Mylan may now be called Viatris, but the story still looks bleak

Sometimes, when companies find themselves between a rock and a hard place, they take desperate measures to change their optics.

As investors think about Facebook’s change to “Meta”, it may be important to look closely at another major rebranding effort.

Now that infamous Mylan is called Viatris and has merged with another large pharmaceutical business, the Credit Cash Flow Prime reveals that the narrative change may not have changed as much as management might have hoped.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Last week, Facebook’s announcement that the company is performing a full-stop rebrand as “Meta” made waves in the business world.

Mark Zuckerberg explained to investors and the public that he sees the “Metaverse” as the primary center for Facebook in the future. But the change comes amid an outpouring of bad headlines and public disdain about the company.

While the rebrand may be the right step for Facebook, just changing a company’s name can’t fix all the issues hovering overhead.

For Facebook, users and politicians alike have been vocalizing their disdain for the social media platform’s broader influence on society.

This may go down as one of the highest-profile rebranding exercises in the history of the corporate world, but there was another company that scrambled to rebrand a year ago. Mylan, a pharmaceutical company with a large generics operation, was also struggling to overcome bad optics.

Mylan was at the center of nationwide outrage about unreasonably high drug prices. It was jacking up the price of its EpiPen product, which tens of millions of people had come to depend on as a first line of defense against severe allergic reactions, to the tune of 600% since its launch.

At the same time, the company was running a colossal marketing campaign about EpiPen and its market dominance, attempting to push competing products to the sidelines. There were lawsuits, public hearings, and direct criticism from popular politicians. Even Mylan’s CEO at the time, Heather Bresch, went on record saying that she “gets the outrage.”

Worse yet, the company was also under fire by its investors due to declining overall business performance. The story needed to change, and quickly.

In 2020 Mylan merged with Pfizer’s (PFE) Upjohn business. Upjohn also specializes in off-patent products, so the pairing had the potential to create a larger business with more scale to reverse the declining operations.

The new combination became known as Viatris (VTRS). Not only did the corporate story change, the name-change helped clear some of the disdain associated with the Mylan name.

While the new company’s stock has been sideways to down since it began trading in late 2020, it looks like the rating agencies have bought into the new narrative, rating the company as a low-end investment grade name, with a BBB- rating.

While this rating sits at the meeting point between riskier high-yield and safer investment grade names, it tells creditors that the chance of default over the next five years is below 2%.

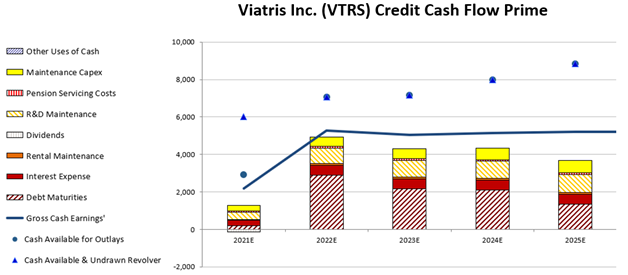

Here at Valens, we need to see the data corroborate these narrative changes before making judgements. Looking at the company’s Credit Cash Flow Prime (“CCFP”), we see a bleaker picture than ratings agencies.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP exposes Viatris as a company with regular and material debt maturities for each of the next five years. Moreover, with future expected cash flows that only barely exceed the company’s obligations for many years going forward, Viatris may struggle to finance the R&D projects that it depends on.

This earns it an HY2- credit grade, in high-yield territory. If cash flows continue to decline as they have historically, creditors could be disappointed that they, like the rating agencies, got caught up in the narrative without critically studying the data.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Viatris Inc. Tearsheet

As the Uniform Accounting tearsheet for Viatris Inc. (VTRS:USA) highlights, the Uniform P/E trades at 19.2x, which is below the global corporate average of 24.3x but around its historical P/E of 18.0x.

Low P/Es require low EPS growth to sustain them. In the case of Viatris, the company has recently shown a 40% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Viatris’ Wall Street analyst-driven forecast is for 83% EPS shrinkage in 2021 followed by a 430% growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Viatris’ $13.3 stock price. These are often referred to as market-embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 1% over the next three years. What Wall Street analysts expect for Viatris’ earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power in 2020 is 2x the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 130bps above the risk-free rate. All in all, this signals a high dividend risk.

Lastly, Viatris’ Uniform earnings growth is below peer averages and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research