MONDAY MACRO: Contrary to what as-reported metrics show, the PH stock market hasn’t become significantly more expensive

Most of the companies listed in the Philippine Stock Exchange have already submitted their Q3 2021 results, so it would be interesting to see where market valuations are currently at.

With the PSEi already sustaining 7,200+ levels, as-reported numbers may lead many to believe that the market is significantly overvalued, but Uniform Accounting reveals that the market is actually close to being fairly valued.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

Many were expecting a weaker business performance in Q3 2021, as the Philippine government reinstated some quarantine restrictions in June due to rising COVID cases and fears over the Delta variant.

That said, a lot of the companies listed in the Philippine Stock Exchange (PSE) were still able to report better numbers. For instance, Jollibee (JFC:PHL) managed to generate a profit in Q3 2021 when the firm ran at a net loss during the same period last year.

In addition, Semirara Mining and Power (SCC:PHL) nearly doubled its revenues and more than quadrupled its profit last quarter compared to Q3 2020, as the global demand and price of coal has skyrocketed in recent months.

However, not everyone is reporting better numbers. The airline stocks Cebu Pacific (CEB:PHL) and PAL Holdings (PAL:PHL) continue to burn cash, as current passenger volumes are still far from pre-pandemic levels.

Overall, it seems the market has responded to the generally improving results. Since November 4, the Philippine Stock Exchange index (PSEi) has remained above 7,200 and it even breached the 7,400 level on November 9.

To provide more context, we should also look at other market valuation indicators. We’ve previously discussed the usefulness of the forward price-to-earnings (P/E) ratio and the forward enterprise value-to-earnings (Fwd V/E′) ratio.

To take into account the company’s future growth, the forward P/E and V/E ratios use the company’s projected earnings of the current year instead of the reported earnings of the previous year.

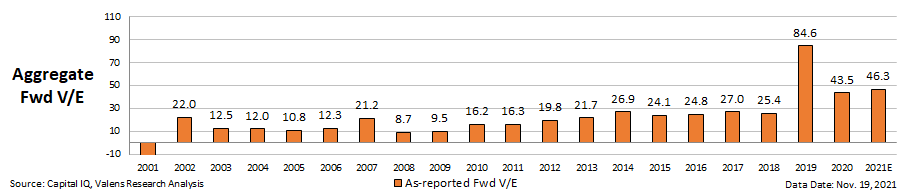

Looking at the as-reported forward V/E of PSE-listed companies in aggregate, current market values are at a 46.3x multiple, which is more than double its historical average of 19x-22x.

Furthermore, the as-reported numbers imply that the market has gotten more expensive since the July article, from just 32.9x then. By looking at this data alone, it suggests investors should stay away from the market.

A lot of the potential upside seems already priced in so if as-reported net income fails to see further improvement, then equity downside will be warranted.

However, when applying Uniform Accounting, we learn that companies’ earnings have historically been materially understated.

In 2020 for example, aggregate as-reported net income was PHP 217.1 billion, but PSE-listed companies actually generated PHP 519.5 billion of Uniform earnings.

One key metric that is causing distortions in the as-reported numbers is minority interest expense.

Minority interest expense is the portion of the company’s total earnings that is attributed to the other owners of the company’s subsidiary. Since this is related to the company’s financing and not its operations, it is added back to earnings.

In 2020, Philippine corporations recorded a significant amount of minority interest expense, totaling to PHP 138.7 billion. Adding back this expense, along with the many other necessary adjustments made by Valens, leads to a much higher aggregate Uniform earnings of PHP 519.5 billion.

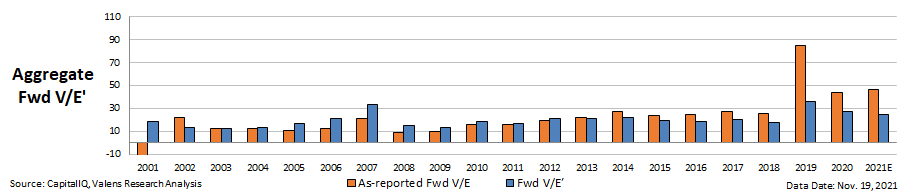

When applying the same formulas to the estimates of PSE-listed companies, we see a similar effect. As a result, Uniform Accounting reveals that the current forward V/E′ is only at a 24.6x multiple.

The current forward V/E′ is substantially lower than what as-reported metrics suggest. It is much closer to historical averages and is only a slight uptick from 23.4x in July.

While a 24.6x multiple also doesn’t suggest that Philippine stocks are cheap right now, it is at least much easier from this level for stocks to become more attractive.

If we see earnings continue to improve without the market noticing, then there is upside to be had for investors. However, opportunities like this can only be recognized through the lens of Uniform Accounting.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com