This company is pioneering the future of recruitment

The job market has recently undergone significant changes, disrupting traditional recruitment practices due to macroeconomic challenges like layoffs and potential recession, alongside technological advancements.

ZipRecruiter (ZIP) has emerged as a key player with its online platform model.

This model streamlines job searching, proving effective and adaptable in the dynamic job market, especially during economic uncertainties.

Financially, ZipRecruiter is robust, with a strong balance sheet and sufficient cash flows to meet obligations.

Today, we’re delving into ZipRecruiter’s credit risk profile using Uniform Accounting to assess if rating agencies have been accurate in their evaluation of the company.

We can use Uniform Accounting to put the company’s real profitability up against its obligations and decide for ourselves the true risk of this business.

Also below is a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The job market has undergone significant changes in recent years that have disrupted the traditional recruitment process.

Macroeconomic headwinds like corporate layoffs, the Great Resignation, and the looming recession have added pressure. At the same time, technological advancements have enabled new models for connecting employers and job seekers.

This dynamic environment represents an evolution from old ways of searching for work.

Companies and talent must adapt to shifting conditions through innovative approaches. One company at the forefront of this transformation is ZipRecruiter (ZIP), leveraging its online platform model.

Ziprecruiter has positioned itself as a strategic platform that streamlines the job search process. By maintaining core capabilities on its digital marketplace while outsourcing other functions, ZipRecruiter provides a scalable and cost-efficient solution.

This “platform-as-a-service” model allows agile response to market changes. It has proven integral to ZipRecruiter’s growth, with the company connecting many employers to candidates through its easy-to-use platform.

Furthermore; contrary to expectations, periods of economic uncertainty often drive demand for job search assistance. As workers seek new opportunities amid layoffs, resignations, and recession worries, ZipRecruiter’s services will remain relevant.

The company’s platform model is well-suited for this dynamic environment. ZipRecruiter can quickly adjust its offerings and match labor supply/demand as conditions evolve.

This strategic alignment positions ZipRecruiter for continued usage in the transforming job market.

Financially, ZipRecruiter has demonstrated resilience.

It maintains a robust balance sheet with limited obligations, showing resilience during past downturns.

However, rating agencies tend to focus narrowly on short-term industry cycles rather than long-term strategic positioning.

Therefore, S&P gives the company a “BB-” rating, indicating a significant risk of default at nearly 11% over the next five years. It also puts the company in the risky high-yield basket.

Given its solid financial standing, we believe ZipRecruiter deserves a more secure rating.

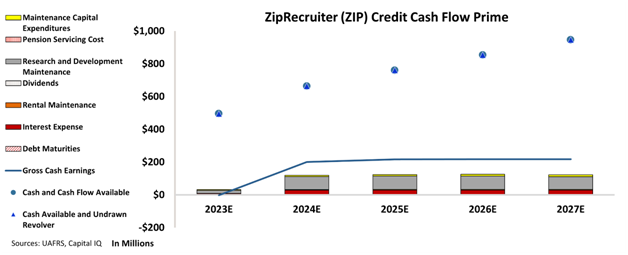

We can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (“CCFP”) to understand how the company’s obligations match against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

The CCFP chart shows that ZipRecruiter’s cash flows are more than enough to serve all its obligations going forward.

The chart suggests that the company has a strong financial footing and should be able to meet its obligations without difficulty over the next five years.

The company has no debt maturities coming in the next 5 years and its substantial cash flows should easily cover all of its obligations.

Moreover, the company’s significant role as a pioneer in online recruiting and recent strategic shifts are likely to boost future cash generation, in line with current market trends.

Our review of ZipRecruiter shows that the company has a low risk of default, contrary to what rating agencies indicate.

Therefore, we are assigning an “IG4+” rating to the company, which places it in the investment-grade basket, with a risk of default of only about 2%.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and ZipRecruiter (ZIP:USA) Tearsheet

As the Uniform Accounting tearsheet for ZipRecruiter (ZIP:USA) highlights, the Uniform P/E trades at 13.7x, which is below the global corporate average of 22.4x, but above its historical P/E of 10.9x.

Low P/Es require low EPS growth to sustain them. In the case of ZipRecruiter, the company has recently shown a 179% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations, that in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ZipRecruiter’s Wall Street analyst-driven forecast is for a 25% and 26% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ZipRecruiter’s $14 stock price. These are often referred to as market-embedded expectations.

Furthermore, the company’s earning power in 2022 was 10x the long-run corporate average. Moreover, cash flows and cash on hand are 6x its total obligations—including debt maturities and capex maintenance. The company also has an intrinsic credit risk that is 230bps above the risk-free rate.

Overall, this signals a moderate credit risk.

Lastly, ZipRecruiter’s Uniform earnings growth is in line with its peer averages and is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research