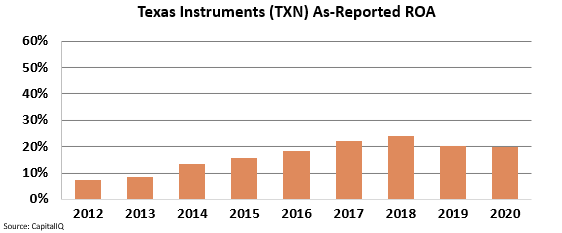

So, many investors might be curious how these two key components of the company have translated into its financial performance, specifically its returns.

By viewing the as-reported metrics, investors can see Texas Instruments has, in fact, done quite well.

Specifically, the company’s ROA trend has been strong since 2012. ROA levels have expanded from 7% in 2012 to 20% in 2020.

In reality, this is not an accurate picture of Texas Instruments’s performance. It only begins to paint the picture of the company’s true profitability.

While investors may look at the above data and conclude the company has done well over the years, they are missing an even more vibrant story.

When looking through a Uniform Accounting lens, it becomes clear that the firm’s business model is better than it seems.

Specifically, the company has been able to expand its ROA generation from 18% levels in 2012 to 47% in 2020.

The company is printing cash.

The company’s ability to control its supply chain and manufacture its own chips, coupled with its specialization in niche segments within the market has translated into massive profitability levels given its premium prices.

Without Uniform Accounting, investors would be unsure of the true power Texas Instruments has unlocked thanks to its smart operational strategies and differentiation.

SUMMARY and Texas Instruments Incorporated Tearsheet

As the Uniform Accounting tearsheet for Texas Instruments Incorporated (TXN:USA) highlights, its Uniform P/E trades at 23.9x, which is around the global corporate average of 25.2x, but above its own historical average of 21.0x.

Moderate P/Es require moderate EPS growth to sustain them. That said, in the case of Texas Instruments, the company has recently shown a 10% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Texas Instruments’ Wall Street analyst-driven forecast is a 12% and 6% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Texas Instruments’ $172 stock price. These are often referred to as market embedded expectations.

Texas Instruments is currently being valued as if Uniform earnings were to grow 4% annually over the next three years. What Wall Street analysts expect for Texas Instruments’ earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 8x the long-run corporate average. Also, intrinsic credit risk is 50bps above the risk-free rate and cash flows and cash on hand consistently exceeds total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low dividend and credit risk.

To conclude, Texas Instruments’ Uniform earnings growth is somewhat in line with peer averages, and the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research