MONDAY MACRO: PHP 120 million debt on average for the PH real estate industry should not be a deal breaker, Uniform Accounting shows there is cash!

The Philippines’ economic growth over the recent years was fueled by real estate demand from Philippine Offshore Gaming Operator (POGO) and Business Process Outsourcing (BPO) companies.

However, disruptions in business activities have slowed down POGOs’ expansion. Not only that, office spaces and retail spaces for non-essential services have temporarily closed amidst the COVID-19 pandemic. Landlords or property owners are not allowed to collect rent during the quarantine period, as declared by the Republic Act 11469 or the Bayanihan to Heal as One Act.

What does this mean for the highly leveraged real estate market, especially when real estate developers have not been able to collect rent in the past two months of community quarantine? Should investors be concerned about these companies being unable to pay their debts?

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

Information Technology and Business Process Management (IT-BPM) has been the top driver of demand for the office space of the real estate sector in the Philippines.

In 2010, the Philippines overtook India’s IT-BPM in voice-based services, making us the number one country to provide these services. In order for that to happen, the local IT-BPM firms had to expand their operations, which meant a corresponding increase in demand for office space.

In 2016, another group pushed demand for office space even higher, particularly in Metro Manila. The Philippine Amusement and Gaming Corporation (PAGCOR) started processing licenses for POGOs, a group of companies that provide online gambling services to foreigners.

One of the requirements in order for them to be issued a gaming license is that they should lease a minimum of 10,000 sq. m of office space. As a result, POGO has overtaken the IT-BPM industry to be the main driver of demand for office spaces in the Philippines.

By 2019, POGO held 36% of office demand across Metro Manila because of its aggressive expansion in the country. The IT-BPM industry made up 30% of the demand for office spaces in the region while the remaining 34% belonged to traditional offices.

The recent community quarantine restrictions took a significant toll on real estate developers’ operations. Not only were they unable to collect rent during the two months in community quarantine, but they were also seeing a decline in demand for office real estate.

With the government gradually lifting the ECQ, commercial real estates will be able to partially resume their operations. However, there are still concerns on whether or not these developers have enough liquidity to cover their debts and other operating obligations.

Normally, developers take on debt from banks to fund their projects given the scale of these projects. The developers pay back their debt and interest through payments they receive from renters and buyers of their property.

Just recently, two of the top five commercial real estate companies by debt maturity have released their Q1 2020 earnings result.

SM Prime Holdings, the real estate developer of the SM Group, registered a 5% revenue decline from their Q1 2020 net income compared to their performance last year. Management reported that the lower revenues is due to their inability to fully lease during the community quarantine.

Ayala Land, Inc., a subsidiary of Ayala Corporation, reported a 17% drop in their revenue for Q1 2020, also citing disruptions because of the pandemic as a major reason for their weaker performance.

Therefore, it is understandable that many investors would be concerned about how badly these real estate developers would be hit because of the pandemic.

However, it is necessary to approach these concerns by looking at real estate companies’ true credit positions. This allows us to properly evaluate their ability to pay their obligations in the next five years.

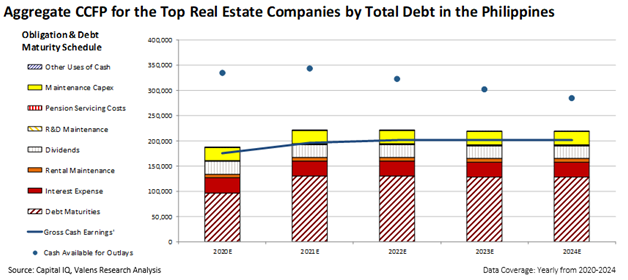

To illustrate, here are the top 5 commercial real estate companies in the Philippines with the highest debt maturities. This list includes SM Prime Holdings, Inc. (SMPH:PHL), Vista Land & Lifescapes, Inc. (VLL:PHL), Ayala Land, Inc. (ALI:PHL), Filinvest Development Corporation (FDC:PHL), and Megaworld Corporation (MEG:PHL).

The Credit Cash Flow Prime chart (CCFP) provides a snapshot of the aggregated credit health of the top five commercial real estate companies that hold the most corporate credit.

Using Uniform Accounting numbers, the bars represent the financial obligations that the commercial real estate companies need to service. These stacked bars include items like debt maturities, dividends, required reinvestment levels into the business, and rent.

The most flexible obligations would be at the top (blue stripes, or other uses of cash). These obligations could be delayed until further notice since they are of least priority. This means that the company may easily push back these payments and continue operating.

The least flexible at the bottom (red stripes, or debt maturities) are of utmost priority. If the company does not pay these, there could be serious financial repercussions in the company’s ability to operate going forward.

The blue line represents the aggregation of corporate cash flows available, while the blue circles above represent the liquidity available to the company including excess cash on hand.

Even when debt and capital requirements exceed the firm’s cash flows, as long as they still have enough cash on hand, there should be nothing to worry about for the year.

At first glance, these companies look like they would be unable to service all of their debt and operating obligations in the next five years. However, a deeper analysis tells us that these companies should have sufficient cash available for outlays going in the same period.

Moreover, these companies’ Uniform gross earnings (blue line) alone should be able to service the majority of their financial obligations, including debt maturities, in each year.

In addition, the companies’ cash available for outlays is sufficient until 2024 since they are approximately at PHP 300-350 billion levels, exceeding their debt maturities that range PHP 100-130 billion.

As we previously mentioned in our Monday Macro Report about the Philippines’ aggregate corporate credit profile, a sizable amount of cash is still available for outlays for the largest Philippine companies. This should be enough to cover their obligations and debt maturities even when their Uniform gross earnings cannot.

It may take years before the Philippines returns to its rising economic status. Fortunately, with the top debt holders in the commercial real estate industry being able to service their obligations, an industry-wide credit event is unlikely. Moreover, once the government’s initiatives and plans are put into action, this will help drive the gradual recovery of the country’s economic performance.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com