Uniform Accounting reveals the growth potential of this mutual fund that as-reported metrics cannot.

This asset management firm offers an online investing platform that allows users to invest in their funds. One of these funds focuses on investing in growth companies not listed in the Philippine Stock Exchange Index (PSEi).

Under as-reported metrics, investors will not see the growth potential of this fund’s holdings. However, Uniform Accounting shows the reality of companies they invest in and how they fit into the firm’s investment strategy.

In addition to examining the fund’s portfolio, we’re including fundamental analysis of one of the fund’s largest holdings, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Philippine Markets Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Last February, we highlighted Seedbox, ATR Asset Management’s (ATRAM) online investing platform that can be accessed through computers and smartphones. Through Seedbox, users are able to invest in ATRAM’s mutual funds and unit investment trust funds (UITFs).

This week’s focus is on one of ATRAM’s newest mutual funds, ATRAM Alpha Opportunity Equity Fund. As its name would suggest, this fund’s goal is to find alpha, which is the measure of a fund’s excess return over its expected return.

The fund aims to achieve alpha by investing in companies with potential for strong growth, which are not necessarily part of the Philippine Stock Exchange index (PSEi).

ATRAM Alpha Opportunity Equity Fund started with a net asset value per unit (NAVPU) of PHP 1.13 in September 2012, the fund’s inception date. After slowly rising to PHP 1.67 in January 2015, the fund’s NAVPU dropped all the way down to PHP 1.00 a year later, a loss of 40%. The PSEi, meanwhile, outperformed the fund with a loss of 17% in the same time span.

Afterwards, the fund reached a peak of PHP 1.68 in July 2019, before settling down to PHP 1.38 by the end of the year. Comparatively, PSEi’s loss of 5% outperformed the fund’s loss of 18%.

Year to date (YTD), the fund and PSEi incurred losses of 33% and 28%, respectively, due to concerns about the COVID-19 pandemic. Since most of the fund’s holdings are in industries affected by the pandemic such as consumers discretionary and industrials, market price volatility is expected to persist in the short run.

That said, companies with strong growth potential and solid business models tend to endure tough times and deliver high-quality performance over the long term.

Analyzing ATRAM Alpha Opportunity Fund using as-reported figures, it is not obvious that they picked companies with strong growth potential and solid business models.

As-reported numbers would have investors incorrectly believe that these companies are low-quality. This could lead to skewed insights, negatively affecting the entire investment decision making process.

However, Uniform Accounting paints a very different picture. With Uniform Accounting metrics, investors can see the true underlying performance and earnings growth potential of companies.

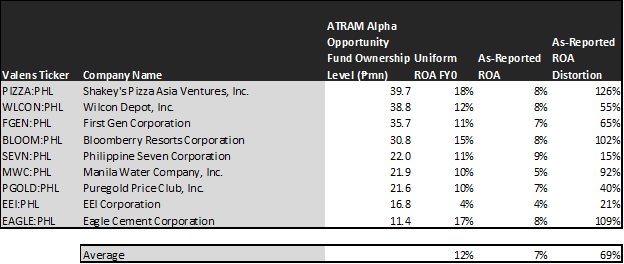

The table below lists the top non-financial holdings of ATRAM Alpha Opportunity Fund along with their Uniform return on assets (ROA), as-reported ROA, and ROA distortion—the difference between Uniform and as-reported ROA.

Most of ATRAM Alpha Opportunity Fund’s holdings show as-reported returns that range around global cost-of-capital levels, suggesting that they are not generating economic profit. However, Uniform Accounting reveals that in reality, the majority of these companies have above-average profitability.

In turn, traditional metrics would have investors believe that this fund is subpar with an average as-reported ROA of 7%, barely above global corporate average returns of 6%. But the reality is, under the Uniform Accounting framework, the companies’ in the fund’s portfolio display a robust average Uniform ROA of 12%.

Uniform Accounting adjusts for the misrepresentations in companies’ financial statements brought about by the inconsistencies in the Philippine Financial Reporting Standards (PFRS) to reveal the true underlying performance of companies.

As such, it should not be surprising that when analyzing the non-financial holdings of ATRAM Alpha Opportunity Fund, the figures that easily stand out are the double-digit discrepancies between Uniform ROA and as-reported ROA for these companies.

While at a glance, the difference between as-reported ROA and Uniform ROA may not seem that great, the distortion in percentage ranges from 15% to 126%, with Shakey’s Pizza Asia Ventures, Inc. (PIZZA:PHL), Eagle Cement Corporation (EAGLE:PHL), and Bloomberry Resorts Corporation (BLOOM:PHL) all having distortions above a hundred percent.

As-reported ROA understates the earning power of PIZZA, suggesting that this company is an average firm with an 8% as-reported ROA. In reality, this company is a high-quality firm with an 18% Uniform ROA, thrice the global corporate average returns.

Similarly, as-reported numbers incorrectly treat EAGLE as an average company with an as-reported ROA of 8%. In reality, it is an above-average firm with a 17% Uniform ROA.

By focusing on as-reported metrics alone, ATRAM would never pick most of these companies because they look like anything but high-quality companies with profitable business models.

