Globally advanced construction technologies are this company’s foundation to building TRUE returns that are three times higher than as-reported ROAs

This construction company has developed a reputation for focusing on large-scale projects, from a 67-storey condominium to a 6.2-hectare resort & casino. However, it has recently struggled to replace completed contracts of a similar size.

The company is mitigating this downside by tapping into another line of business, which as-reported metrics is showing to be ineffective. In reality, this business is enabling the company to continue performing well, seen only through the lens of Uniform Accounting.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In our DoubleDragon article, we talked about how competitive the Philippine real estate market has been. In order to thrive, DoubleDragon had to do something completely different from the veterans in the space.

DoubleDragon built commercial real estate outside of Metro Manila, where others were unwilling to venture into. As a result, it was able to grow and perform better than its peers during the COVID-19 pandemic.

Megawide Construction Corporation (MWIDE:PHL) seems to be facing the same dilemma. Its main business deals with the construction of residential and commercial real estate, namely condominiums and office towers.

Starting in 2007 when Megawide acquired its AAA (now AAAA) contractor license, the company had no problem finding construction projects. At the time, no one else could complete projects faster and more efficiently. Megawide adopted European construction systems and techniques, so the company had the most advanced formwork system in the country.

With the construction of its own pre-cast concrete plant, the company sought to bolster their competitive advantage further. Megawide was one of the few construction companies in the country at the time that also had a manufacturing component.

Megawide’s competitive strengths attracted the biggest clients, one of its earliest was SM. It enabled the company to focus on large-scale projects such as The Antel Spa Residences, the SMDC Showroom, and the Rockwell Business Center.

Megawide even began delving into government projects with the expansion of the Public-Private Partnership (PPP) program. It helped build schools and modernize the Philippine Orthopedic Center.

Although Megawide had been able to outperform its peers from 2016-2017, the company has recently struggled to fill its backlog. Construction order backlog only grew 5% from 2018 to 2019.

Competitors have begun advancing their formwork systems as well, threatening Megawide’s competitive edge. Coupled with the finite opportunities available for large-scale projects, the company has had difficulty replacing its finished contracts.

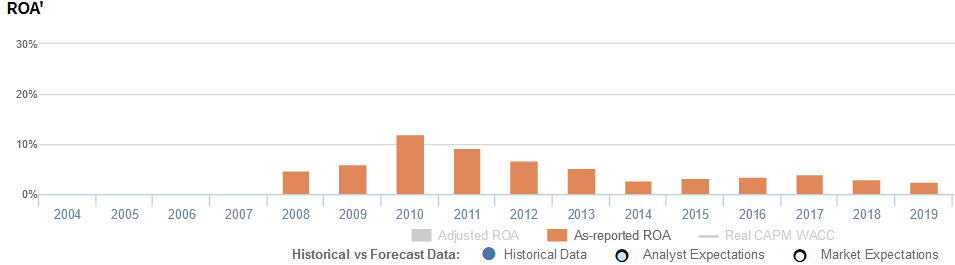

As a result, as-reported ROA fell from an already low 4% in 2017 to just 2% in 2019, following the completion of its ongoing contracts. Some may look at this performance and conclude that Megawide has done nothing but let its profitability collapse.

In reality, we see that, although profitability did decline, it remains at levels almost three times as-reported ROAs. From 2017 to 2019, Megawide’s Uniform earning power only fell from 10% to 6%, implying that the company is indeed making efforts to mitigate earnings erosion.

Over the recent years, Megawide has been developing its new airport and landport businesses to reduce its dependence on the cyclical nature of construction projects. Sales growth of these segments combined have been north of 25% for the past four years.

Instead of refining a new competitive advantage in the general construction market, the company has been pivoting specifically towards transportation infrastructure. Aside from the construction of the asset, the company now intends to be involved in the operation of the asset as well.

Currently, Megawide holds the concession assets of the Mactan-Cebu International Airport (MCIA) and the Parañaque Integrated Terminal Exchange (PITX). Meanwhile, it continues to bid for the $2 billion modernization of Ninoy Aquino International Airport (NAIA).

If Megawide wins the NAIA contract, the company could easily sustain the airport and landport segments’ sales growth for the years to come. However, as-reported metrics are understating its current success and its potential to be the leading transport-oriented infrastructure company.

The understatement of Megawide’s profitability is compounded further by failing to adjust for the accounting distortions, mainly interest expense.

Interest expense represents the costs of taking on debt, but the Philippine Financial Reporting Standards (PFRS) allows the item to be classified as an operating cash flow. In reality, it is not part of the company’s operations and should always be classified as a financing cash flow.

As such, interest expense is added back to earnings to reflect the company’s true profitability. For Megawide, the company recognized PHP 2.1 billion of interest expense in 2019 alone.

Reversing the distortion along with the other changes Valens makes, Megawide’s 2% as-reported ROA and PHP 859.5 million net income are adjusted to reveal a TRUE Uniform earning power of 6% and Uniform earnings of PHP 2.7 billion.

Megawide’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that the company is weaker than what real economic metrics highlight.

