Food has been the center of this company’s success, generating a Uniform ROA of 17%, not 10%

This food company has continually shown its commitment to profitably grow in the industry through its strategic initiatives. However, as-reported metrics say otherwise.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

When you hear the name San Miguel, the first thought that immediately comes into mind will always be beer.

However, despite San Miguel Food and Beverage Inc. (FB:PHL) or SMFB, being dominant in the local alcoholic beverages market, much of the success of the company is thanks to its food subsidiary, San Miguel Foods (SMF). Specifically, the various strategic brand acquisitions it has garnered throughout the years—such as Pure Foods, Spam, Magnolia, and Monterey—have helped the company maintain its market dominance.

Even during the pandemic, SMF was able to bounce back through its robust product strategies. With a solid focus on innovation and operational efficiencies, this delivered consolidated revenues of PHP 151 billion in 2021, up 12% from the previous year and 8% from 2019.

Among all of the company’s food businesses, the Protein and Animal Nutrition Business pulled in the biggest recovery after being severely impacted by the pandemic and the recent African Swine Fever (ASF), surpassing SMF’s performance in 2019.

The protein segment continued to capitalize on this recovery by growing its portfolio through the launch of Magnolia Chicken Timplados. It also revitalized its current lineup by producing more variants to this already-established segment, which included Spicy Wings, Oriental Wings, Inasal, and Spicy Fried Chicken.

Another strategy that SMF focused on is the expansion of its ready-to-eat business in order to give its customers healthier and more convenient alternatives.

For one, it introduced products like Chicken Caldereta, Chicken Curry, and Beef Mechado. SMF also made Korean-inspired dishes under its plant-based Veega line, which included Bulgogi and Spicy Soy Garlic Balls.

For the dairy and spreads business, particularly the ice cream category, SMF focused on premiumizing its products and deployed the Magnolia Gold label, with plans to include carabao’s milk in all ice cream flavors.

The coffee business also did the same with the introduction of Moccona Freeze Dried Instant Coffee, Moccona Cafè Style Coffee Mix, and L’OR Capsules—all of which are premium coffee brands of joint venture partner Jacob-Douwe Egberts (JDE).

However, the development of the company’s food products alone is not enough to ensure the company’s profitability amid market downtrends.

That is why as part of its recovery efforts, Great Food Solutions (GFS), SMF’s food service arm, jumpstarted its customer engagement initiatives through virtual product ideation sessions and product launches. This enabled GFS to bring Veega into its key accounts such as S&R, 7-11, and Conti’s.

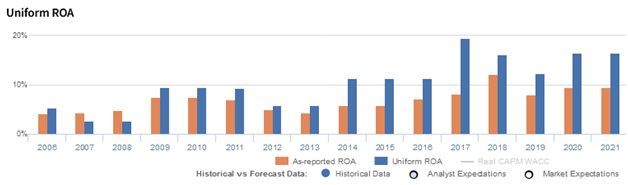

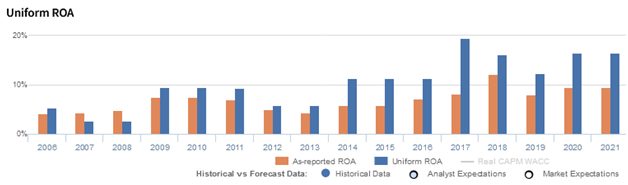

Overall, the continued strength of its food brands along with its resilient strategic initiatives helped boost the company’s performance. However, as-reported metrics show a company that has barely stood out, with ROAs only reaching 10%.

In reality, SMFB’s remarkable recovery efforts, as well as its current initiatives have been advantageous to the business, with its Uniform ROA achieving 17% despite the negative effects of the pandemic.

For this company, the largest accounting distortion has been the treatment of minority interest expenses. With the firm also having its own set of subsidiaries, each subsidiary has investors that possess non-controlling stakes.

According to the Philippine Financial Reporting Standards (PFRS), the profits attributable to minority shareholders can be recognized under operating cash flow, leading people to think that it is essential to the firm’s core operations.

In reality, it should always be classified as a financing cash flow. Minority shareholders have provided capital to the subsidiaries in exchange for a piece of the company’s earnings. As a result, minority interest expense should not be subtracted from SMFB’s revenues when calculating its real core earnings.

In 2021, SMFB recognized PHP 11.6 billion in minority interest expense, resulting in a PHP 19.8 billion net profit and a 10% as-reported ROA. By adding the expense back alongside the other adjustments Valens makes, the company should actually be recognizing PHP 31.9 billion in earnings and a 17% Uniform earning power.

San Miguel Food and Beverage’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that San Miguel Food and Beverage’s profitability has been stronger than real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROAs have been understated over the last fourteen years. For example, as-reported ROA was 10% in 2021, but its Uniform ROA was actually higher at 17%.

San Miguel Food and Beverage is more efficient with its assets than you think

As-reported metrics significantly overstate San Miguel Food and Beverage’s profitability trends.

For example, as-reported asset turns for the company was 0.8x in 2021, lower than Uniform asset turns of 1.2x, making the firm appear to be a less efficient business than real economic metrics highlight.

SUMMARY and San Miguel Food and Beverage, Inc.Tearsheet

As our Uniform Accounting tearsheet for San Miguel Food and Beverage, Inc. (FB:PHL) highlights, the company trades at a Uniform P/E of 13.1x, below global corporate average of 20.6x, and its historical P/E of 16.1x.

Low P/Es require low EPS growth to sustain them. In the case of SFMB, the company has recently shown a 88% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, SFMB’s sell-side analyst-driven forecast is to see Uniform earnings grow by 7% and 25% by 2022 and 2023, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify SFMB’s PHP 60.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 8% annually over the next three years. What sell-side analysts expect for SFMB’s earnings growth is well above what the current stock market valuation requires in 2022 and 2023.

Furthermore, the company’s earning power is 3x the long-run corporate average. Furthermore, cash flows and cash on hand are also 2x total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 170bps above the risk-free rate. Together, this signals a low dividend risk.

Lastly, SFMB’s Uniform earnings growth is above peer averages, but currently trades below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com