MONDAY MACRO: At 14.7x, this is a buying opportunity for the Philippine stock market. Inverted yield curves are not a local concern.

The novel coronavirus pandemic (COVID-19) has had such a severe impact in the global economy in just a few months. It has caused massive declines in stock markets worldwide, as well as uncertainty in the Treasury yield markets.

In the Philippines, negative investor sentiment was exacerbated by the Enhanced Community Quarantine (ECQ) in Luzon, now in its second week. The stock market is now down over 40% since the start of the year.

With talks of global recession becoming more likely because of COVID-19, this bond-market metric is triggering more fears, especially when viewed without a true understanding of companies’ credit profiles.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

There have been over 300,000 confirmed COVID-19 cases and at least 14,000 resulting deaths in around 170 countries and territories worldwide.

Governments are implementing flight bans and mandatory self-quarantine as precautionary measures to contain the spread of the virus. Numerous cities have closed their borders and ordered daily curfews to restrict people’s movement, and hopefully flatten the curve—the coronavirus curve.

Just last week, Europe replaced China as the new epicenter of COVID-19 cases, with Italy recording the highest number of deaths globally. In the US, the number of cases is now over 32,000, with nearly half of that coming from the state of New York.

With major economies suffering from reduced operations, the coronavirus pandemic has sparked recession fears for the global economy.

In the United States, recession fears manifested through the collapse of Treasury yields, resulting in a brief inversion of the yield curve.

Treasury yields refer to the total return on investment on the government debt obligations. An increase in yield means a decline in the value of the treasury note, bill, or bond, and vice versa.

An inverted yield curve happens when the yields of short-term debt instruments become higher than long-term debt instruments.

Normally, long-term Treasury bonds have higher yields to compensate investors to hold the bond for a longer period of time, at a premium. A declining long-dated yield trend may indicate expectations for slower economic growth, making long-term bonds less attractive to hold.

So when long-dated yields fall below short-dated yields, investors become concerned that a recession is nearing. In the US, an inverted yield curve has preceded all five recessions since 1980.

For example, the 2008 financial crisis had an inverted yield curve in late 2005, while the 2001 dot-com bubble was preceded by two inverted yield curves in 1998 and 2000.

A way to manage these interest rates is through monetary policies. Short-term bonds such as the 3-month bond yields soared after the US Federal Reserve’s historic December rate hike in 2018.

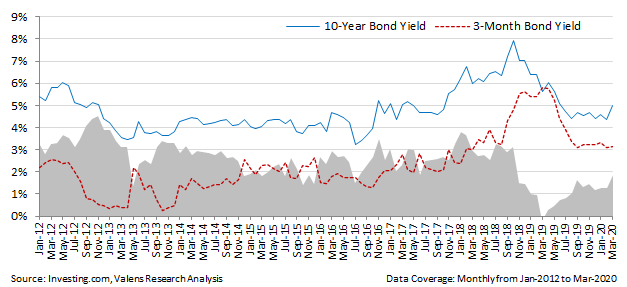

The Philippines is no exception to this phenomenon as an inverted yield curve briefly occurred in the country in March 2019. A series of rate cuts in 2019 reversed this inverted yield curve.

The Philippine 10-year Treasury Yield has remained stable at lower levels relative to bond yields during the global financial crisis. However, inflation concerns and the central bank’s planned rate cuts caused a decline in the 10-year bond yields.

In March 2019, 10-year bond yields fell to 5.6% from 7.0% in December while 3-month bond yields increased to 5.8% from 5.6% in December.

As of March 20, 2020, 10-year bond yields have fallen to 5.0% while 3-month bond yields have dropped further to only 3.1%, increasing the difference of the yields to 1.9% from -0.2% last March 2019.

Meanwhile, regional peer Singapore has experienced an inverted yield curve multiple times in the past two years. The first crossover of the 10-year vs. 3-month bond yields occurred in December 2018, where the short-term yield exceeded the long-term yield by 0.6%. Subsequently, the 3-month bond yield exceeded the 10-year bond yield four more times in the past eight months.

Investors have reason to worry, given the decline in consumer spending because of the ECQ in Luzon. Remittances from overseas Filipino workers (OFW) will also likely fall given that some of the hardest-hit countries in the world are top OFW locations.

However, this is no reason to panic.

Our Monday Macro Report on the Philippines’ credit profile shows that a sizable amount of cash is still available for outlays for the largest Philippine companies, which should cover their obligations and debt maturities even when their Uniform gross earnings cannot.

Together with no catalyst for credit destruction for companies in the Philippine Composite Index, proper fiscal sustainability from the government’s tax reforms, and a low-interest rate environment, the Philippines should be able to pacify recession fears and minimize the pandemic’s impact.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com