With a 2% Uniform ROA, this airline may take more time before economic value takes off

When travel restrictions were imposed globally because of the pandemic, many investors became concerned about the state of the commercial aviation industry.

We discussed how Cebu Pacific, the pioneer of the Piso fare, was hit hard by the canceled flights and restrictions. Today, we will talk about another airline business in the country and how the company has been coping in this time of crisis.

Although Uniform Accounting suggests that the company’s profitability is higher than what as-reported metrics are portraying, its still muted profitability looks troubling for the firm.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The airlines industry has gained so much traction in the last decade, driven by a mixture of rising demand for leisure travel and more affordable airfares.

In 2009, total passengers carried in the Philippines amounted to nearly 11 million. This number more than doubled to 23 million passengers in 2010, and by 2019, at least 43 million passengers have been recorded as having flown either internationally or domestically in the Philippines.

The Piso fare promos have contributed to this increase in travelers, making it easier for the average Filipino to visit local provinces. While these promos have been largely associated with budget airlines, even full-service airlines nowadays are offering heavily discounted fares to remain competitive in the market.

One such airline is the Philippines’ flag carrier, Philippine Airlines.

PAL Holdings, Inc. (PAL:PHL) is a holding company primarily engaged in the air transport of passengers and cargo that is also riding the trend. The firm derives its revenues primarily from its subsidiary, Philippine Airlines.

This airline company has had its share of difficulties, particularly when low-cost carriers became serious competitors.

To remain competitive, it had to offer lower ticket prices on a regular basis through its Economy Supersaver option. Passengers still enjoyed baggage allowance and in-flight meals, but no longer received full points for their miles, among others.

Selling tickets at a lower price point from time to time allowed the firm to generate additional sales from flights that would have still flown even without those cheaper tickets.

PAL also needed to keep up with the digital age. The firm launched PAL Mobile in 2009 to make it easier to book flights on mobile devices through mobile browser. Then, in 2015, it fully rolled out its mobile app, making it even more convenient to book online.

However, even with all the caution PAL took to ensure business continuity, nothing could have prepared the firm for the COVID-19 pandemic.

With global travel restrictions in place, passenger airplanes could not take off as scheduled. As a result, investors pulled out quickly from airline stocks, sending the stock price of PAL’s fellow airline, Cebu Pacific, tumbling by more than 50% since March 2020.

Although PAL’s stock price has not fallen as much as its peer, the firm did report massive losses of PHP 10.7 billion and PHP 11.6 billion in Q1 2020 and Q2 2020, respectively.

Ahead of the local lockdown in March, PAL had already laid off 300 ground staff in February. However, since demand for airline travel remains low to this day, the company decided to lay off an additional 35% of its manpower this September.

At this point, it’s not just the rising costs and increasing losses that PAL has to address–the company needs to pay attention to its credit profile.

Many investors had initially feared bankruptcy in the airline market, given the high costs of maintaining its fleets and given the minimal revenues. These bankruptcy concerns prompted PAL Chairman Lucio Tan to pour in PHP 15.2 billion into Philippine Airlines in May 2020. As of June 30, total deposits are at PHP 17.68 billion, which were presented as non-controlling interests.

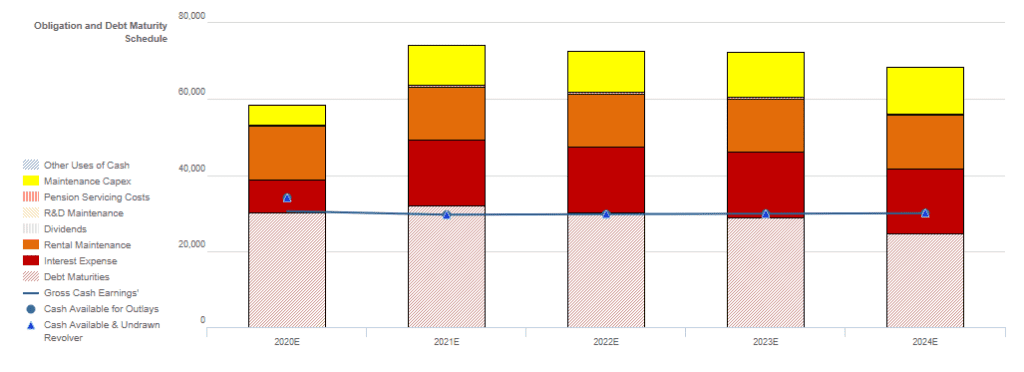

Looking at PAL’s financial obligations and debt maturity schedule, investors are right to be concerned. Each year, PAL’s available cash falls short of its obligations, owing to its PHP 30 billion debt headwall. It could postpone its maintenance capex, but even then, it would need to refinance its debt in order to satisfy obligations.

