Microblogging and real-time engagement are trends this social media company has perfected, leading to Uniform ROAs of 10%+, not negative levels

This social media giant enables people to follow current events and spark conversations, effectively managing real-time engagement among its users.

Because of this, the company has been able to amass a few hundred million active users which it successfully monetizes through its ad platform.

However, as-reported return on assets (ROAs) indicate weak profitability, which has been consistently negative up until recently. Uniform Accounting, on the other hand, reveals that the company’s advertising model is in fact highly robust as expected, showing Uniform returns that have been positive since the company’s IPO.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

The rise of social media in the 2000s was revolutionary. Social media platforms made access to information available at the click of a button. They have also gone as far as providing consumers with the capability to communicate with friends and family within mere seconds.

We’ve previously talked about the largest social media platform, Facebook, and its humble beginnings. Today, we will talk about another leading social networking site, Twitter (TWTR:USA).

Twitter is a microblogging site that optimizes excellent real-time engagement among registered members through a short post of a maximum of 280 characters called “tweets.” These tweets may contain photos, videos, links, or text.

While Facebook is more focused on connecting people with one another, Twitter is centered more on topics and ideas. Twitter is more known as a place for users to just share their thoughts or browse through the content of users that you follow.

It is also commonly used as a place to read breaking news, since topics or headlines can be grouped with the use of hashtags. This function on Twitter allows users to discover the biggest stories each day. As a result, conversations are easily sparked and different movements spread like wildfire on Twitter.

With this kind of real-time engagement, Twitter attracts great user interaction. This provides a perfect opportunity for advertisers to capitalize on popular topics around the world and reach users whenever and wherever they are.

Since tweets can reach millions of users in seconds, Twitter generates its profits from advertisers promoting tweets, accounts, or trends that will appear on people’s timelines.

For example, the option of paying for in-stream video ads is available for advertisers to be distributed to a targeted audience.

In order to ensure that these promoted products end up into the right users’ timelines, Twitter uses an algorithm to tailor its advertising.

Users’ activities—meaning who they follow, what they tweet, and their searches, views, or interactions with other Twitter accounts—are the information the company uses to customize Twitter ads specifically for each user.

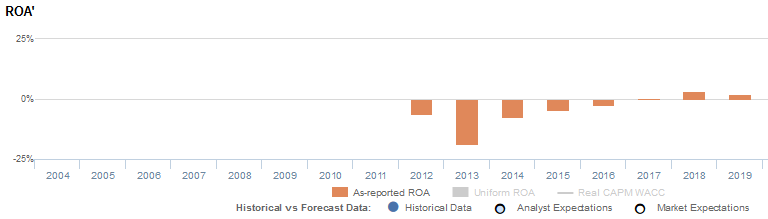

With over 192 million daily active users, this is how Twitter takes advantage of its strong network effects. However, looking at as-reported metrics, it appears that its advertising model has only been profitable recently, and even then, at only below cost-of-capital levels.

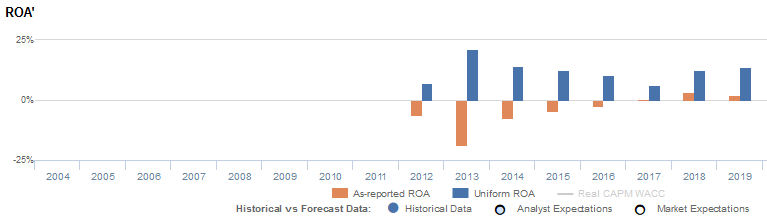

Uniform Accounting paints an entirely different picture, with Uniform ROAs that have been remarkably robust, currently sitting at 14%, 7x higher than the as-reported ROA of 2%.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of excess cash on Twitter’s balance sheet.

While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

The purpose of removing excess cash is to see what the true operating ROA of the firm is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

In the case of Twitter, the company had a substantial excess cash balance in the amount of $6 billion to $7 billion, most of which is tied up in short-term marketable securities. This materially overstates the company’s cash balances, inflating the asset base and causing profitability to look weaker than it really is.

