No hurdle is going to stop this utility company’s stable income flow, with Uniform ROAs doing better than as-reported

Companies under the utilities sector are considered defensive stocks because of their relatively stable demand and earnings even through economic downturns. However, for these companies, growth is often limited.

This utilities company’s profitability has been declining in the past 15+ years, but not to the extent that as-reported metrics suggest.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Utilities stocks are quite special compared to other sectors. Since the products and services they provide are considered basic necessities vital to live, companies in this sector are heavily regulated.

Because of these regulations, it can be quite challenging for existing companies to expand and for new companies to enter the market.

We’ve talked about one utility company in the past, the electric power distribution company Manila Electric Company (MER:PHL), which had to deal with government regulations while trying to turn a profit for themselves.

Another company that operates under the utilities sector is Manila Water Company (MWC:PHL). Manila Water is the exclusive provider of the East Zone of Metro Manila and Rizal province.

Before Manila Water became the exclusive water provider in those areas, only 26% of the East Zone’s population had access to a 24-hour water supply. Moreover, there was 63% water loss from leakages and pilferages.

To resolve the water supply problem in the East Zone, the government decided to privatize utility operations. Manila Water was able to win the bid for the East Zone and became regulated under Metropolitan Waterworks and Sewerage System (MWSS).

Manila Water spent PHP 166 billion to improve water and wastewater services, resulting in water availability in the area increasing from 26% to nearly 100%. Water loss significantly declined to less than 15%, translating to about 700 million liters of water saved per day.

Since Manila Water exclusively provides water in the East Zone, one of the most densely populated locations in the country, investors would expect the company to earn substantial income from supplying a basic necessity.

However, it doesn’t look like the company is able to effectively utilize its assets and investments to generate earnings.

Even though Manila Water started expanding its wastewater services in 2017, infusing a total of PHP 13.3 billion of capital expenditures or a 49% increase from previous year’s spending, it wasn’t able to turn around the declining trend of its Uniform ROA since 2006.

Then, the company’s situation was further aggravated in 2019 after it faced a water supply shortage due to El Niño, resulting in decreased net income.

Since the company belongs to a heavily regulated sector, it also has to deal with more intense government scrutiny. At one point in 2019, there was even a threat of the Philippine government seizing its (and fellow water utility company Maynilad’s) operations and assets for delaying construction projects.

In 2020, another challenge in Manila Water came when the contributions from its domestic subsidiaries had slowed down due to the pandemic, resulting in an 18% decline in its profitability. The increase in residential consumption was not enough to offset revenue declines from its other business units.

That said, analysts are optimistic about the company’s outlook, particularly with the changes in Manila Water’s management and board.

Enrique Razon, the third richest man in the country, was recently appointed as the new Chairman, President, and CEO of the company, following the PHP 14.58 billion shares subscription through Trident Water, a subsidiary of Razon’s Prime Strategic Holdings. In effect, this means Razon has 51% voting interest in the company.

Prime Strategic’s interests in the current Wawa Bulk Water Supply project at Wawa Dam will likely be beneficial for Manila Water. Once the project is completed, it will act as another source of water supply for the company, addressing any water shortage concerns in the future.

Overall, with the recent hurdles it faced, one might think that Manila Water has struggled to remain profitable.

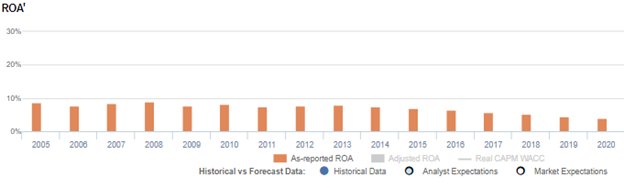

As-reported metrics seem to agree, implying a severe collapse with as-reported ROA falling from 9% in 2005 to below cost-of-capital at 4% in 2020.

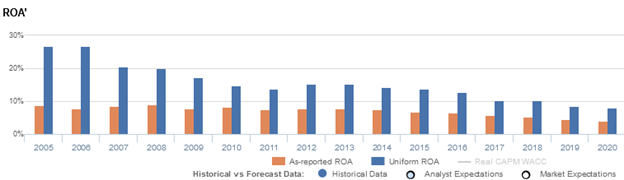

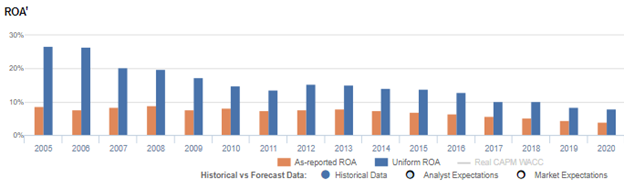

In reality, although the company has seen declining returns, it is not as weak as as-reported metrics suggest. Though Uniform ROAs fell from 27% in 2008 to 8% in 2020, this is still stronger than as-reported metrics show and is still above cost-of-capital levels.

One of the said distortions for the discrepancy is due to the treatment of amortization expense according to the Philippine Financial Reporting Standards (PFRS).

Analyzing Manila Water’s financial statements, the amortization of “service concession assets” is the largest expense impacting earnings. Its non-cash nature means that it does not represent an actual outlay of cash every time amortization is recorded.

Additionally, post-2016, amortization of some intangible assets changed from a straight line basis to the unit of production method. This made Manila Water’s intangible assets less comparable against pre-2016 results or against its direct peer, Maynilad.

Therefore, in addition to the many other adjustments made, amortization expense is added back to calculate Manila Water’s true earnings power.

In 2020 alone, if we add amortization expense of PHP 2.9 billion back to earnings and with many other important adjustments Valens made, we arrive at PHP 8.7 billion Uniform earnings and 8% