Being the pioneer of the SaaS model in the software industry paid off for this company, with Uniform Accounting illustrating returns as high as 60%

This software company is known for its creative applications that have become staples for multimedia artists everywhere. However, payments for a perpetual license of its software were too expensive for users, discouraging upgrades and creating cyclical profitability for the firm.

As a solution, the company took a huge risk and became the pioneer of the software-as-a-service (SaaS) model in the software industry. User costs were lower upfront, and the company enjoyed better, less cyclical returns.

While as-reported data suggests that this transformation strategy was not as beneficial to the company’s profitability as it expected, Uniform Accounting shows that it has actually helped generate robust Uniform ROAs of more than 60%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Back in the early 1980s, printing wasn’t as simple and developed as it is now. Publishing systems often depended on manual processes to put their work into print. On top of that, compatibility issues between computers and printing systems made the process a lot more tedious.

That is, until Dr. Charles Geschke and John Warnock developed Xerox’s page-description language, Interpress, as a solution to their printing problems. This language enabled the user to digitally print their work using a Xerox laser printer.

The idea was well-received by some of their colleagues within the corporation. Nonetheless, their motion to bring the technology to market was declined. The two scientists then decided to quit their jobs and start their own company, Adobe Inc. (ADBE).

They went ahead with their original idea to revolutionize printing technology by developing a language similar to Interpress, which they named Adobe PostScript, in 1984. This became the first printing software to allow customers to print exact pages from the computer that included text, line art, and photos.

It was a huge gamble for Adobe considering that it was the first product of its kind to hit the commercial market. A year later, the company partnered with Apple’s LaserWriter and Aldus’ PageMaker, kick-starting the desktop publishing revolution and PostScript’s eventual success.

PostScript became a standard language in the industry, and Adobe continued its path to success with the development of more than 400 third-party software programs. Some of the more popular ones are Adobe Illustrator, Adobe Photoshop, Indesign, and Adobe Premier—all of which were developed to further expand the company’s product suite and branch out into the creative software market.

Adobe also made a few bolt-on acquisitions to complement their growing product lines, including PageMaker creator Aldus, graphics company Macromedia, and web analytics firm Omniture.

The company’s comprehensive content creation software products have consistently dominated the creative market, in graphics specifically, with Photoshop, Indesign, and Illustrator collectively taking 90% of the industry’s market share. It’s no wonder these tools have become staples in the world of multimedia.

Adobe was able to sustain its competitive edge with its strong brand identity and consistent product improvement through updates. However, as essential as these tools are, users were inclined to avoid making upgrades because of how expensive the bundles were.

This was a problem not only for the users, but for the company as well. Using a perpetual license model, users would cash out one time to be able to use the software forever. In turn, it caused the company to have very cyclical profitability.

As a solution, Adobe took another big gamble in 2013. Similar to the risk that the company took when it commercialized its printing technology, it decided to switch from a perpetual license model to a subscription-as-a-service (SaaS) model.

So now, from a one-time purchase of $1,800, Adobe is able to charge its annual subscribers only $50 per month for the whole Creative Cloud bundle (consisting of Photoshop and its other products), or around $20 per month for its single app plan. This is a much lower upfront cost to consumers, and it includes continuous updates and support so long as you remain a subscriber.

This transformation strategy, however a big of a risk it was, has paid off significantly. In fact, this strategy has become so successful that in the investment community and in the software community, most people immediately understand what you’re saying when you say a company is “going through the Adobe” conversion.

Previously, we’ve talked about how companies like Atlassian and Activision Blizzard “went Adobe” and generated massive returns as a result. For Adobe, the success of the transformation strategy isn’t apparent at all when looking at as-reported metrics.

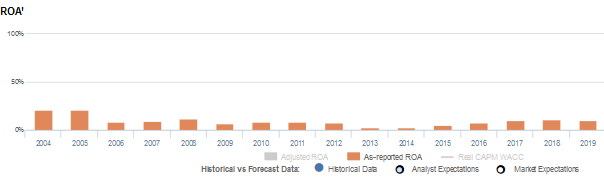

Specifically, as-reported return on assets (ROAs) have been fairly weak, ranging only from 3%-21% levels since 2004. Looking only at these returns would have you question why software companies have adopted the SaaS model so feverishly.

