MONDAY MACRO: Credit bank officers are too pessimistic on aggregate credit outlook. UAFRS numbers say otherwise

Philippine inflation reached a 6-month low at 2.2% this past April. Given low economic activity in the past three months due to the adverse effect of the COVID-19 pandemic, it is unsurprising that this is its third consecutive drop.

The Bangko Sentral ng Pilipinas (BSP) has implemented a number of monetary policies to manage inflation amidst the pandemic. These include policy rate cuts, lower reserve requirements, and lower credit risk weights on Micro, Small, and Medium Enterprises (MSME) loans.

However, will the BSP’s efforts in this low inflationary environment be enough to stimulate growth in the Philippine economy? Or are we heading straight for a recession?

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

The BSP’s latest Senior Bank Loan Officers’ Survey (SLOS) showed another quarter of net credit standards tightening. The survey results indicated that more banks were less likely to process loans for both enterprises and households for Q1 2020.

As discussed, in our Monday Macro Report on SLOS, when banks tighten their lending standards, it becomes harder for businesses to access money to either fund their growth or continue operating.

It’s not surprising that banks remain cautious about lending during this global health crisis. With the major cities of commerce still on limited operations due to the quarantine, there is already uncertainty about companies’ ability to pay their current debt obligations.

SLOS respondents also indicated a persistent view on stricter financial system regulations and reduced tolerance for risk for Q2 2020. It makes sense then that even with lower borrowing costs from BSP cutting interest rates by 43 basis points (bps) or 0.43% in Q1 2020, net credit standards did not ease.

One of the tools of BSP is policy rates, which it can use to monitor and adjust the financing cost levels of borrowers. BSP modifies interest rates to manage inflation as part of their mandate to achieve price stability.

Higher policy rate leads to more expensive loans offered by banks, which translates to lower spending levels in an economy. Conversely, a lower rate leads to spending increases, which in effect results in an increase in prices, or higher inflation.

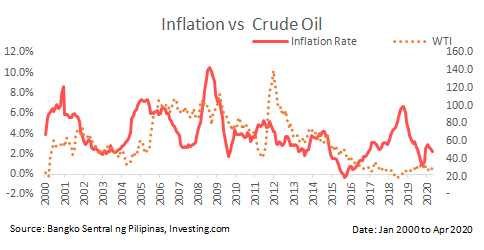

Looking back at the Philippines’ inflation during the 2008-2009 Global Financial Crisis, the inflation rate reached a high of 10% due to elevated world oil prices.

A high inflationary environment prompted BSP to increase the policy rate to temper down price growth.

However, the relationship between inflation and oil prices did not hold in 2012. We saw inflation rate ranged from 2.8% to 4.1%, despite WTI crude oil reaching a new high of $140 per barrel.

Lower prices of majority food items due to favorable domestic supply conditions and lower electricity rates were cited sources by BSP of low inflation at that time.

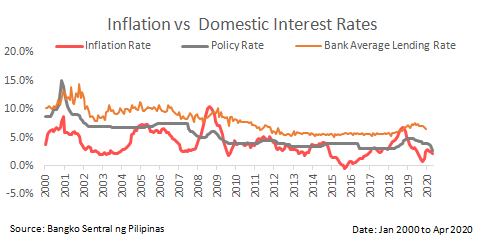

Given that inflation rates have an inverse relationship with interest rates, using policy cuts under a high inflationary environment may be a cause of concern.

However, as of April 2020, the inflation rate is at 2.2% which is within the central bank’s 2020 inflation target of 1.8% to 3.8%. This low inflationary environment gives BSP room to conduct further policy rate cuts when needed.

This year, the BSP has lowered the policy rate to an all-time low of cutting to a total of 120bps.

In 2019, the Philippine banks’ average lending rate rose to as high as 7.5% in May 2019 before dropping down to 6.5% in December 2019. This is, however, still above the 10-year average of 6.1%, which gives BSP room to implement more interest rate cuts.

The current low inflationary environment is expected to persist in the near-term, given oil price outlook and muted consumption demand caused by lay-offs and underemployment.

We can still expect an improvement in credit circulation, given the current efforts of BSP.

Moreover, other liquidity enhancement measures done by the central bank are looser reserve requirement ratio and reduced credit risk weights on MSME loans.

These initiatives were taken to improve credit flow in the financial system. However, given the tightening of credit standards from more banks, BSP may need to provide additional stimulus to the economy.

Additionally, BSP still has ways to support the economy through interest rate cuts. The current bank lending rate levels and a stable low inflationary environment make this possible without harming the economy. Credit standards easing initiatives will become more effective once the banks’ outlook brightens.

Furthermore, as we discussed in our previous Monday Macro report, the largest Philippine companies continue to enjoy a healthy cash profile for the next five years. This indicates that any recession will not be caused by a credit crisis. If a recession should occur, the Philippines’ largest companies have enough liquidity to continue operating in an economic slowdown.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com