Having the taste of home positioned this company as the leading fast-food chain in the country, achieving Uniform ROA double its as-reported ROA

This restaurant chain built its empire from the ground up and became the largest fast-food company in the country. Focusing on its expansion initiatives paved the way for this company to go global, beating another international industry titan in the process.

However, looking at as-reported metrics, it seems that its strategy hasn’t been generating accurate returns. In reality, Uniform Accounting shows that the company’s delicious and expanding portfolio has actually achieved Uniform ROAs that are higher than its as-reported.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Before becoming one of the richest billionaires in Asia, Tony Tan Caktiong started out from modest beginnings. Similar to Megaworld’s Andrew Tan, he also migrated from China to the Philippines in order to live a better life.

At an early age, he was already immersed in the field of commerce when his father started his own restaurant business. This venture then became profitable, which allowed Tony to graduate with a degree in chemical engineering at the University of Santo Tomas.

However, in 1975, after visiting the Magnolia Ice Cream plant in Quezon City, Tony decided to switch professions and opened two ice cream parlors in Cubao and Quiapo.

Upon realizing that customers weren’t keen on eating ice cream all the time, he added chicken and hamburger sandwiches to his menu. These additions were so popular that hamburgers were becoming more profitable than his original product. It was clear he had to change the business into a fast-food spot that would cater to the tastebuds of the Filipino people.

So in 1978, Jollibee Corporation (JFC:PHL) was born, forever changing the direction of the fast-food industry in the Philippines.

Since then, Jollibee has expanded nationwide. From its “juicylicious” Chickenjoy to its Langhap-Sarap Yumburger, Jollibee has continued to introduce new menu items—such as its famous palabok, Jolly Hotdog, Peach Mango Pie, and Jolly Spaghetti—throughout the years.

The Filipinos’ undying love for the “Filipino taste” proves that this restaurant chain has become a huge part of the country’s culture. Due to this, Jollibee was able to remain the top fast-food brand in the Philippines, the only country where McDonald’s isn’t number one. In 2020, Jollibee has around 1,100 stores nationwide while McDonald’s only has 640 branches.

Jollibee’s mission of continuously spreading joy allowed the company to further widen its industry footprint by going global. It was able to open up branches in countries in Southeast Asia, the Middle East, North America, and Europe, where thousands of Filipinos lined up on opening days just to have a taste of home.

However, in order to grow, the company could not just rely on one restaurant chain. It shifted its focus on expanding through domestic and international acquisitions—including Red Ribbon and Greenwich in the Philippines, Coffee Bean and Smashburger in the U.S., and Yonghe King in China—to name a few.

In February, it announced its 50-50 joint venture with its first Japanese restaurant, Yoshinoya International Philippines. Currently, there are three Yoshinoya restaurants in the country. If the deal pushes through, Jollibee plans on opening around 50 stores in the country, which will then help give the company more avenues to grow.

Though operations in the Philippines suffered during the pandemic, Jollibee’s international segment revenues slightly improved in 2020. In the U.S., the company started its nationwide delivery service by partnering with DoorDash. The company also managed to open 12 stores across North America. In 2021, Jollibee plans to add 28 more stores in North America, marking the largest addition to the country’s network in the company’s history.

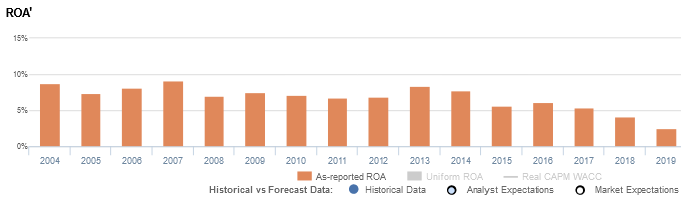

Jollibee’s ever-growing portfolio and its intense focus on its expansion initiatives would make investors think the company has been able to push its profitability higher. However, looking at as-reported metrics, it appears that this strategy hasn’t made Jollibee a consistently profitable business, with return on assets (ROAs) only reaching a high of 9% in 2007.

