This truck manufacturer is made to deal with the driver shortage

The trucking industry was forced to endure a tumultuous few years as a result of the pandemic. As supply chains begin to recover, commercial truck companies like Wabash National that weathered the storm see an opportunity to capitalize.

As the current truck driver shortage is addressed, demand for commercial truck and trailer manufacturing will also increase. Wabash was able to expertly navigate its debt obligations during the pandemic and is well positioned to service the supply chain reinvestment. However, ratings agencies are still missing the picture.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Tearsheets

Powered by Valens Research

It’s no secret that there is a current truck driver shortage in the United States. As the economy begins to rebound, companies need to address the supply chain issues that have impeded growth and driven inflation.

Part of solving this puzzle will be solving the trucking shortage to bring shipped products the last mile.

If the trucking industry begins to pick up, all signs point to truck manufacturers benefitting. Wabash National Corporation (WNC) is a market leader in the design and manufacturing of semi-trailers and specialized commercial vehicles.

In 2015, Moody’s gave the company a Ba3 rating, signifying a low risk of default. However, in 2020 Moody’s downgraded Wabash to a B1 grade. Moody’s now thinks that despite the potential for significant demand growth in the near future, default chances are higher than ever before.

During the pandemic when the world came to a standstill, the trucking industry was one of the many casualties of the economy grinding to a halt. Despite this, Wabash was able to weather the storm through smart balance sheet management.

Wabash has been very successful in managing its debt obligations in recent years and there is little to suggest that this will change in the coming years. This is why it is bizarre for Moody’s to continue giving the company a B1 rating.

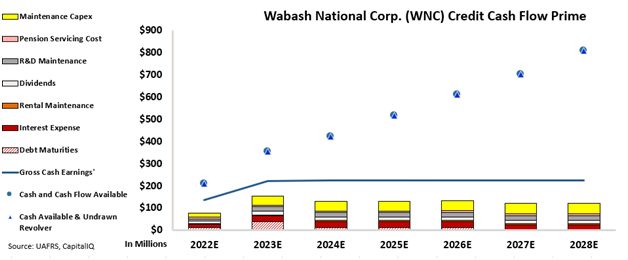

We can see exactly how safe the name is by examining it through the Credit Cash Flow Prime perspective.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The B1 rating suggests a moderate risk of default, but the CCFP shows that Wabash’s cash flow alone is more than enough to cover all of its obligations over the next seven years.

Considering that Wabash will continue to improve its already healthy credit picture over time, it’s nonsensical that ratings agencies like Moody’s are still so apprehensive towards this company.

That is why it deserves to have an IG3+- rating, which corresponds to a default risk of around 1%. This is a far cry from the 24% default risk that Moody’s is implying with its credit rating.

Rating agencies seem to miss the potential of sound companies again, by rating Wabash National much riskier than it actually is.

On the other hand, Valens Credit Rating reflects the full story of the company with much less risk than what the rating agencies suggest.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Wabash National Corporation Tearsheet

As the Uniform Accounting tearsheet for Wabash National Corporation (WNC:USA) highlights, the Uniform P/E trades at 11.9x, which is around the global corporate average of 19.3x, but below its own historical P/E of 17.6x.

Low P/Es require low EPS growth to sustain them. In the case of Wabash National, the company has recently shown a 29% decline in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Wabash National’s Wall Street analyst-driven forecast is 221% and 19% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Wabash National’s $16 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 3% annually over the next three years. What Wall Street analysts expect for Wabash National’s earnings growth is above what the current stock market valuation requires in 2022 and 2023.

Furthermore, the company’s earning power in 2021 is 1x the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals low dividend and credit risk.

Lastly, Wabash National’s Uniform earnings growth is well above its peer averages, but the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research