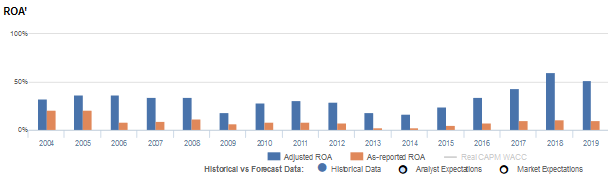

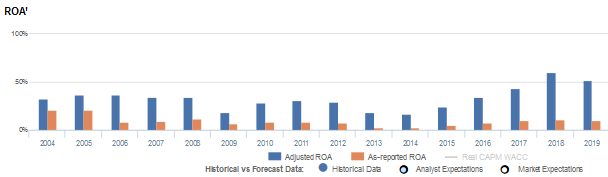

In reality, the success of Adobe’s strategic shift is portrayed more accurately by Uniform ROAs, which have gone up to 50%-60% in recent years—almost twice the previous highs of 30%!

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Adobe’s balance sheet. In recent years, goodwill has sat at about $5 billion to $11 billion due to the company’s series of acquisitions.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Adobe’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing consistently poor. In fact, it has been the opposite, with returns that are nearly 3x-9x greater.

Adobe’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Adobe’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 10% in 2019, but its Uniform ROA was actually over 5x higher at 52%.

Specifically, Adobe’s Uniform ROA has ranged from 16%-60% in the past sixteen years while as-reported ROA ranged only from 3%-37% in the same timeframe.

After maintaining 33%-37% levels in 2004-2008, Uniform ROA declined to 19% in 2009 before expanding to 31% in 2011. Then, it gradually compressed to 16% in 2014 and subsequently rose to a peak of 60% in 2018. Thereafter, Uniform ROA compressed to 52% in 2019.

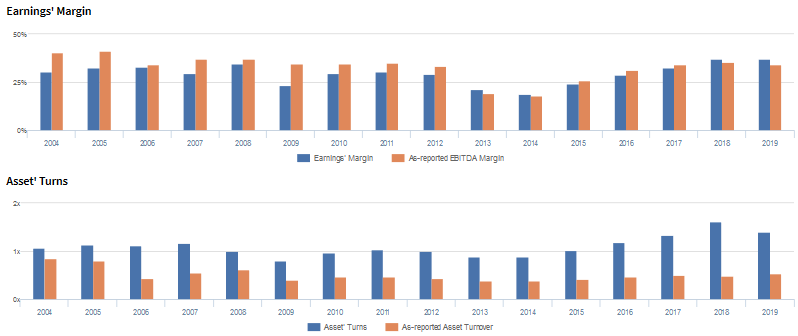

Adobe’s Uniform earnings margins are weaker than you think, but its robust Uniform asset turns make up for it

Adobe’s cyclical profitability has been driven by cyclical trends in Uniform earnings margins and to a lesser extent, Uniform asset turns.

Uniform margins reached cycle lows of 23% in 2009 and 19% in 2014, while reaching cycle highs of 35% in 2008, 30% levels in 2010-2011, and 37% levels in 2018-2019.

Meanwhile, Uniform turns improved from 1.1x to 1.2x from 2004-2007, before dropping to a trough of 0.8x in 2009 and stabilizing at 0.9x-1.0x levels through 2015. Thereafter, Uniform turns jumped to a peak of 1.6x in 2018, before compressing to 1.4x in 2019.

At current valuations, markets are pricing in an expectation for record improvements in Uniform margins and a reversal of recent declines in Uniform turns.

SUMMARY and Adobe Inc. Tearsheet

As the Uniform Accounting tearsheet for Adobe Inc. (ADBE) highlights, the Uniform P/E trades at 41.6x, which is above corporate average valuation levels and its own history.

High P/Es require high EPS growth to sustain them. In the case of Adobe, the company has recently shown a 24% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Adobe’s Wall Street analyst-driven forecast is a 44% EPS growth in 2020, followed by a 9% EPS shrinkage in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Adobe’s $468 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 26% each year over the next three years to justify current prices. What Wall Street analysts expect for Adobe’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 9x the corporate average. Also, cash flows and cash on hand are 2x higher than its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit and dividend risk.

To conclude, Adobe’s Uniform earnings growth is above its peer averages in 2020 and the company is also trading in line with average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com