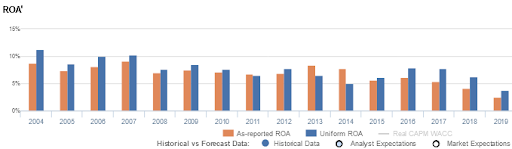

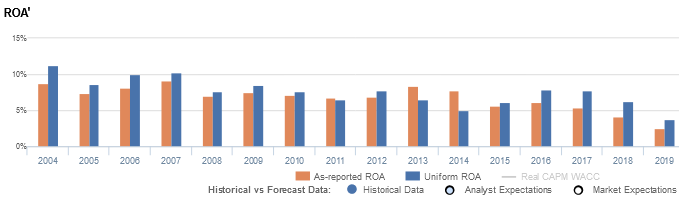

In reality, Uniform Accounting shows that Jollibee’s efforts to expand its global presence has generated better returns, with Uniform ROAs reaching 11%.

One of the distortions between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Jollibee’s balance sheet. The company’s goodwill has ranged from PHP 7 billion to PHP 14 billion, which is around 9% of its total assets in recent years, due to its extensive focus on acquisitions.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

If we remove this item from Jollibee’s asset base and with the many other necessary adjustments Valens makes, we arrive at a 4% Uniform ROA for 2019, double its as-reported ROA of only 2%.

Jollibee’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight, especially with recent years showing below cost-of-capital returns.

Jollibee’s Uniform ROA has actually been higher than its as-reported ROA in fourteen of the past sixteen years. For example, as-reported ROA was 2% in 2019, but its Uniform ROA was actually twice that at 4%. When Uniform ROA peaked at 11% in 2004, as-reported ROA was only at 9%.

Specifically, Jollibee’ Uniform ROA has ranged from 4% to 11% in the past sixteen years, while as-reported ROA has ranged only from 2% to 9% in the same timeframe. Uniform ROA declined from a peak of 11% in 2004 to 9% in 2005, before rebounding to 10% levels in 2006-2007 and subsequently fading to 5% in 2014. Thereafter, Uniform ROA improved to 8% levels in 2016-2017, before compressing to a low of 4% in 2019.

Jollibee’s earnings margin is weaker than you think

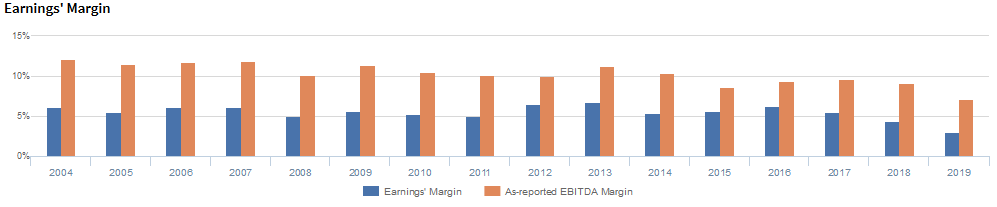

The recent strength in Uniform ROA has been driven by strength in Uniform asset turns, although this is offset by a historically weak Uniform earnings margin. Since 2004, Uniform margins have been significantly lower than as-reported EBITDA margins each year.

As-reported EBITDA margins were maintained at 12% levels from 2004-2007, before contracting to 9%-10% levels in 2010-2018 and falling further to 7% in 2019.

Meanwhile, Uniform margins were sustained at 5%-6% levels from 2004 to 2011, before improving to 7% levels in 2012-2013. Thereafter, Uniform margins compressed back to 5%-6% levels through 2017, before eroding to 3% in 2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost efficient business than is accurate.

SUMMARY and Jollibee Foods Corporation Tearsheet

As the Uniform Accounting tearsheet for Jollibee Foods Corporation (JFC:PHL) highlights, it trades at a Uniform P/E of 39.7x, above the global corporate average of 25.2x, but below its historical average of 56.3x.

High P/Es require high EPS growth to sustain them. In the case of Jollibee, the company has recently shown a 57% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Jollibee’s sell-side analyst-driven forecast calls for a 90% and 54% Uniform EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Jollibee’s PHP 187 stock price. These are often referred to as market embedded expectations.

Jollibee is currently being valued as if Uniform earnings were to grow 32% annually over the next three years. What sell-side analysts expect for Jollibee’s earnings growth is far above what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is below the long-run corporate average. However, cash flows are 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low dividend risk, although credit risk is moderate due to its 130bps iCDS.

To conclude, Jollibee’s Uniform earnings growth is the highest among peers in 2020, despite trading in line with its average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com