This market consolidator has a much safer credit risk than rating agencies think

Some companies follow aggressive acquisition strategies to consolidate the market they operate in.

As they usually take on debt to fund their acquisitions, they are considered as high credit risk companies.

However, if these acquisitions help the company to drive growth and profitability, and have a strategic rationale, it does not always mean that it has a high default risk.

A great example of this is Vista Outdoor (VSTO). Rating agencies think it has high credit risk and rate it with a high chance of bankruptcy.

Let’s see the company from the Uniform Accounting perspective and evaluate its credit risk.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

People usually think that when a company makes a lot of acquisitions, it takes a huge chunk of debt and therefore incurs significant credit risk.

However, this is not always the case, especially if a company has a strategic capital allocation roadmap to grow the business and improve its profitability.

Vista Outdoor is one of the companies that follows an aggressive acquisition strategy to consolidate the outdoor and sporting products market.

The company provides consumer products for the outdoor sports and recreation markets worldwide. It’s among the leading providers of ammunition and related equipment.

To drive growth, improve its profitability, and consolidate the outdoor and sporting goods market, it has made more than 10 acquisitions in the last 5 years.

Thanks to its strategic acquisitions, Vista has been able to increase its total revenue by more than 30% and its operating income has grown almost tenfold since 2018.

Its ammunition business is pretty much recession-proof while its sporting goods business is about to float on its own with the post-consolidation of the market, de-risking the company’s core business.

Taking these into account, the company does not seem like an aggressive acquisitive company that consistently overleverages its balance sheet to drive growth.

Yet, rating agencies like S&P seem to miss all these facts and rate the company “BB”, which implies around a 10% chance of default.

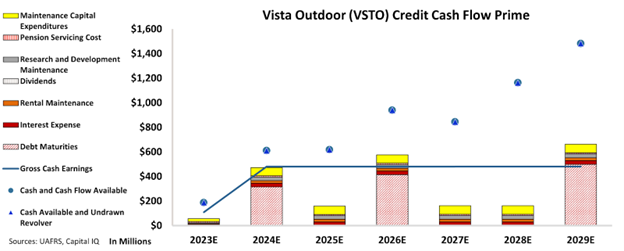

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that Vista Outdoor’s cash and cash flows are always above its obligations going forward.

CCFP chart indicates that the company has consistent debt maturities in the next few years.

However, it has sufficient cash and cash flows to cover all these obligations. Also, with the post-consolidation of the markets it serves, its profitability might even see further improvement.

Additionally, it has the opportunity to refinance its obligations going forward.

Yet, S&P rates the company “BB”, implying a very high chance of default, at around 10%.

Considering its success in strategic acquisitions and improved profitability, this is too much credit risk accounted for towards the company.

That is why, at Valens, we are rating the company “IG4”, which implies around a 2% chance of default and reflects the company’s resilient financial positioning.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Vista Outdoor (VSTO:USA) Tearsheet

As the Uniform Accounting tearsheet for Vista Outdoor (VSTO:USA) highlights, the Uniform P/E trades at 6.6x, which is below the global corporate average of 18.4x but above its historical P/E of 5.2x.

Low P/Es require low EPS growth to sustain them. In the case of Vista Outdoor, the company has recently shown a 99% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Vista Outdoor’s Wall Street analyst-driven forecast is for a 25% and 14% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Vista Outdoor’s $26 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power in 2022 was 6x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 300bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, Vista Outdoor’s Uniform earnings growth is below its peer averages and is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research