Whirlpool is ready to ride strong capex tailwinds to profitability

We have talked regularly about the capex revolution that is underway. This has implications from large-scale government infrastructure spending, to company’s reinvesting in their infrastructure.

Whirlpool is one of the most prominent household appliances companies in the United States. However, it appears they have maintained a low profitability even in the face of these massive tailwinds in recent years.

Today, we are going to take a closer look at the performance of Whirlpool to see its true performance under Uniform Accounting metrics.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Here at Valens, we have talked regularly about the idea of the capex spending boom. As you can see from when we talked about C&I Loan Growth, low Net/Gross PP&E, and high management sentiment, it has been a consistent theme.

The volatility of the past couple of years has provided us with a series of factors that have contributed to this inflection point.

Part of the reason we see this capex inflection occurring, as we have mentioned before, is because the COVID-19 pandemic has overhauled how people approach their lives.

Rather than prioritize certain amenities of the past, such as going out to the theater or a restaurant, consumers are more likely to create that environment in their own homes.

This desire has been a strong driving force in changing the demand people have for goods. And as one may expect with so many people rushing to reconstruct their homes, household appliances have seen an outsized portion of this demand.

Between this heightened demand for reconstructing homes to the surge of people looking for new homes, these appliances are seeing long supply backlogs.

At this point, many of these household appliances and furniture pieces are looking at backlogs measured by the months.

Although consumers may be frustrated by the lengthy waits, this visibility into demand is giving management teams confidence that they have clear cash flow visibility to position themselves well.

Management can make better decisions about investing in their assets, but that does not necessarily mean every management team should rush out and invest in growth. That growth has to be profitable for shareholders, or it is a waste.

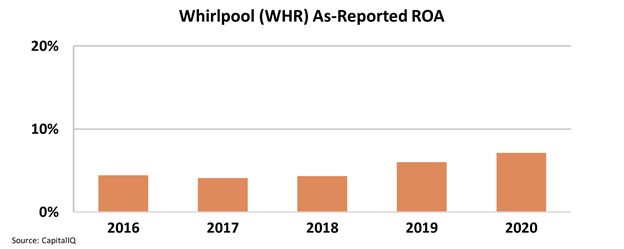

Yet looking at as-reported metrics, it looks like it might be better for a company like Whirlpool (WHR) to not spend large amounts of investor capital to expand capacity.

With a ROA that has consistently been below 5% each year, and only barely beating the cost of capital at 7% in 2021, this is a company that does not appear to create value for investors.

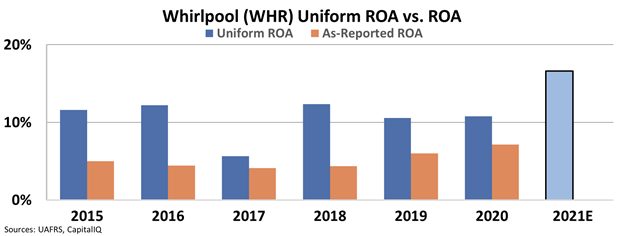

However, Uniform Accounting tells us a different story. It shows us why it may be wise for Whirlpool to expand capacity, as it is already a 10% a year ROA business in five of the past six years.

Going further, it is forecasted to see even more strength in 2021. If the company can follow in the footsteps of Boeing and Airbus, by maintaining operations and then use its backlog to sustain profitability, Whirlpool is poised for profitable growth.

Uniform Accounting makes it clear that this is a business that is ready to capitalize on the perfect storm of demand that comes with the capex revolution.

While Whirlpool is positioned to do incredibly well, the market may not know this. Distortions in as-reported metrics may convince investors that Whirlpool is a poor business, but Uniform metrics tell us otherwise. To see what markets are pricing in for Whirlpool to do in the future, you can subscribe to our database.

SUMMARY and Whirlpool Corporation Tearsheet

As the Uniform Accounting tearsheet for Whirlpool Corporation (WHR:USA) highlights, the Uniform P/E trades at 11.8x, which is below the global corporate average of 24.0x, but around its own historical P/E of 12.1x.

Low P/Es require low EPS growth to sustain them. In the case of Whirlpool, the company has recently shown a 12% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Whirlpool’s Wall Street analyst-driven forecast is a 68% EPS growth in 2021 and a 22% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Whirlpool’s $204 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 5% annually over the next three years. What Wall Street analysts expect for Whirlpool’s earnings growth is above what the current stock market valuation requires in 2021 but below that requirement in 2022.

Furthermore, the company’s earning power in 2020 is twice the long-run corporate average. Moreover, cash flows and cash on hand are also twice its total obligations—including debt maturities, capex maintenance, and dividends. Overall, this signals a low credit and dividend risk.

Lastly, Whirlpool’s Uniform earnings growth is above its peer averages and the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist&

Director of Research

at Valens Research