Strengthening its digital marketing helped this company cope with the changing environment, leading to a 7% Uniform ROA

2020 was a year full of uncertainties and changes brought by the pandemic. There was a massive shift in how people live, work, and entertain themselves. This also led to a tremendous change in consumer behavior, particularly in the snacking market.

This snacking company channeled its efforts into strengthening brand awareness. However, looking at its as-reported metrics, it seems that focusing on this strategy hasn’t been beneficial to the company’s profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

With nowhere else to go and not much to do during the lockdowns, people stuck at home turned to snacking to alleviate their boredom, to take their mind off their worries, or to partner with their binge watching sessions.

In a past Thursday PMD article, we talked about how Mondelez (MDLZ:USA) benefited from the upward trend in the snacking industry during the pandemic. Today, we are going to talk about another company that was able to ride the wave and succeed, Universal Robina Corporation (URC:PHL).

Through the years, URC has continued to develop its strongest brands in the market—Jack ‘n Jill for snack-foods, C2 for ready-to-drink tea, and Great Taste for coffee—and has become the company that has some of the most sought-after products in the ASEAN region.

In addition, the snack manufacturer also formed joint ventures with Calbee and Danone, giving its consumers new options and flavors, as well as offering them more on-the-go and better-for-you (BFY) products.

It also acquired Griffin’s Food Company in New Zealand in 2014, which enabled URC to bring Nice & Natural, a healthy snacks company, to the Philippines.

One of the keys to the company’s success is its intense focus on brand marketing. Compared to its public peers, URC dedicates 76% of its selling general and administrative expenses to its marketing and advertising efforts.

Even with a lot of budget, it’s imperative to have the right marketing strategies in place to reach and encourage its target customers to purchase its products.

That is why URC has been pretty consistent in employing continuous advertisements, particularly with its potato chip brand Piattos. Among all its potato chip products, Piattos receives the most frequent advertising exposure, with a new marketing campaign being launched every two years since 2009.

However, because of the pandemic, URC had to rethink its usual marketing methods to reach its target market.

Hence, the company had to shift its focus on social media platforms, particularly Facebook (FB:USA).

Since the Philippines is considered the “social networking capital of the world,” it is safe to say that pairing with the social media giant has proven, and will continue to prove beneficial to the snacks maker.

The shift to digital was not difficult for the company because it had collaborated with Facebook in the past. It is proving to be an additional opportunity to gain a better advantage with its marketing and advertising initiatives by allowing the company to learn more about recent trends and practices.

For example, URC agreed to participate in Facebook’s Brand Lift study by launching a four-week regional-specific broadcast of C2’s advertisement, coupled with Facebook’s location targeting feature.

This was deemed successful as the Brand Lift study’s results showed that there was a 2.3x increase in brand familiarity, which in turn, contributed to the 48% increase in purchase intent for URC’s products.

On top of that, the company also delved into the e-commerce space by making its products available online through different platforms like Shopee, Lazada, and Zalora, to name a few.

Besides helping the company’s business, developing its e-commerce also accentuated URC’s other goal, which was to make shopping convenient for its customers. Today, consumers can just easily click “add to cart” in order to get all of their favorite URC products.

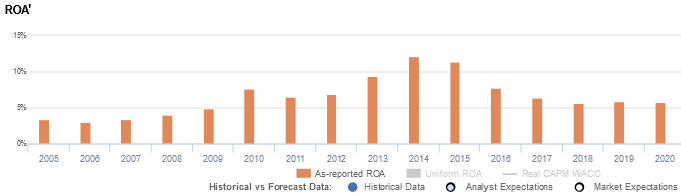

For years, URC’s focus on its marketing and advertising strategies has been keeping the company’s products top of mind for consumers. However, as-reported data seem to suggest that these initiatives weren’t enough to increase its profitability in the long-run, with ROAs falling severely from 12% in 2014 to 6% in 2020 after its acquisition of Griffin’s Food Company.

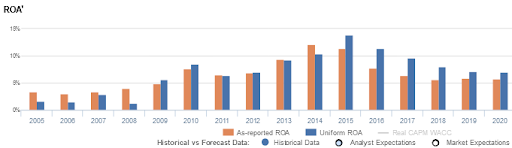

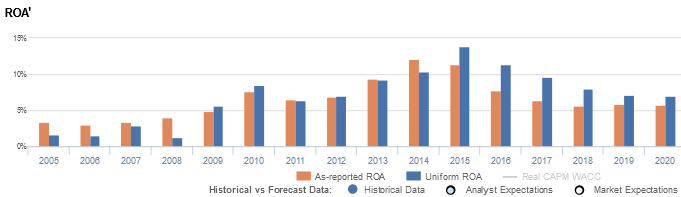

In reality, although URC saw declining returns as the firm expanded its global operations, the firm’s Uniform data still fared better than its as-reported, with profitability ranging from 7%-14% in recent years.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on URC’s balance sheet. The company’s goodwill sits at about PHP 31.2 billion in recent years, which was approximately one-third of its total assets, stemming from the acquisitions over the course of its operations.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of URC’s earning power. Specifically, if we remove goodwill along with the other necessary adjustments in Uniform Accounting in 2020, Universal Robina Corporation should be recognizing PHP 36 billion less in assets and a 7% Uniform ROA.

URC’s recent earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that URC is a much weaker business than real economic metrics highlight.

URC’s Uniform ROA has actually been higher than its as-reported ROA for the past five years. For example, as-reported ROA was 11% in 2015, but Uniform ROA is displaying stronger profitability at 14%.

Historically, as-reported ROA was maintained at 3%-4% levels from 2005-2007, before improving to 8% in 2010 and subsequently contracting to 6% levels in 2011. Thereafter, as-reported ROA rose to a peak of 12% in 2014, before regressing to 6% levels from 2017-2020.

Uniform ROAs followed a similar trend. After fading from 3% in 2007 to a low of 1% in 2008, Uniform ROA jumped to 9% in 2010, before compressing to 6% in 2011. Then, Uniform ROA expanded to a peak of 14% in 2015, before falling to just 7% in 2020.

URC’s recent asset utilization is more efficient than you think

URC’s recent performance has been driven primarily by stronger Uniform asset turns, a key driver of profitability.

From 2005-2007, as-reported asset turnover remained at 0.6x levels, before expanding to 1.2x peaks in 2013-2014 and subsequently fading to 0.7x in 2020.

Meanwhile, after sustaining 0.7x levels from 2005-2008, Uniform turns soared to a high of 1.2x in 2015, before contracting to 0.9x in 2020.

As-reported metrics are making the firm appear to be a less asset efficient business than real economic metrics highlight.

SUMMARY and Universal Robina Corporation Tearsheet

As the Uniform Accounting tearsheet for Universal Robina Corporation (URC:PHL) highlights, it trades at a Uniform P/E of 28.5x, above the global corporate average of 23.7x, but below its historical average of 32.4x.

High P/Es require high EPS growth to sustain them. In the case of URC, the company has recently shown a 4% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, URC’s sell-side analyst-driven forecast calls for a 30% and 7% Uniform EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify URC’s PHP 142.00 stock price. These are often referred to as market embedded expectations.

URC is currently being valued as if Uniform earnings were to grow 12% annually over the next three years. What sell-side analysts expect for URC’s earnings growth is above what the current stock market valuation requires in 2021, but below the requirement in 2022.

Furthermore, the company’s earning power is above the long-run corporate average, and cash flows and cash on hand are also above total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, URC’s Uniform earnings growth is in line with its peer averages, but the company is trading way above its average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com