Uniform Accounting shows this company’s switch to an entirely different sector generated much better returns at 13% Uniform ROA, not just 6%

When a business is not profitable, owners must find ways to save their business…or even just their assets.

Today’s company was once an oil producer, before transforming its core activities into an investment holding firm to achieve a more profitable business.

Through restructuring and a spin-off, this company has been able to generate robust Uniform ROA but as-reported shows weak returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Over the years, business owners have developed different strategies to manage risks and preserve the company’s resources. One of the go-to game plans they usually consider is diversifying one’s business into several entities that are all owned and controlled by a single holding company.

There are a lot of advantages in becoming a holding firm. Aside from the fact that it reduces risk, this type of business is not directly involved in manufacturing or operating activities, which means lesser day-to-day management.

Additionally, a holding firm can own up to 100% of its subsidiary, implying that it will ensure that a vote of owners will go its way.

An example of a businessman who took this action was Lucio Tan, the owner of LT Group, Inc. (LTG:PHL). After consolidating his interests into one portfolio, he was able to recognize a more efficient business.

Similarly, today’s company spun off its core assets to a wholly-owned subsidiary, raised capital by listing additional shares on the stock market, and made asset swaps with other existing companies, in order to execute its expansion plans.

Cosco Capital, Inc.(COSCO:PHL), formerly Alcorn Gold Resources Corporation, was initially engaged in oil and gas exploration when it was established in 1998 by Lucio Co, the owner and founder of Puregold Price Club, Inc. (PGOLD:PHL).

However, due to several years of unprofitability, Co decided to transform Alcorn into a holding company in 2013. From being purely an oil company, the company would now hold shares in various businesses including supermarkets, real-estate, wine distribution, and oil storage tanks.

Some of the businesses that the company invested in were Puregold Price Club Inc. (supermarket), Ellimac Prime Holdings (real-estate), Meritus Prime Distributions (wine distribution), and Pure Petroleum (oil storage tanks).

Through the consolidation of its businesses, Cosco Capital was able to enjoy healthy cash flows starting in 2013, which allowed the company to further make plans for its portfolio expansion. In 2014, it acquired 100% shares of Office Warehouse Inc., a retailer of office and school products with around 47 stores nationwide. Then, in 2015, the company bought RFC shopping center in Las Piñas City.

Recently, Cosco Capital entered into a swap agreement with Da Vinci Capital Holdings Inc (DAVIN), a company also owned by Lucio Co. The terms of the agreement include Cosco Capital spinning off three of its wine and liquor units to DAVIN, which also paves the way for the backdoor listing of these three unlisted units. In exchange, Cosco Capital will be able to acquire a controlling interest in DAVIN which would, in turn, strengthen the company’s position in the wine distribution business.

Taking into account all of the company’s diversification efforts, Cosco Capital was able to turn the tide and achieve robust profitability.

However, similar to other companies, Cosco Capital was affected by disruptions caused by the COVID-19 pandemic. Its real estate and wine and liquor businesses took a heavy hit as these were industries that were most negatively affected by quarantine restrictions.

Still, despite all the losses from other segments, Cosco Capital managed to increase its revenue by 12% from PHP 76.6 billion in H1 2019 to PHP 85.7 billion in H1 2020, thanks to its grocery businesses, Puregold and S&R. At 49% of Cosco Capital’s investments, Puregold’s ability to thrive during quarantine provided support for Cosco Capital’s profitability.

As for its low performing segments, they will likely contribute to the company eventually, once the government further eases the country’s quarantine restrictions.

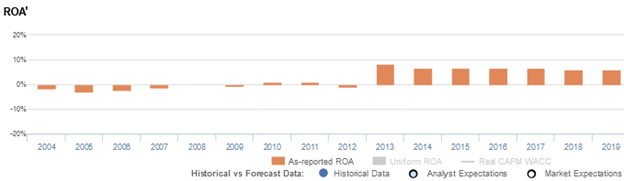

Overall, Cosco Capital’s 2013 decision to shift from oil and gas to become a retail conglomerate has generated profitability for the company. However, as-reported metrics show that returns have not been stellar, only ranging from 6%-8% since then.

