MONDAY MACRO: Declining aggregate recovery rate may be a concern for the Philippines, despite an A credit rating; steady 6% Uniform ROA says otherwise

In 1993, S&P and Moody’s gave the Philippines its first credit rating of BB- and Ba2, respectively. In 1999, Fitch gave a credit rating of BB+ for the country.

It was only in 2013 when the Philippines’ credit rating finally reached investment grade. Fitch gave a BBB- rating on account of a robust economy and improved fiscal management.

The metric we are highlighting in this report will provide insight on the Philippines’ debt condition amidst a growing economy.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

A sovereign credit rating is used to determine the country’s borrowing costs in the international capital market.

Locally, it affects private borrowing costs as it becomes the ceiling for ratings given to companies. It also helps institutional investors determine their appetite for a country’s financial instruments.

In April 2019, Standard and Poor’s Global Ratings (S&P) upgraded the Philippines’ credit rating to BBB+, the highest credit rating in Philippine history. S&P cited consistent economic growth, robust fiscal measures, and sustainable public finances as the main reasons behind the upgrade.

S&P is one of the Big Three global credit rating agencies that rate a country’s ability to pay back debt by ensuring principal and interest payments. The other two global agencies are Moody’s Investors Service (Moody’s) and Fitch Ratings (Fitch).

Both Moody’s and Fitch have had a medium investment grade rating with a moderate credit risk for the country, both just two notches away from an A credit rating.

Last February 11, 2020, Fitch upgraded their expectations to a positive outlook from stable, banking on continued economic growth and moderate inflation. They are also expecting government debt to remain within manageable levels.

This outlook upgrade indicates that Fitch may upgrade its rating on Philippine sovereign debt within one or two years.

Usually, having an A credit rating means that the country would enjoy a lower cost of borrowing for the public and private sectors. This could also attract foreign funds that invest exclusively in A-rated countries.

Though an investment grade rating sounds good for the country, keep in mind that credit ratings agencies have not always provided reliable information. The International Monetary Fund has criticized credit ratings agencies in the past because of their hand in the 2008 global financial crisis, particularly in their failure to properly rate subprime mortgage-backed securities.

Key factors that credit ratings agencies consider for their sovereign credit ratings are qualitative factors such as fiscal and monetary strength, economic growth, a track record of honoring their debt, and quantitative factors such as the level of debt, and structure of government debt.

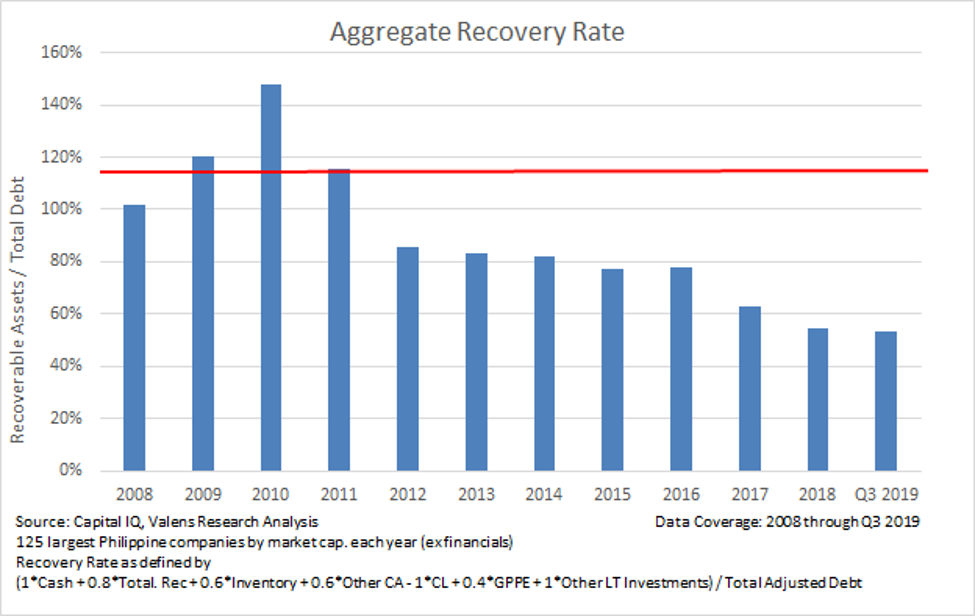

Uniform Accounting, on the other hand, lets the numbers speak for themselves. Our aggregate recovery rate analysis using Uniform data shows that despite economic growth, we still need to watch out for the level of total debt.

The Aggregate Recovery Rate shows firms’ ability to cover debt payments using their asset base.

Recoverable assets, which include cash, total receivables, inventory, other current assets (less current liabilities), gross PP&E, and other long-term investments, are the numerator, while the denominator is total adjusted debt.

We get the aggregate recovery rate by adding the recoverable assets of 125 of the largest publicly-listed companies in the Philippines and dividing that by the total debt of those same 125 companies.

From 2008 to 2011, the aggregate recovery rate was above 100%, peaking at 137% in 2010. But in 2012, it fell below 100%. It hasn’t reached 100% levels since then.

The recent decline was caused by the growth of total debt outpacing recoverable assets growth, which should be monitored given that current levels are at its lowest in the last decade

A similar trend can be seen for some of the Philippines’ major trading partners and peers.

Singapore’s aggregate recovery rate fell from a peak of 118% in 2016 to 50% in 2018, while the US fell to a decade low of 70% by mid-2019.

Just like in the Philippines, the recent drop from their recent highs was driven by a much faster growth in total debt than growth in recoverable assets.

A declining aggregate recovery rate may increase risk for access to credit markets for refinancing as needed in the long term.

But as our Monday Macro Report on the Philippines’ credit profile explains, a sizable amount of cash is still available for outlays for the largest Philippine companies, which should cover their obligations and debt maturities even when their Uniform gross earnings cannot.

With no catalyst for credit destruction for the Philippine Composite Index and with proper fiscal sustainability from the government’s tax reforms, an upgrade to an A credit rating is warranted.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com