Uniform Accounting shows how this company’s strategy is leading to a resilient business, but at the expense of weaker margins

When trends develop in an industry, it is often for a beneficial reason. However, these can at times cause harm, especially when extraordinary cases occur.

This real estate company has been acting against the conventional thinking of other commercial developers. Its strategy is paying off amidst the COVID-19 pandemic, but at the expense of weaker profitability as shown by Uniform Accounting.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Over the past couple of years, the Philippine commercial real estate market has experienced a rebound. Just last year, PHP 117 billion was spent for commercial construction in the country.

A near majority of the investments were made within Metro Manila, which many may find unsurprising. The region is the most densely populated in the Philippines, offering many lucrative opportunities for commercial developers.

However, what had been a boon for the industry has now turned into a hurdle for real estate. Due to Metro Manila’s dense population, the region is more susceptible to disease transmission. As a result, it has been on the receiving end of stricter quarantine measures during the COVID-19 pandemic.

In the past, we’ve talked about how property developers Ayala Land and SM Prime have suffered massive headwinds from the pandemic. According to Google’s Community Mobility Report, visits to retail establishments in Metro Manila slumped by 68% between February and July 2020.

There is one commercial real estate company though that has managed to evade the troubles of its peers. Where others are reporting weaker performance, DoubleDragon Properties Corp. (DD:PHL) has been reporting stronger results so far in 2020.

Established in 2009, DoubleDragon is a relatively new player in the market. That said, it has not followed the footsteps of veteran players in the space.

Instead of competing in Metro Manila as the veteran developers have, the company’s CityMalls business has been capturing the markets of provincial areas in the Philippines.

Furthermore, the company has mostly been targeting providers of basic needs as its tenants, including pharmacies, supermarkets, clinics, banks, and others. As such, it has been able to maintain high tenant retention rates.

Aside from its mall segment, the company’s hotel business is also seeing strong performance. Its Hotel 101 branches have been able to maintain high occupancy rates as BPO companies continue to book accommodations for employees.

As a result of DoubleDragon’s strategies, the company was minimally affected by the pandemic, even posting revenue growth of 45% year-over-year in H1 2020.

However, its Uniform profitability before the pandemic has been weak, only ranging 0%-2% each year. Although this is partly due to the time needed for their projects to generate revenue, its margins have been weaker than perceived.

In fact, DoubleDragon’s as-reported EBITDA margins are significantly overstating the company’s true margins. The company’s Uniform earnings margins have only reached as high as 30% historically, not 46%.

The overstatement in DoubleDragon’s margins is mainly due to an accounting distortion. Philippine Financial Reporting Standards (PFRS) allows companies to remeasure investment properties based on fair value.

Any change occurring from the remeasurement is charged as a gain or a loss in the income statement, even without an actual inflow or outflow of cash. To better reflect the company’s economic performance, these remeasurements should be reversed.

In the case of Double Dragon, its investment properties represent nearly the entire asset base. A small change in its market value can have a material impact on the income statement.

In fact, in 2019, the company recognized PHP 9.2 billion unrealized after-tax gains from its investment properties. This single-handedly turned the company from running at a net loss into a profit-making business of PHP 8.8 billion.

Reversing the distortion along with the other changes Valens makes, DoubleDragon’s 46% as-reported EBITDA margin and PHP 8.8 billion net income are adjusted to reveal a TRUE Uniform earnings margin of 30% and Uniform earnings of only PHP 2.0 billion.

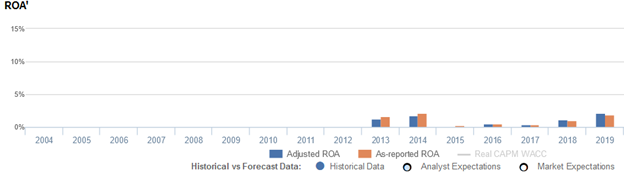

DoubleDragon’s recent asset growth is weaker than you think

As-reported metrics distort the market’s perception of the firm’s recent asset growth. If you were to just look at the as-reported ROA, you would think the company is a more aggressive business than real economic metrics highlight.

Historically, DoubleDragon’s Uniform asset growth has been lower than its as-reported ROA for three of the past six years. Most recently, as-reported asset growth was 38% in 2019, but its Uniform asset growth was actually lower at 23%.

As a newly formed company, DoubleDragon’s asset growth has been consistently positive, although weakening each year. From 2014-2019, Uniform asset growth has steadily fallen each year from 758% to 23%.

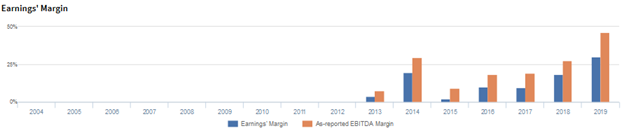

DoubleDragon’s earnings margin is weaker than you think

The weakness in Uniform ROA has been driven by trends in Uniform earnings margins. In fact, Uniform margins have been lower than as-reported EBITDA margin for each of the past seven years.

As-reported EBITDA margin jumped from 7% in 2013 to 30% in 2014, before falling to 9% in 2015. Since then, as-reported EBITDA margin has steadily expanded to a peak of 46% in 2019.

In contrast, Uniform margins rose from 4% in 2013 to 20% in 2014, before collapsing to a low of 2% in 2015. Since then, Uniform margins have improved to a high of just 30% in 2019.

Looking at the firm’s margins alone, the as-reported metrics are making the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and DoubleDragon Properties Corp. Tearsheet

As the Uniform Accounting tearsheet for DoubleDragon highlights, the Uniform P/E trades at 51.4x, which is well above corporate average valuation levels but below its own history.

High P/Es requires high EPS growth. In the case of DoubleDragon, the company has recently shown a 70% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, DoubleDragon’s sell-side analyst-driven forecast calls for a 3% Uniform EPS growth in 2020 followed by an immaterial decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify DoubleDragon’s PHP 14.50 stock price. These are often referred to as market embedded expectations.

The company needs its EPS to grow by 25% each year over the next three years to justify current valuations. What sell-side analysts expect for DoubleDragon’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is below the long-run corporate average, and cash flows and cash on hand are below its total obligations—including debt maturities, and capex maintenance. Together, this signals high credit and dividend risk.

To conclude, DoubleDragon’s Uniform earnings growth is above peer averages in 2020, and the company is trading well above its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com