MONDAY MACRO: Will these 5 Philippine companies with the most debt survive the pandemic? What does their credit profile look like?

As the number of COVID-19 cases increases, more countries and territories have been implementing lockdowns and quarantines.

Businesses of all sizes have been hit one way or another, spurring talks of recession both locally and globally. While large businesses might have backup funds to continue operating, a lot of smaller businesses have either shut down or have started laying off their employees.

To further understand the impact of this pandemic, we take a look at the credit profile of five companies in the Philippines with the most debt and operating obligations.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

A recession is defined as a decline in economic activity that lasts for several months. It includes, among others, declines in real gross national product, manufacturing, and job cuts over six months.

The COVID-19 pandemic’s adverse effects to businesses have caused concerns regarding companies’ sustainability and growth potential.

When companies earn less, which is now happening because of the decline in demand for goods and services, they have less to reinvest into the firm. Any funds for growth once demand picks back up would be raised through either stock offerings or debt.

With stock market sentiment as negative as it is now, it might be difficult to fund growth through offering additional equity. The alternative is to fund growth through additional debt issuances.

When we last talked about the Philippines’ corporate credit profile, we showed that a sizable amount of cash is still available for outlays for the largest Philippine companies. This should be enough to cover their obligations and debt maturities even when their Uniform gross earnings cannot.

We highlighted that without a catalyst for credit destruction, a recession for the Philippines is unlikely. After all, negative credit events and credit destruction are necessary for a recession to occur.

The Bangko Sentral ng Pilipinas (BSP) is continuing to take an active role in managing the Philippine economy by cutting rates to stimulate the local economy. By cutting key rates and increasing the liquidity of banks, the BSP is encouraging businesses to borrow credit to boost their operations.

Of course, an excess of credit is not advisable as well, since recessions occur when corporations take on too much leverage and fail to service them. In all the major global recessions that occurred, it is very difficult to find one that didn’t start with a debt crisis.

What investors need to do is to monitor the trend of how much additional debt was taken in the next quarters to get a better understanding of how close (or far) we are to a recession.

In today’s Monday Macro Report, we feature the top five companies that are most at risk of defaulting because of the amount of total debt servicing obligations they hold for the next few years.

In order, the top five Philippine companies are as follows: San Miguel Corporation (SMC:PHL), Top Frontier Investment Holdings, Inc. (TFHI:PHL), SM Investments Corporation (SM:PHL), Petron Corporation (PCOR:PHL), and PLDT Inc. (TEL:PHL).

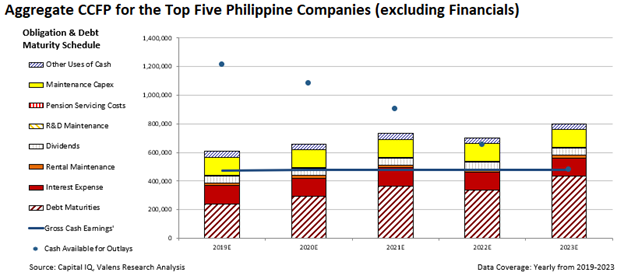

The Credit Cash Flow Prime chart (CCFP) provides a snapshot of the aggregated credit health of the top five Philippine companies that hold the most corporate credit.

Using Uniform Accounting numbers, the bars represent the financial obligations that Philippine companies need to service. This “stack” bar includes items like debt maturities, dividends, required reinvestment levels into the business, and rent.

The most flexible obligations would be at the top (blue stripes). These obligations could be delayed until further notice since they are of least priority. This means that the company may easily push back these payments and continue operating.

The least flexible at the bottom (red stripes) are of utmost priority. This means if the company does not pay these, there could be serious financial repercussions in the company’s ability to operate going forward.

The blue line represents the aggregation of corporate cash flows available, while the blue circles above represent the liquidity available to the company which includes excess cash on hand.

Even when debt and capital requirements exceed the firm’s cash flows, as long as they still have enough cash on hand, there should be nothing to worry about for the year.

At first glance, these companies look like they would be unable to service their debt and operating obligations in the next five years. However, a deeper analysis tells us that these companies should have sufficient cash available for outlays going forward until 2021.

Moreover, these companies’ Uniform gross earnings alone should be able to service the majority of their financial obligations, including debt maturities, in each year.

It also helps that with the issuance of the Republic Act 11469 or the Bayanihan to Heal As One Act, borrowers are given a 30-day grace period for loan payments without incurring any additional charges.

Meanwhile, the BSP has loosened its requirements to facilitate access to financial services while the month-long enhanced community quarantine in Luzon is in effect.

With even the most debt-heavy companies able to service their debt maturities in the near future, together with the proper fiscal and monetary assistance, it is possible to pacify recession fears in the Philippines and minimize the impact of this public health crisis.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com