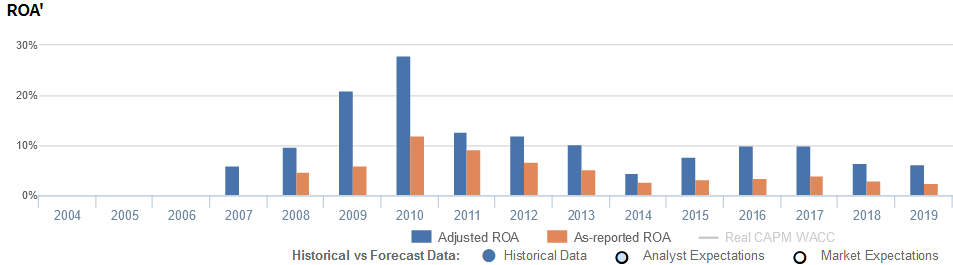

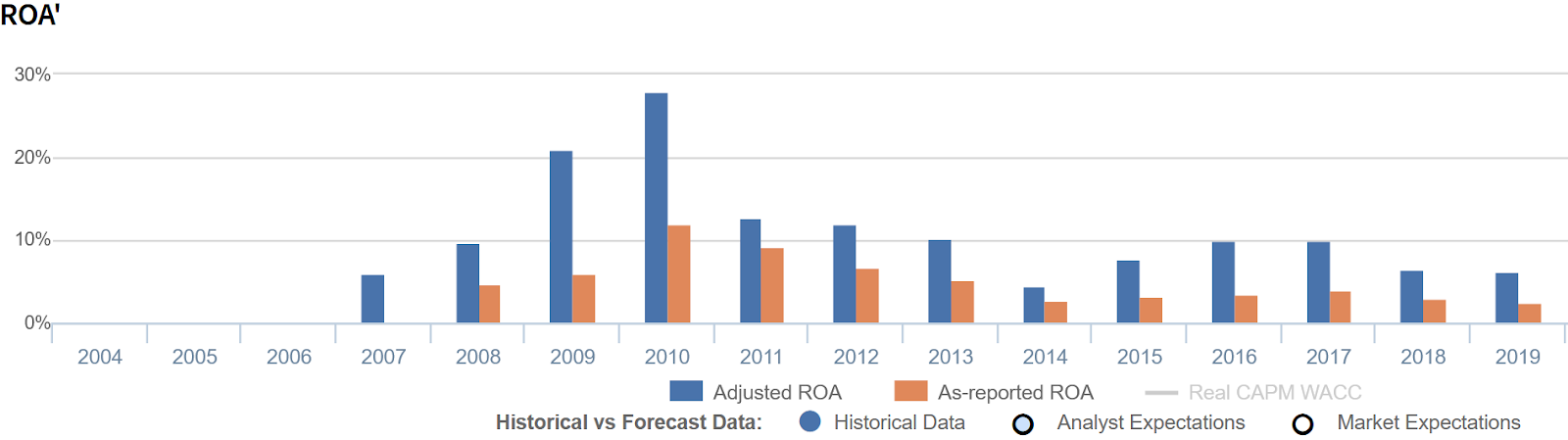

Megawide’s Uniform ROA has actually been higher than its as-reported ROA in the past twelve years. For example, as-reported ROA was 2% in 2020, but its Uniform ROA was actually 3x higher at 6%.

Specifically, as-reported ROA improved from 5% in 2008 to a high of 12% in 2010, before slowly fading to 2% in 2019.

Meanwhile, after expanding from 6% in 2007 to a peak of 28% in 2010, Uniform ROA fell to 5% in 2014. Thereafter, Uniform ROA recovered to 10% levels in 2016-2017, before compressing to 6% in 2019.

Megawide’s asset turns are stronger than you think

Strength in Megawide’s Uniform ROA has been driven by strength in its Uniform asset turns. Uniform turns have been higher than as-reported asset turnover in each of the past thirteen years.

From 2007-2010, as-reported asset turnover improved from 0.9x to 1.4x, before slowly eroding to 0.2x in 2018-2019. Meanwhile, Uniform turns rose 1.6x in 2007 to 3.9x in 2010, before gradually compressing to 0.5x in 2019.

Looking at the firm’s turns alone, the as-reported metrics are making the firm appear to be a less asset efficient business than is accurate.

SUMMARY and Megawide Construction Corporation Tearsheet

As the Uniform Accounting tearsheet for Megawide (MWIDE:PHL) highlights, the Uniform P/E trades at 44.6x, which is above corporate average valuations, but near its own history.

High P/Es require high EPS growth to sustain them. In the case of Megawide, the company has recently shown a 62% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Megawide’s sell-side analyst-driven forecast calls for a 513% and 71% Uniform EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Megawide’s PHP 7.21 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow by 5% each year over the next three years to justify current valuations. What sell-side analysts expect for Megawide’s earnings growth is well below what the current stock market valuation requires in 2020 and 2021.

In addition, the company’s earning power is near the long-run corporate average and intrinsic credit risk is 1,625bps above the risk-free rate. Together, this signals high credit and dividend risk.

To conclude, Megawide’s Uniform earnings growth is well below peer averages in 2020, and the company is trading well above its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com