Working from home further enhanced this company’s leadership in VDI systems, launching Uniform ROAs of 20%+

With the continued transition from an office setup to a work-from-home setting, products that provide easy accessibility to work desktops continues to be a good investment for any company.

This technology company provides a great solution to support the employees’ need for flexibility and safety with the use of virtual desktops (VD). Its products continue to dominate the VD market, further fueling the company’s growth that is supplemented by world-class partnerships and a significant business transformation.

While the impact of its strategic growth is not visible when looking at as-reported returns, Uniform Accounting shows that it has led to stronger profitability, with Uniform ROAs that are nearly 5x the as-reported numbers.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

This time last year, this was the picture of a regular workday: dress up, commute to your office, and work at your desk for the rest of your shift. Much has changed over the past year, with the pandemic significantly disrupting how companies operated.

Strict quarantine guidelines prohibited businesses from having their full workforce working onsite. While some did have essential employees at the office, most firms set up remote working protocols to allow for business continuity.

In the Philippines, surveys showed that about 70% of companies have allowed for remote operations, while the remaining 30% continued office operations through minimal staff workforce and staggered shifts to facilitate physical distancing.

With almost a year since the widespread adoption of the work-from-home setup, more and more firms are considering keeping it that way even post-COVID.

It could be a smart move. Without the physical location barrier, companies could have a larger pool of potential talents, hiring from cities that would otherwise have been too far to hire from. Employees can also enjoy workspace flexibility and save time by not having to commute, which could lead to increased productivity.

Applications like Zoom (ZM), Atlassian (TEAM) software tools, Microsoft Outlook, and Google Suite became instrumental in the work-from-home transition. Apart from these teleconferencing or online collaboration tools, Citrix Systems (CTXS) also offers an invaluable product for the switch: virtual desktop infrastructure (VDI).

The purpose of VDI systems is to provide clients remote access to their desktop operating systems through a centralized server. This means that they are able to work anywhere and anytime from their personal computers, laptops, or mobile devices.

Desktop virtualization also boosts cybersecurity, and enhances data storage and recovery capabilities, mostly because the company would only have to back up, secure, and manage one centralized server.

XenDesktop, Citrix’s main entry in the VDI market, provides an avenue for clients to access their virtual screens in real time without interrupting other users and is considered by many to have one of the most complete and flexible systems among its competitors.

In comparison to VMWare, one of its largest competitors, Citrix has more diversity in its hosting solutions platform and provisioning technology. Additionally, the company has excellent strategic partnerships, allowing for integration with some of the major cloud companies including Microsoft, Google, Amazon, and Oracle.

Citrix has grown, and continues to expand with new product offerings and partnerships. To complement its growth over the past decade, the company has transformed its business by moving into the cloud, shifting to a software-as-a-service (SaaS) model, and moving from point to platform.

The transformation makes perfect sense for a software company like Citrix. The cloud has increasingly become essential to many business operations, and if there’s anything to learn from Adobe’s playbook, it’s that shifting to a SaaS model would cause massive growth through consistent revenue streams.

Platforms, as opposed to a single product, would also create more revenue streams. It also creates an ecosystem of interdependent products—similar to how Apple has the iPhone or the Mac, and the app store, Citrix has other bundled offerings such as analytics, hardware services, and management software on top of its core VDI product.

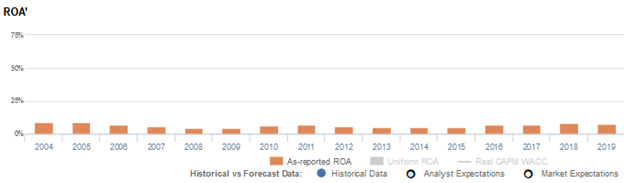

Given the company’s material business evolution, considerable profitability and high returns would be reasonable expectations. However, looking at as-reported return on assets (ROA), returns have been lackluster for the past sixteen years, ranging only from 4%-9%.

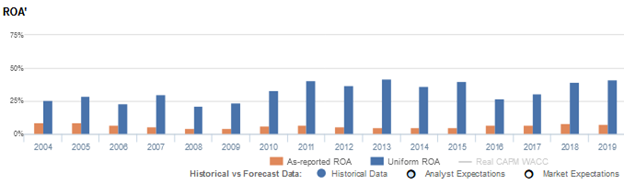

Uniform Accounting, on the other hand, reveals that the company is in fact a high-return business as expected, with Uniform ROAs ranging from 20%-40%. Furthermore, forecasts are for returns to climb to 60% levels, highlighting how Citrix’s VDI system, as well as its other suite offerings, will prove valuable in the post-COVID, remote working world.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Citrix’s balance sheet. Due to the acquisitions made over the course of its operations, the company’s goodwill sits at about $1.7 billion to $2 billion, or at least 20% of its total assets in recent years.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Citrix’s earning power. Adjusting for goodwill, we can see that the company isn’t actually displaying lackluster performance. In fact, it is the opposite, with returns that are more than 5x greater.

Citrix’s earning power is actually far more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Citrix’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 8% in 2019, but its Uniform ROA was actually significantly higher at 41%. When Uniform ROA peaked at 42% in 2013, as-reported ROA was only at 5%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been much higher. Citrix’s Uniform ROA for the past sixteen years has ranged from 22% to 42%, while as-reported ROA ranged only from 4% to 9% in the same timeframe.

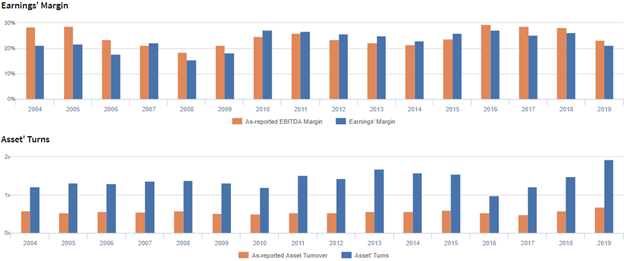

Citrix’s earnings margins are accurately stated while asset turns are understated

Citrix’s profitability has been driven by stability in Uniform earnings margin and trends in Uniform asset turns.

From 2008 to 2010, Uniform earnings margin increased from 16% to a peak of 27% levels, before subsequently declining to 23% in 2014. It then recovered to 25%-27% levels in 2015-2018, before compressing to 21% in 2019.

Meanwhile, Uniform asset turns remained at 1.2x-1.7x levels from 2004 to 2013. It then fell to a historical low of 1.0x in 2016 before reaching a peak of 1.9x in 2019.

At current valuations, markets are pricing in expectations for both Uniform earnings margin and Uniform asset turns to remain stable.

SUMMARY and Citrix Systems’ Tearsheet

As the Uniform Accounting tearsheet for the Citrix Systems, Inc. (CTXS) highlights, Its Uniform P/E trades at 19.2x, which is below corporate average valuation levels, but around its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Citrix, the company has recently shown a 9% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Citrix’s Wall Street analyst-driven forecast is a 51% EPS growth in 2020 and an immaterial change in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Citrix’s $129 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 2% each year over the next three years to justify current prices. What Wall Street analysts expect for Citrix’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 7x the corporate average. Also, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Citrix’s Uniform earnings growth is above its peer averages in 2020, but the company is trading below average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com