However, to find companies that can deliver alpha, it is insufficient to just look at companies using as-reported metrics since they misrepresent a company’s real profitability.

To generate alpha, any investor must also identify if the market is significantly undervaluing the company’s potential.

ATRAM Alpha Opportunity Fund is invested in companies with unreasonably low market expectations.

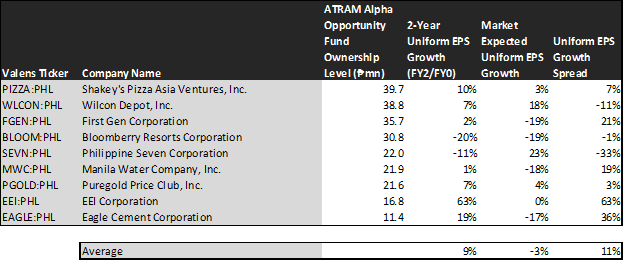

This table shows the earnings growth expectations for the major company ownerships of ATRAM Alpha Opportunity Fund. It features three key data points:

- The 2-year Uniform EPS growth represents the Uniform earnings growth the company is likely to have for the next two years. The earnings number used is the value of when we convert consensus sell-side analyst estimates to the Uniform Accounting framework.

- The market expected Uniform EPS growth represents what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next two years to justify the current stock price of the company. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the difference between the 2-year Uniform EPS growth and market expected Uniform EPS growth.

On average, Philippine companies are expected to have 6% annual Uniform earnings growth over the next two years. However, the market sees a decline in earnings for these companies with market-expected Uniform EPS shrinkage of 3% over the next two years.

In reality, ATRAM Alpha Opportunity Fund’s top holdings are forecast to deliver strong 9% Uniform earnings growth in the next two years.

Among these companies, EEI Corporation (EEI:PHL) and EAGLE have the highest Uniform earnings growth dislocation.

The market is mispricing EEI’s Uniform earnings, expecting it to remain flat in the next two years. However, sell-side analysts are forecasting it to accelerate by 63% going forward.

Additionally, the market is seeing EAGLE’s Uniform earnings to shrink by 17%, but analysts are projecting an impressive 19% earnings growth for the firm in the next two years.

That being said, ATRAM should take another look at Philippine Seven Corporation (SEVN:PHL). The market appears overly bullish about SEVN with expected Uniform earnings growth of 23%. However, analysts are seeing its Uniform earnings plummet by 11% a year going forward.

Most of ATRAM Alpha Opportunity Fund’s holdings look like an undervalued set of high-quality stocks with businesses displaying solid earning power and strong earnings growth potential. It just isn’t clear on an as-reported basis, incorrectly leading investors to think that this mutual fund is subpar with depressed earnings expectations.

Unsurprisingly, Uniform Accounting reveals the reality behind these companies’ underlying fundamentals—that ATRAM Alpha Opportunity Fund invests in high-quality companies.

Wilcon Depot, Inc. Tearsheet

Today, we’re highlighting one of the largest individual stock holdings in ATRAM Alpha Opportunity Fund—Wilcon Depot, Inc. (WLCON:PHL).

As our Uniform Accounting tearsheet for WLCON highlights, it trades at a Uniform P/E of 42.8x, well above global corporate averages and its historical averages.

High P/Es require high EPS growth to sustain them. In the case of WLCON, the company has recently shown a robust Uniform EPS growth of 37%.

Sell-side analysts provide stock and valuation recommendations that poorly track reality. However, sell-side analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

We take sell-side forecasts for PFRS earnings as a starting point for our Uniform earnings forecasts. When we do this, WLCON’s sell-side analyst-driven forecast shows that Uniform earnings will shrink by 17% in 2020 and grow by 38% in 2021.

Based on the current stock market valuations, we can back into the required earnings growth rate that would justify PHP 15.28 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of WLCON, the company would have to see Uniform earnings grow by 18% each year over the next three years. Sell-side analysts’ expected 38% earnings growth for the company is well above what the current stock market valuation requires.

WLCON has an earning power twice the long-run corporate averages—based on its Uniform ROA calculation. Moreover, with cash flows and cash on hand consistently exceeding obligations within the next five years, the company has a low dividend risk.

To conclude, WLCON’s Uniform earnings growth is below peer averages. However, the company is trading well above peer average valuations.

About the Philippine Markets Daily

“Friday Uniform Portfolio Analytics”

Investors who don’t engage in the buying or selling of securities for a living oftentimes rely on professionals to manage their own investments within the scope of their investment policies.

With so many funds and managers out there, it can get confusing and difficult to decide which one best suits your needs as an investor.

Every Friday, we focus on one fund in the Philippines and take a deeper look into their current holdings. Using Uniform Accounting, we identify the high-quality stocks in their portfolio which may not be obvious using the as-reported numbers.

We also identify which holdings may be problematic for the fund’s returns that they would need to reconsider from a UAFRS perspective.

To wrap up the fund analysis, we highlight one of their largest holdings and focus on key metrics to watch out for, accessible in our tearsheets.

Hope you’ve found this week’s focus on ATRAM Alpha Opportunity Fund interesting and insightful.

Stay tuned for next week’s Friday Uniform Portfolio Analytics!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com