Despite this company’s valuable commodity and market leadership, it has only been able to fuel a TRUE earnings margin of 1%

Despite recent global economic and health problems, oil continues to live up to its reputation as “black gold”. It still is and will continue to be a highly valued resource to many countries and industries.

This Philippine oil refining company can trace its origins back to one of the most profitable companies in modern history. However, Uniform Accounting shows how little this company retained its predecessor’s key to success.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

150 years ago, American industrialist John D. Rockefeller incorporated Standard Oil. By essentially monopolizing the U.S. oil industry, the company grew to become one of the largest companies to have ever existed.

In fact, Standard Oil was so big it made John D. Rockefeller the world’s first official billionaire and the richest man in modern history when adjusting for inflation. The U.S. Supreme Court had to separate the company into 34 different businesses just to finally break the monopoly.

Today, many of Standard Oil’s successors are still in operation. These successors established many more oil companies found all over the world. Some have merged together or acquired others, while some have temporarily ceased operations due to the COVID-19 pandemic.

One of the companies that can trace its roots back to Standard Oil is Petron Corporation (PCOR:PHL).

During the 1930s, two of Standard Oil’s successors collaborated in expanding to the Far East. Standard Oil of New Jersey and Standard Oil of New York—soon to be known as Exxon and MobilOil respectively—formed a joint venture company known as Standard Vacuum Oil Company or Stanvac.

After a few decades, the two partners decided to dissolve the joint venture. Esso Philippines, Inc. would acquire Stanvac’s Philippine operations.

In the 1970s, Esso Philippines’ assets came under the government’s control and was rebranded as the Petrophil Corporation. It would later be renamed again as the Petron Corporation that we know of today.

Unfortunately, Petron retained little of what made Standard Oil great. Although Petron continues to lead the Philippines’ oil market, the company has struggled to consistently generate economic value.

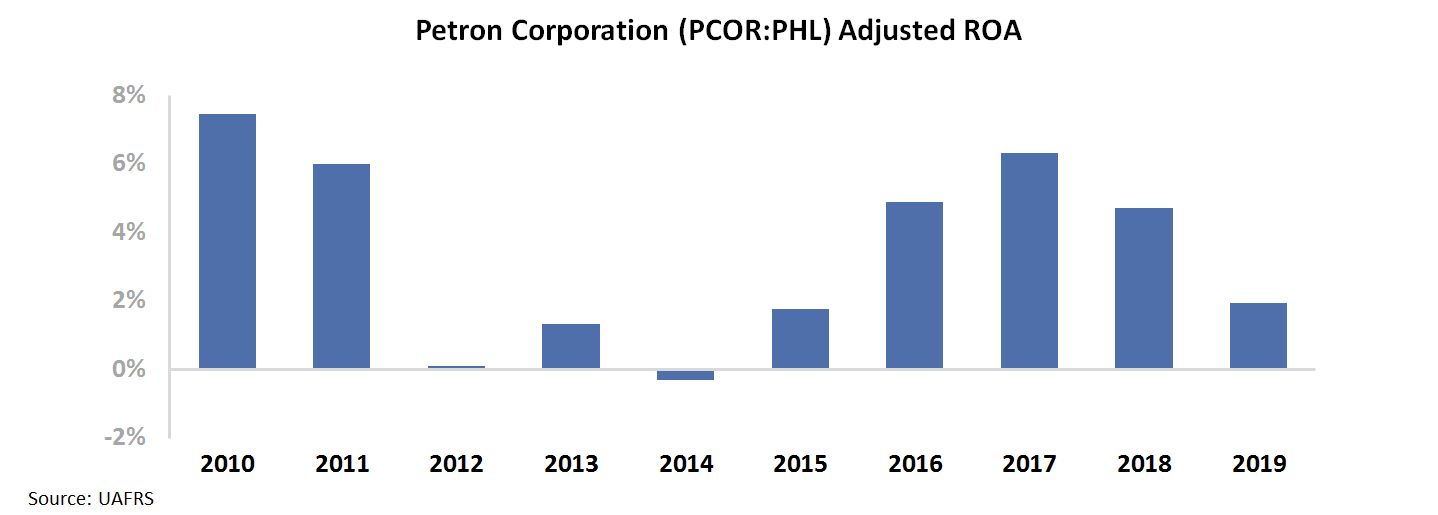

In the past decade, the firm has only been able to generate Uniform ROAs above corporate averages in half of those years. Additionally, Uniform ROA has been dropping since 2017.

