Uniform Accounting reveals a business transformation that as-reported metrics missed, with this company earning returns that are actually 4x higher

The U.S. has stringent antitrust laws in place to control competition and to keep companies from monopolizing an industry and controlling prices. This healthcare company knows that well—federal regulators have blocked some of its M&A deals to keep it from having too concentrated of a market share.

Being already too large to grow massively through acquisitions, thus shrinking its growth opportunities, this company has been able to add another line of business by rethinking how to monetize its assets differently.

However, while stagnant as-reported returns signal that this initiative has not done much to generate value, Uniform Accounting thinks differently, with ROAs that have actually expanded to new highs.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

With the popularity of coal fireplaces in the early 1900s, cleaning the soot off of wallpapers used to be an issue for homeowners. Luckily, the job was made easier by a company called Kutol, whose main product was a moldable clay made especially for wiping off soot.

At that time, Kutol was the largest wallpaper cleaner manufacturer in the world. However, with the transition from coal to gas and electric sources of heat, Kutol’s product became obsolete—or at least for its original target market.

Reading an article about how wallpaper cleaning putty was used for various art projects, Joseph McVicker, the founder’s son, and his sister-in-law, a nursery teacher, gave the product to her students to use and play with. Seeing that it was a hit among the children, McVicker then reformulated the product and marketed it as a children’s toy under the name Play-Doh.

What used to be a wallpaper cleaner, Play-Doh has gone on to become one of the most iconic children’s toys of all time, with it even getting inducted into the Toy Hall of Fame.

Transforming the purpose of a product is not such a rare thing in the world of business. Coca-Cola did it too, initially setting out to be a cure for morphine addiction before becoming a beloved beverage.

UnitedHealth Group (UNH) also did something similar when it launched its Optum business in 2011.

UnitedHealth’s focus used to only be on its insurance and health maintenance business, with written premiums being its primary source of revenues, like all insurance companies do. It’s the largest health insurer across almost every state in the U.S.—which was a problem back then.

Because of its market leadership, regulators were blocking the company from acquiring smaller firms and becoming too concentrated. If it hadn’t, it would reduce the insurance options for individuals and corporations.

This means that the insurance plans taken by UnitedHealth would increase, as well as the risk for the system as a whole. This also meant that the company’s growth in the insurance space had been limited.

However, as the largest health insurer in the U.S., it had specialized knowledge about American patients and a massive data library on health care. By combining this data from their patient claims, pharmacy benefit management (PBM) operations, and other information sources, UnitedHealth was able to launch Optum.

Optum operates under three segments:

- OptumHealth, which uses its own data to partner with health care facilities and organizations to improve patient care.

- OptumInsight, which unlocks UnitedHealth’s data to help health care companies innovate in areas of need, help other health plans use analytics to improve outcomes, and help employers track and reduce health care costs.

- OptumRX, which uses data to identify the best drugs to include on UnitedHealth’s chosen list of drug offerings based on the best outcomes and lowest net costs, and uses UnitedHealth’s scale to get lower prices on drugs.

With Optum, UnitedHealth was able to enter into a different addressable market, specifically into data analytics for governments, corporations, and other organizations, as well as generate new revenue streams and optimize its patient care and pharmacy benefits management business.

UnitedHealth’s transformation of data—previously only used to improve internal insurance operations—into an entirely new business restored previously-capped growth potential and made it more of a health care powerhouse than it already was.

While this should have created significant value for UnitedHealth, looking at as-reported metrics, it seems like it has barely contributed to the firm’s profitability. As-reported ROA has been flat for the better part of a decade.

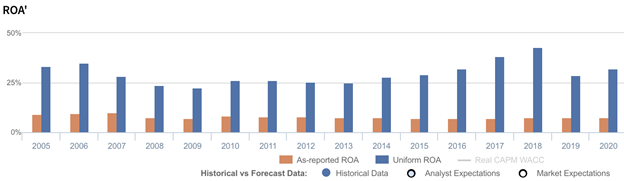

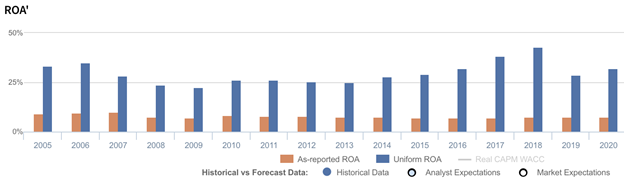

On the other hand, Uniform ROA reveals just how strong this business is and how quickly they’ve improved returns. Since the establishment of Optum in 2011, UnitedHealth’s Uniform ROA has expanded from 26% to 32% currently.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on UnitedHealth’s balance sheet. In recent years, goodwill sits at about $50 billion to $70 billion, making it the firm’s third largest long-term asset, arising from acquisitions made to further growth.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of UnitedHealth’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing poorly. In fact, it has been the opposite, with returns that are nearly 4x-6x greater.

UnitedHealth is actually more profitable than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

UnitedHealth’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 8% in 2020, but its Uniform ROA was actually 4x higher at 32%.

Specifically, UNH’s Uniform ROA has ranged from 22% to 43% in the past sixteen years while as-reported ROA ranged only from 7% to 10% in the same timeframe. Uniform ROA regressed from 34%-35% levels in 2005-2006 to 22% in 2009, before steadily rebounding to a peak of 43% in 2018. Uniform ROA has since faded to 32% through 2020.

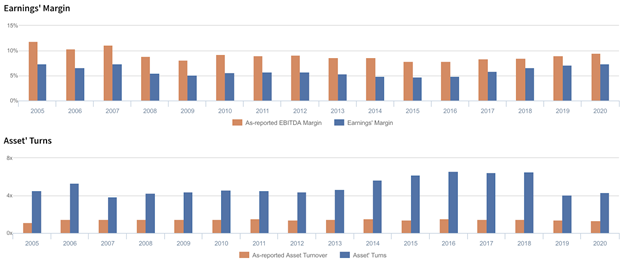

UnitedHealth’s Uniform earnings margin is weaker than you think, but its Uniform asset turns make up for it

Uniform ROAs have been driven primarily by trends in Uniform asset turns, accompanied by generally steady Uniform earnings margin.

Uniform turns rose from 4.5x in 2005 to 5.3x in 2006, before falling to 3.8x in 2007 and subsequently expanding to a peak of 6.6x in 2016. Since then, Uniform turns compressed to 4.4x in 2020.

Meanwhile, after sustaining 7% levels in 2005-2007, Uniform margins fell to 5%-6% levels from 2008-2017, before recovering back to 7% levels in 2018-2020.

At current valuations, markets are pricing in expectations for Uniform turns and Uniform margins to continue their recent decline.

SUMMARY and UnitedHealth Group Incorporated Tearsheet

As the Uniform Accounting tearsheet for UnitedHealth Group Incorporated (UNH:USA) highlights, the Uniform P/E trades at 19.6x, which is below the global corporate average of 25.2x but above its historical average of 17.6x.

Low P/Es require low EPS growth to sustain them. In the case of UnitedHealth, the company has recently shown a 13% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, UnitedHealth’s Wall Street analyst-driven forecast is a 4% and 14% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify UnitedHealth’s $367 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 1% per year over the next three years. What Wall Street analysts expect for UnitedHealth’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 5x the corporate average. Also, cash flows and cash on hand are 3.1x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, UnitedHealth’s Uniform earnings growth is around its peer averages, and the company is also trading in line with its average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com