Its user-generated content model enabled this company to successfully grow and monetize its user base, leading to robust Uniform ROAs of 50%+

Digital businesses often enjoy the benefit of network effects. This means that as the number of users who contribute to a platform increases, the more valuable that platform becomes—and this online travel company has powerful network effects.

With its massive database of travel-related reviews generated by its users, the company was able to attract high traffic to its website from other users planning their trips. Once it built up a considerable user base, the company managed to successfully monetize this asset through advertising.

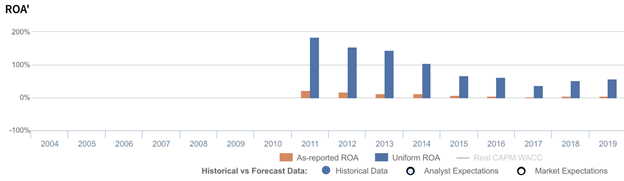

However, looking at as-reported metrics, it seems that the company has had less success from their monetization efforts than expected. In reality, Uniform Accounting uncovers the opposite, with returns that have been above 50%, and not below cost-of-capital levels.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Alibaba, Amazon, Facebook, Google, and Microsoft are five of the world’s biggest firms by market value, with a combined capitalization of about $6.5 billion. One thing these companies have in common is that they’re all digital businesses.

An example of a digital business is a company where the platform is the product and the users are the customers. In this case, user base growth becomes a critical component of a digital business’s success.

Not only that, the more users they have on their platforms, the stronger their network effects are. Having network effects means that a platform or a service becomes increasingly valuable as more participants are involved.

Take YouTube for example. The $15 billion revenue-generating machine wouldn’t be as valuable as it is without the people uploading the videos and the people watching those videos. Twitter, Facebook, and Amazon are the same; these wouldn’t be multi-billion- or trillion-dollar companies without the users who post or sell on these sites every day.

A user-generated content business model with a robust user base delivers some pretty powerful network effects. If monetized properly, it could mean massive returns for a company.

TripAdvisor (TRIP) has done exactly just that.

Co-founder of TripAdvisor Stephen Kaufer originally planned on developing a search engine focused specifically on travel-related information. In addition to the database they were building, they also added a feature where users could post their own reviews on the site.

While the search engine was a good idea, user reviews were getting all the traffic, which is why they shifted focus to that instead. This is where the network effects came in—users were generating content for the company and attracting other users as well, all for free.

It gave them the perfect opportunity to monetize the company’s high site traffic through advertisements.

TripAdvisor uses a cost-per-mille (CPM) and a cost-per-click (CPC) advertising model. Basically, the CPM model relies on ad views, where advertisers pay a certain fee for every 1,000 views. CPC, on the other hand, relies on ad clicks where payment is based on the number of people who clicked on the ad.

The CPM model is more appropriate for advertisers who only want to increase brand awareness, regardless of whether or not a user clicks through or purchases their product or service. Plus, the fees for this model are generally cheaper.

However, the CPC model, which is generally the more expensive option, is where TripAdvisor generates about 50% of its revenues. This model makes more sense for the company considering that users usually book their hotels and other travel services through the site anyway.

Overall, because of its strong network effects, massive user base, and monetization strategies, TripAdvisor, a company that started with an initial investment of $4 million, has grown to a nearly $5 billion firm with over 490 million monthly active users.

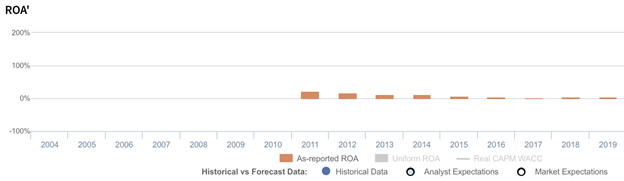

However, looking at as-reported metrics, TripAdvisor doesn’t seem to be as profitable as one might expect. As-reported ROAs over the past five years have been below cost-of-capital levels.

Uniform Accounting, on the other hand, reveals exactly just how successful the company has been at monetizing its user base assets, with Uniform ROAs ranging from 36% to as high as 184%.

Although returns are still robust, growing competition around the digital travel services space from competitors such as Expedia, Booking, and until recently, Google, have shrunk TripAdvisor’s Uniform ROAs.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on TripAdvisor’s balance sheet. In recent years, goodwill sits at about $800 million, arising from the acquisition of travel-related companies to enhance and add on to its services.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of TripAdvisor’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing poorly. In fact, it has been the opposite, with returns that are nearly 8x-13x greater.

TripAdvisor’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

TripAdvisor’s Uniform ROA has actually been higher than its as-reported ROA in the past nine years. For example, as-reported ROA was 6% in 2019, but its Uniform ROA was actually nearly 10x higher at 58%.

Specifically, TripAdvisor’s Uniform ROA has ranged from 36% to 184% in the past nine years while as-reported ROA ranged only from 3% to 22% in the same timeframe. Uniform ROA declined from 184% in 2011 to 36% in 2017, before expanding to 58% in 2019.

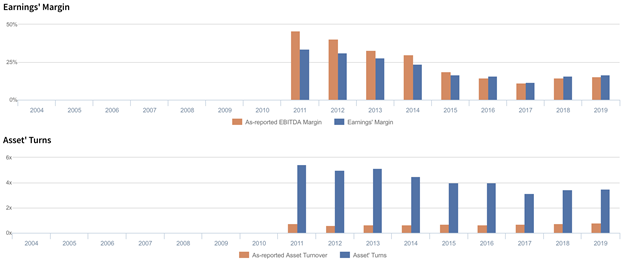

TripAdvisor’s Uniform earnings margins are generally weaker than you think, but its Uniform asset turns make up for it

TripAdvisor’s overall profitability trends have been driven by trends in Uniform earnings margins, coupled with stable Uniform asset turns.

Uniform margins steadily fell from 34% in 2011 to 12% in 2017, before expanding to 17% in 2019. Uniform turns followed a similar trend, falling from 5.4x in 2011 to 3.1x in 2017, before improving slightly to 3.5x in 2019.

At current valuations, the market is pricing in expectations for Uniform margins and Uniform turns to sustain current levels.

SUMMARY and TripAdvisor Tearsheet

As the Uniform Accounting tearsheet for TripAdvisor, Inc. (TRIP) highlights, the Uniform P/E trades at -67.8x, which is below the global corporate average of 25.2x, and its historical average Uniform P/E of -9.9x. Prior to the pandemic, its average Uniform P/E was 32.1x.

Low P/Es require low EPS growth to sustain them. In the case of TripAdvisor, the company has recently shown a 4% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, TripAdvisor’s Wall Street analyst-driven forecast is a 198% and an 87% EPS shrinkage in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify TripAdvisor’s $36 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 5% per year over the next three years to justify current stock prices. What Wall Street analysts expect for TripAdvisor’s earnings growth is well below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 10x the corporate average. Also, cash flows and cash on hand are about 3x higher than its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, TripAdvisor’s Uniform earnings growth is below its peer averages, and the company is also trading below its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com