The weakness in Petron’s earning power can likely be found in its failure to expand margins. Given the lack of brand loyalty and their price-conscious consumer base, the company has had very little pricing power and has been losing market share recently to smaller but cheaper competitors.

Instead of fighting on pricing, Petron has focused more on outscaling the competition. The company has been undergoing numerous capacity expansion projects, either by constructing more gas stations or building new oil refinery facilities.

More importantly, the firm has been unable to efficiently manage crude oil costs. Falling oil prices have made Petron’s commodity hedges worthless and has made the company take in more expenses than needed.

Petron also does not extract its own oil and relies heavily on Middle Eastern producers for its supply, making the firm highly vulnerable to macroeconomic and political headwinds.

All of these factors have led to Petron’s weak margins. Since 2004, the firm’s true earnings margins have never risen above 4%. However, you would likely reach a different conclusion if you were to look at the as-reported metrics instead.

Accounting distortions are falsely showing Petron to be a more cost-efficient business. One of the most severe distortions is about the treatment of income tax.

Since interest on debt is a tax-deductible expense, Philippine companies can reduce taxes paid by taking on more interest expense. Ás mentioned in many articles before, Uniform Accounting adds interest expense back to earnings because it is not a part of the company’s core operations. Since its impact on earnings is reversed, interest expense’s effect on tax must also be reversed.

So in reality, highly leveraged companies should be reporting greater tax expenses as a result of a higher taxable income. In the case of Petron, the company should be recognizing PHP 4.6 billion more in income taxes.

With the many other adjustments Valens makes, Petron’s earnings margin is actually 1% in 2019 and not 5% as reported.

Petron’s earning power is more volatile than you think

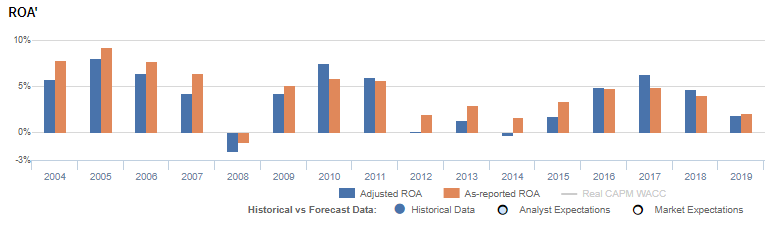

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much consistent business than real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been more volatile than as-reported ROA in the past sixteen years. Additionally, as-reported ROA only reached negative levels once in 2008, whereas Uniform ROA reached negative levels twice in 2008 and 2014.

After falling from a peak of 8% in 2005 to negative levels in 2008 amidst the Global Financial Crisis, Uniform ROA recovered back to 8% in 2010. Thereafter, Uniform ROA declined again to negative levels in 2014 as oil prices crashed, before rebounding 6% in 2017 and subsequently deteriorating to 2% in 2019.

Petron earnings margin is weaker than you think

Volatility in Uniform ROA has been driven by volatile Uniform earnings margin. From 2004 to 2008, Uniform margins declined from 3% to -1% in 2008.

Then, Uniform margins improved to 4% in 2010, before slowly touching negative levels in 2014. Thereafter, Uniform margins achieved new highs of 4% in 2017, but declined again to 1% in 2019.

At current valuations, markets are pricing in expectations for continued declines in Uniform Turns and Uniform Margins.

SUMMARY and Petron Corporation Tearsheet

As the Uniform Accounting tearsheet for Petron highlights, the Uniform P/E trades at 81.4x, which is far above corporate average valuation levels but below its own history.

High P/Es require high EPS growth to sustain them. However in the case of Petron, the company has recently shown a negative inflection in Uniform EPS.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Petron’s sell-side analyst-driven forecast calls for 68% Uniform EPS deterioration in 2020 followed by 72% Uniform EPS improvement in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Petron’s PHP 3.00 stock price. These are often referred to as market embedded expectations.

To justify current valuation, the company would need to grow its Uniform earnings by 19% each year over the next three years. What sell-side analysts expect for Petron’s earnings growth is far below what the current stock market valuation requires.

The company’s earning power is below the long-run corporate average. In addition, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high credit and dividend risk.

To conclude, Petron’s Uniform earnings deterioration is the worst among peers in 2020, but the company is trading the highest among peer valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com