Mastering the way of snacking earned this confectionery a jawbreaking position in the industry, attaining recent Uniform ROAs of 20%+

Today’s often busier lifestyles have influenced people’s eating patterns. The traditional three square meals a day now includes one or more snacks in between to satisfy hunger or cravings, control moods, as well as for other psychological reasons.

This company spun off from another big food company in order to focus on its snacking business. It further strengthened its portfolio through brand acquisitions and product improvement, as well as by expanding into the healthy snack market.

However, as-reported data suggests that these initiatives have not been generating robust returns for the company. In reality, Uniform Accounting shows that it has actually helped achieve Uniform ROAs of more than 20%, which are at least twice its recent as-reported numbers.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

What’s a Netflix movie marathon without a large bowl of popcorn?

Popcorn is an ideal snack for watching movies because it’s easy to eat—you don’t need utensils for it and it doesn’t distract you from the movie. But popcorn or any other easy-to-consume food like chips or candy bars have become a bigger part of one’s day, not just as a snack to eat with an accompanying movie.

There are a lot of reasons why people snack. It could be to satisfy cravings or hunger, or for psychological reasons such as dealing with moods and emotions, and combating boredom.

Snacking has increased during the pandemic lockdowns, mostly because consumers now have freedom and control over their snack supply and when they snack, as opposed to office spaces or schools where both time and snacks are likely limited.

However, snacking has been on the rise for quite some time now. Global calorie intake, largely attributable to snacking, has seen a massive increase from the early 60s up to now. Snacking meets the evolving needs of an on-the-go society where a traditional sit-and-dine scenario outside of breakfast, lunch, and dinner would be too inconvenient.

Overall, the snacking industry has grown to a $210 billion industry, which is set to reach $265 billion by 2023.

Mondelez International, Inc. (MDLZ) has benefitted from the growth in the snacking industry, and stands to gain more going forward.

Originally named Cadbury, Mondelez was acquired by Kraft in 2010 and subsequently spun off in 2012 to separate Mondelez’s high-growth snacks business from Kraft’s slower-growth grocery business.

The spin-off presented Mondelez an opportunity to strengthen its position in the snacking industry with increased focus on their snack brands and international confections. The spin-off also improved Mondelez’s ability to achieve its strategic priorities through brand strengthening, brand acquisitions, and even digital transformation.

The company’s decision to split came at the right time as one key growth opportunity for the snacking industry lies in functional ingredients and organic foods since health-conscious consumerism had begun to rise.

Mondelez recognized the increase in demand for healthy snack alternatives, a market expected to grow to $32 billion by 2025.

The company reestablished its core portfolio by developing its well-being brands. It strengthened this segment through product innovation by making thinner, smaller, and less sweet snacks. It also sought to reduce sodium and saturated fat content in its products, and introduced lactose-free and gluten-free snacks.

Furthermore, considering that well-being snacks are a significant aspect for growth opportunities, Mondelez has committed to increasing its portfolio at twice the average rate through a series of planned acquisitions over the next five years.

However, as-reported metrics make it look like Mondelez isn’t the high-growth snacking business that it is. Specifically, focusing on product innovation and keeping up with the healthy snack trends has only led to flat, below cost of capital as-reported returns for the company.

In reality, robust, improving Uniform ROAs of more than 20% prove that snacking is in fact a high-growth industry, with Mondelez successfully adapting to its consumers’ preferences to take advantage of secular growth trends.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Mondelez’s balance sheet. In recent years, goodwill sits at about $20 billion to $21 billion, the firm’s largest long-term asset, stemming from the company’s acquisitions to expand its portfolio.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Mondelez’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing poorly. In fact, it has been the opposite, with returns that are nearly 6x-9x greater.

Mondelez’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Mondelez’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 4% in 2019, but its Uniform ROA was actually 9x higher at 36%.

Specifically, Mondelez’s Uniform ROA has ranged from 14% to 36% in the past sixteen years while as-reported ROA ranged only from 3% to 6% in the same timeframe.

After expanding from 17% in 2004 to 22% levels in 2005-2006, Uniform ROA declined to a low of 14% in 2010 before jumping to 25% in 2013. Then, it compressed to 20% in 2014 and subsequently expanded to 36% in 2020.

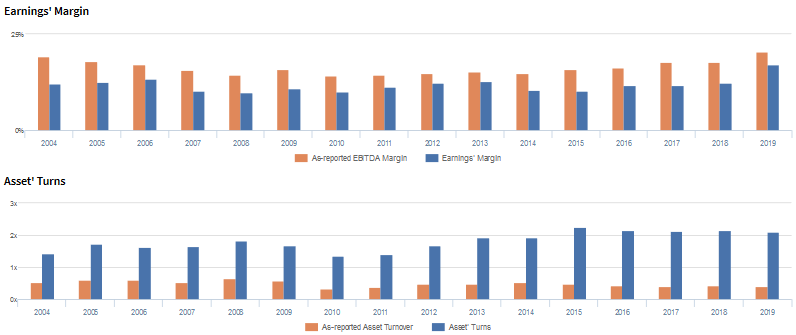

Mondelez’s Uniform earnings margins are generally weaker than you think, but its Uniform asset turns more than make up for it

Mondelez’s trends in Uniform ROA have been driven largely by trends in Uniform asset turns, and to a lesser extent, Uniform earnings margins.

After maintaining 12%-13% levels in 2004-2006, Uniform margins fell to 10% levels in 2007-2008 before gradually expanding to 13% in 2013. Thereafter, Uniform margins declined back to 10% in 2015, but subsequently expanded to a peak of 17% in 2019.

Meanwhile, Uniform turns improved from 1.4x in 2004 to 1.8x in 2008, before falling back to 1.4x in 2010-2011 and recovering to a peak of 2.2x in 2015. Since then, Uniform turns have compressed to 2.1x levels in 2017-2019.

At current valuations, markets are pricing in expectations for both Uniform margins and turns to expand to new peaks.

SUMMARY and Mondelez Tearsheet

As the Uniform Accounting tearsheet for Mondelez International, Inc. (MDLZ) highlights, the Uniform P/E trades at 24.6x, which is around corporate average valuation levels and its own recent history.

Average P/Es require average EPS growth to sustain them. In the case of Mondelez, the company has recently shown a 43% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Mondelez’s Wall Street analyst-driven forecast is an 18% EPS shrinkage in 2020 and a 15% EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Mondelez’s $57 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 1% each year over the next three years to justify current prices. What Wall Street analysts expect for Mondelez’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 6x the corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a moderate credit and dividend risk.

To conclude, Mondelez’s Uniform earnings growth is well below its peer averages in 2020, but the company is trading well above its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com