Network integration solutions provided by this company have been powering the internet for decades, leading to robust Uniform ROAs of 20%+

Radio waves are one of humanity’s greatest discoveries. Radio waves power satellites, phones, and the internet, and it has enabled people to connect with each other faster and farther than ever before.

With the same mission of connectivity in mind, this company developed a multi-protocol router that could link computer systems together. Since then, the company has grown massively, offering a wide array of network integration services, and acquiring companies and shifting business models to complement growth.

While as-reported data suggests that the company’s impressive product portfolio and transformation strategy has led to only sub-10% growth, Uniform Accounting shows that its strategy has actually produced far more robust Uniform ROAs of more than 20%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

In 1867, mathematical physicist James Clerk Maxwell theorized that an electric and a magnetic field could both travel through space as an electromagnetic wave. Two decades later, this theory would be proven correct by Heinrich Hertz through a series of radio wave generation experiments.

However, it was Guglielmo Marconi who managed to put radio waves into practical use with the invention of radio transmitters. This enabled the radio waves to transmit signals farther, and allowed for longer-distance communication.

The works of Maxwell, Hertz, and Marconi collectively paved the way for the wireless revolution. Radio waves power almost all of today’s communication, from satellites, smartphones, and the internet, to name a few.

Continuous advancements in wireless technology aims to connect more people in a fast, secure, and efficient manner. Cisco Systems (CSCO) is helping further this agenda.

Cisco is the brainchild of Leonard Bosack and Sandra Lerner, who were both working at Stanford at the time. The two experimented with linking the university’s computer systems together, and managed to do so by creating the multi-protocol router.

Bosack and Lerner, who had resigned from their posts in 1986, then launched their company with the router as its main product. Since then, Cisco has grown to a $180 billion company with an expansive suite of hardware and software products.

The company specializes in cybersecurity and network integration solutions, and provides hardware and software platforms that make it possible for an organization’s network of apps, databases, and devices to interconnect securely over the internet.

Cisco is essentially a one-stop shop networking vendor.

But while the company’s switches and routers are necessary product lines, it decided to shift away from its hardware business, where revenues are relatively more cyclical, and focus more on its software business.

Similar to Adobe, Cisco also uses the software-as-a-service (SaaS) model. This means the company licenses the use of its software on a subscription basis, allowing for recurring and stable revenues.

With Cisco’s renewed focus, it was able to keep up with megatrends powering the tech industry. The company has been working on developing cloud platforms, which has become increasingly significant in modern business operations.

Additionally, the company has also been working on the Internet-of-Things (IoT). Its products make it easier to connect and control smart devices, like microwaves or even cars, from a smartphone. Given the company’s connectivity capabilities, working on IoT is exactly right up its alley.

While it continues to grow organically, Cisco has also made acquisitions to aid in the hardware-to-software transition, to expand its market reach and achieve market dominance.

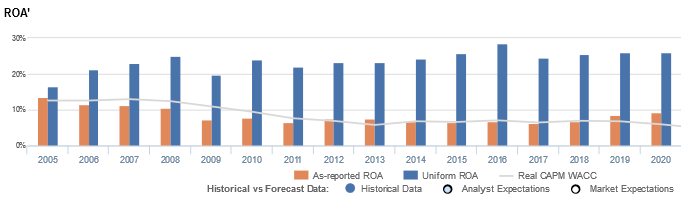

Cisco’s brand strength, robust product portfolio, and massive consumer base make it easier for the company to carry out its growth initiatives. However, looking at as-reported metrics, it appears its growth came at the cost of lucrative profitability, with return on assets (ROAs) falling from 13% in 2005 to just 9% in 2020.

In reality, thanks to Cisco’s comprehensive offerings and proper strategic focus, it has been able to execute growth profitably. Uniform ROAs have been remarkably robust, reaching north of 16% in each of the past sixteen years.

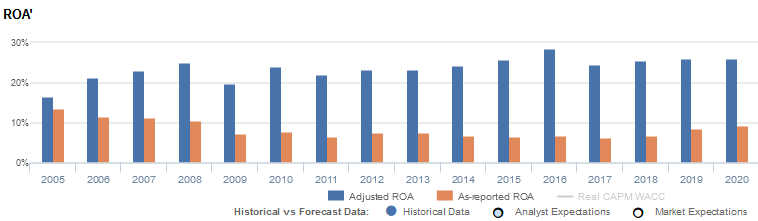

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Cisco’s balance sheet. Due to its acquisitions for growth, the company’s goodwill has ranged from $25 billion to $35 billion, or at least 20% of its total assets in recent years.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Cisco’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing poorly. In fact, it is the opposite, with returns that are 3x greater.

Cisco’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Cisco’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 9% in 2020, but its Uniform ROA was actually nearly 3x higher at 26%.

Specifically, Cisco’s Uniform ROA has ranged from 17% to 29% in the past sixteen years while as-reported ROA ranged only from 7% to 13% in the same timeframe.

Uniform ROA expanded from 17% in 2005 to 25% in 2008, before falling to 20% in 2009 and rebounding to a peak of 29% in 2016. Then, after dropping to 25% in 2017, Uniform ROA recovered to 26% levels in 2018-2020.

Cisco’s Uniform earnings margins are generally weaker than you think, but its Uniform asset turns slightly make up for it

Cisco’s overall improvements in profitability have been driven by trends in Uniform earnings margins, coupled with stable Uniform asset turns.

Uniform margins slowly expanded from 17% in 2005 to 24%-25% levels in 2016-2020. Meanwhile, since 2005, Uniform turns have maintained at 1.0x-1.1x levels.

At current valuations, the market is pricing in expectations for Uniform margins to slightly fade and for Uniform turns to sustain current levels.

SUMMARY and Cisco Tearsheet

As the Uniform Accounting tearsheet for Cisco Systems, Inc. (CSCO) highlights, the Uniform P/E trades at 17.4x, which is below corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Cisco, the company has recently shown a 6% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cisco’s Wall Street analyst-driven forecast is a 4% EPS shrinkage in 2021 and a 12% EPS growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cisco’s $45 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings decline 4% each year over the next three years and still justify current prices. What Wall Street analysts expect for Cisco’s earnings growth is in line with what the current stock market valuation requires in 2021 but above this requirement in 2022.

Furthermore, the company’s earning power is 4x the corporate average. Also, cash flows and cash on hand are 3x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Cisco’s Uniform earnings growth is in line with its peer averages in 2021, but the company is trading below its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com