As a result, as-reported ROAs are not capturing the strength of Twitter’s earning power. Adjusting for excess cash, we can see that the company isn’t actually performing poorly. In fact, it’s the complete opposite, with the company being profitable even during its early years after its IPO.

Twitter is actually more profitable than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Twitter’s Uniform ROA has actually been higher than its as-reported ROA in the past eight years. For example, as-reported ROA was 2% in 2019, but its Uniform ROA was actually over 7x higher at 14%.

Specifically, Twitter’s Uniform ROA has ranged from 6% to 21% in the past eight years while as-reported ROA ranged only from -19% to 3% in the same timeframe. Uniform ROA elevated from 7% in 2012 to 21% in 2013, before gradually decreasing to 6% in 2017 and rising to 14% in 2019.

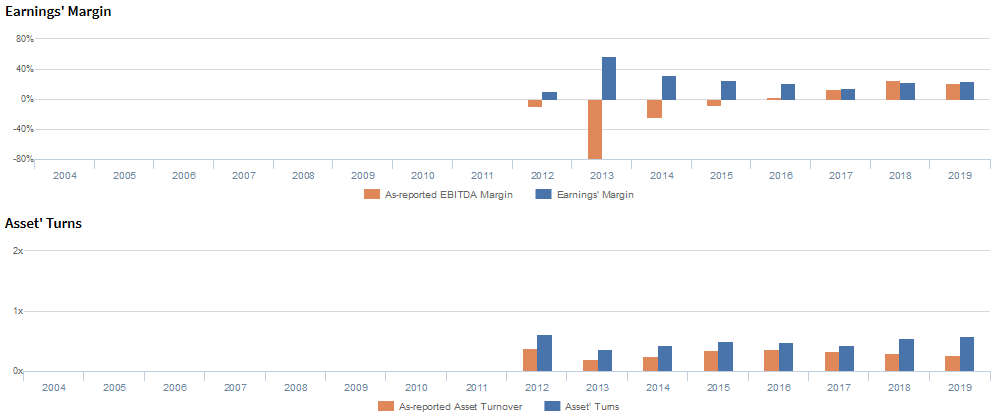

Twitter’s Uniform earnings margins and Uniform asset turns are more robust than you think

Uniform ROAs have been driven primarily by trends in Uniform earnings margins, accompanied by generally steady Uniform asset turns.

Uniform earnings margins jumped from 11% in 2012 to 58% in 2013, before fading to 15% in 2017 and subsequently recovering to 24% in 2019. Meanwhile, Uniform asset turns declined from 0.6x in 2012 to 0.4x in 2013-2014, before rebounding back to 0.6x in 2018-2019.

At current valuations, markets are pricing in expectations for Uniform margins to continue improving and for Uniform turns to remain stable.

SUMMARY and Twitter Tearsheet

As the Uniform Accounting tearsheet for Twitter, Inc. (TWTR:USA) highlights, the Uniform P/E trades at 50.6x, which is above the global corporate average of 25.2x and its historical Uniform P/E of 31.1x.

High P/Es require high EPS growth to sustain them. In the case of Twitter, the company has recently shown a 25% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Twitter’s Wall Street analyst-driven forecast is a 4% EPS shrinkage in 2020, followed by a 37% EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Twitter’s $72 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 24% per year over the next three years to justify current stock prices. What Wall Street analysts expect for Twitter’s earnings growth is below what the current stock market valuation requires in 2020 but above its requirement in 2021.

Furthermore, the company’s earning power is 2x the corporate average. Also, cash flows and cash on hand are 3.5x higher than its total obligations—including debt maturities and capex maintenance. Together, this signals low credit risk.

To conclude, Twitter’s Uniform earnings growth is around its peer averages, and the company is also trading in line with its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com