MONDAY MACRO: This chart shows why inflation shouldn’t cause much worry to investors

Textbook definition of inflation is the rate of price increases over time. Some even refer to it as an “invisible tax” because as inflation rises, consumers are able to purchase less of a good or service for each peso spent—a bit like how higher taxes limit consumers’ ability to purchase the same good or service because of lower take-home pay.

In this article, we’ll talk about another aspect of inflation and whether the Philippines might see high inflation in the future.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

With the global economy recovering from the pandemic, inflation has once again become an increasing concern. Although the Philippines has had high inflation since the start of the year, it’s only recently that other countries are following suit.

The United States, for instance, saw its highest inflation since 1990 at 6.2% in October 2021. Meanwhile, China’s inflation rate has risen to a 26-year high in October.

Many are attributing the rise in prices to the global supply chain constraints. While demand for goods has soared, supply has been unable to keep up as production has remained hindered.

The supply-demand imbalance has led producers to raise prices, effectively contributing to rising inflation.

For the Philippines, the main driver of higher inflation is the Food and Non-Alcoholic Beverage commodity group. Specifically, the price of pork has remained high despite the loosening of import restrictions.

Bangko Sentral ng Pilipinas (BSP) governor Diokno claims that the high inflation we’ve been seeing is just transitory, and he is not planning on changing interest rates to reduce inflationary pressure.

Looking at the data, the BSP governor may be right. The inflation coming from the Food and Non-Alcoholic Beverage group has been decelerating, from 6.8% in August 2021 to 5.3% in October.

That said, the BSP might not have foreseen how rapid global oil prices will increase. Inflation from the Housing, Water, Electricity, Gas, and other Fuels commodity group rose from 0.5% in January 2021 to 4.4% last month, lengthening the “transitory inflation.”

The OPEC nations have been reluctant to ramp up oil production, for fear of another COVID outbreak that would disrupt the industry again. As a result, inflation from this category may continue to be high in the near term.

However, as we’ve mentioned in last Monday’s article, all of this inflation talk is irrelevant to long-term investors. This is because the BSP controls the monetary policy tool that dictates long-term inflation.

While oil prices and food production can cause short-term volatility over inflation, only the money supply can control it over the long term.

Economists call this concept “Superneutrality of Money.” Its technical definition is that the rate of money supply growth does not affect real variables like wages and economic output.

In other words, it simply means that doubling the rate at which money in circulation grows will just double the price of everything in the long term. The country’s real GDP neither improves nor becomes worse off.

Therefore, if we expect higher inflation to persist for years in the Philippines, the BSP should be growing the money supply at a rate above historical norms according to the superneutrality of money.

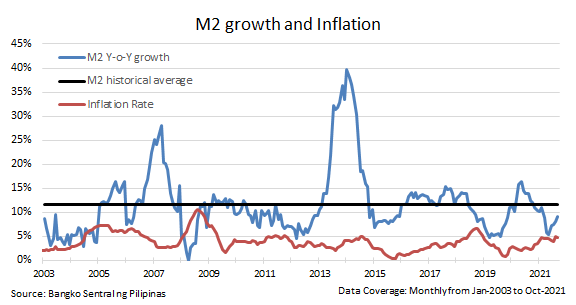

If we look at the chart below, it hasn’t actually been the case.

Historically, M2 (cash in circulation + bank deposits) grew at an average of 11.6%. Although it went above that level during Q2 2020 and Q3 2020, M2 growth has been below the line ever since.

When averaging the M2 growth of 2020 and 2021 so far, it is still only at 10.8%. This implies the BSP hasn’t enacted any policy that significantly expanded the money supply and thereby generated higher long-term inflation.

As a result, while high inflation may last longer than projected, the concept of superneutrality of money indicates that it will likely return within the BSP’s guidance of 2%-4%.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com