Additionally, investors and creditors are anxious about the company’s ability to recover quickly. Even with a slight relaxation in flight restrictions, it is likely that PAL will continue to struggle in its financial recovery, given its year-to-date losses.

Still, the market does not agree that these are good enough reasons to be concerned about PAL. Current valuations imply that the firm is still set to generate economic value in the future.

Although Uniform Accounting suggests that PAL’s profitability is higher than what the as-reported metrics are showing, the company’s true earning power is still at muted levels.

In 2019, PAL’s as-reported ROA was at 1%, whereas its Uniform ROA was actually at 2%. What the as-reported metrics missed is in the accounting of interest expense.

Interest expense represents the costs of taking on debt, but the Philippine Financial Reporting Standards (PFRS) allows the item to be classified as an operating cash flow. In reality, it is not part of the company’s operations and should always be classified as a financing cash flow.

As such, interest expense is added back to earnings to reflect the company’s true profitability. For PAL, the company recognized an interest expense of PHP 12 billion in 2019.

Applying the interest adjustment to earnings, along with the many other adjustments made, we arrive at a PHP 7.2 billion Uniform earnings and a 2% Uniform earning power for PAL in 2019.

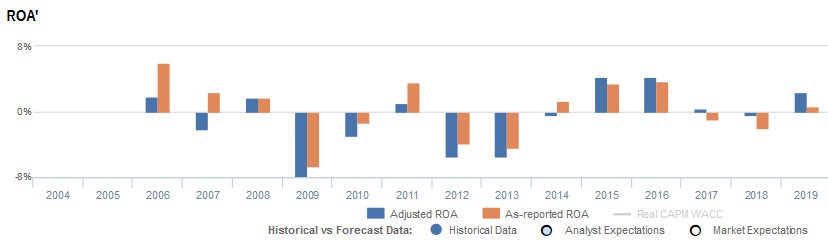

PAL’s recent earning power is somewhat stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight in the past three years.

PAL’s Uniform ROA has actually been higher than its as-reported ROA in recent years. Most recently, as-reported ROA was 1% in 2019, but Uniform ROA was actually higher at 2%.

After declining from 2% in 2006 to its lowest at -8% Uniform ROA in 2009, Uniform ROA recovered to 1% in 2011, before falling again to negative levels in 2012-2013. Uniform ROA then improved to 4% levels in 2015-2016, before fading to 2% in 2019.

Meanwhile, as-reported ROA only declined from 6% in 2006 to -7% in 2009, before ranging from -4% to 4% in 2010-2014. As-reported ROA then improved to 4% in 2015-2016, before declining to 1% in 2019.

PAL’s historical margins are weaker than you think

Trends in Uniform ROA have been driven by trends in Uniform earnings margins. Uniform margins have been lower than as-reported EBITDA margins in thirteen of the past fourteen years.

As-reported EBITDA margins declined from 19% in 2006 to -5% in 2009, before improving to 15% in 2011. Since then, as-reported EBITDA margins have mostly stayed positive, between 2% and 15%, except in 2013.

In contrast, Uniform margins dropped from 3% in 2006 to its lowest levels of -14% in 2009. Though it gradually recovered to 2% in 2011, Uniform margins fell back to -14% in 2013, and then reached its high of 9% in 2015. Since then, Uniform margins have deteriorated to -1% in 2018, but bounced back to 5% in 2019.

Looking at the firm’s margins alone, the as-reported metrics are making the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and PAL Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for PAL highlights, the Uniform P/E trades at 67.6x, which is well above corporate average valuation and its own history.

High P/Es requires high EPS growth. In the case of PAL, the company has recently shown a 21% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, PAL’s sell-side analyst-driven forecast calls for an immaterial Uniform EPS decline in 2020 and immaterial growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify PAL’s PHP 5.83 stock price. These are often referred to as market embedded expectations.

The company needs its EPS to grow by 27% each year over the next three years to justify current valuations. What sell-side analysts expect for PAL’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is below the long-run corporate average, and cash flows and cash on hand are below its total obligations—including debt maturities and capex maintenance. Together, this signals average credit risk.

To conclude, PAL’s Uniform earnings growth is above peer averages in 2020, and the company is trading above its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com