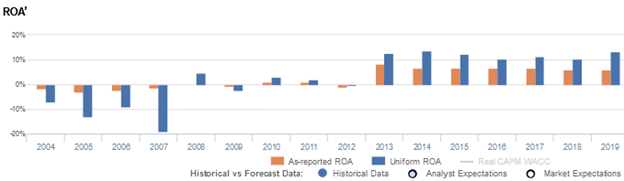

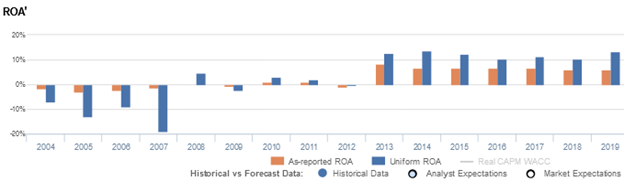

In reality, Cosco Capital’s focus on its diversification strategy actually enabled it to achieve stronger profitability, with Uniform ROAs ranging 10%-14% in the past seven years.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Cosco Capital’s balance sheet. The company’s goodwill has ranged from PHP 16 billion to PHP 18 billion, which is around 16% of its total assets in recent years, due to its extensive focus on acquisitions.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

If we remove this item from Cosco Capital’s asset base and with the many other necessary adjustments Valens makes, we arrive at a 13% Uniform ROA for 2019, significantly higher than its as-reported ROA of only 6%.

Cosco Capital’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Cosco Capital’s profitability has been weaker than real economic metrics have highlighted in eleven of the past sixteen years.

In reality, Cosco Capital’s true profitability has been higher than as-reported ROA in most years.

After ranging from -19% to 5% levels in 2004-2012, Uniform ROA improved to 13% in 2013, before reaching a peak of 14% in 2014. Thereafter, Uniform ROA gradually declined to 10% in 2018, before expanding back to 13% in 2019.

In contrast, after ranging from -3% to 1% in 2004-2012, as-reported ROA reached a peak of 8% in 2013, before gradually compressing to 6% in 2019.

Cosco Capital is a more efficient business than you think

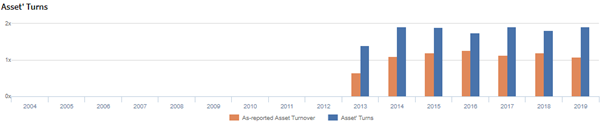

Similarly, as-reported metrics significantly distort the firm’s asset efficiency, a key driver of profitability.

From 2013-2019, Uniform turns ranged from 1.4x-1.9x, while as-reported asset turnover only ranged from 0.7x-1.3x, making the company appear to be a less efficient business than real economic metrics reveal.

Moreover, as-reported asset turnover has been lower than Uniform turns in each year for the past seven years, distorting the market’s perception of the firm’s historical asset efficiency level.

SUMMARY and Cosco Capital Tearsheet

As the Uniform Accounting tearsheet for Cosco Capital (COSCO:PHL) highlights, it trades at a Uniform P/E of 10.3x, below the global corporate average of 25.2x, but around its historical average of 11.1x.

Low P/Es require low EPS growth to sustain them. In the case of Cosco Capital, the company has recently shown a 26% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Cosco Capital’s sell-side analyst-driven forecast calls for a 1% and 4% Uniform EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cosco Capital’s PHP 5.48 stock price. These are often referred to as market embedded expectations.

Cosco Capital is currently being valued as if Uniform earnings were to shrink 15% annually over the next three years. What sell-side analysts expect for Cosco Capital’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is almost 2x the long-run corporate average, but cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Cosco Capital’s Uniform earnings growth is below peer averages, and the company is trading below peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com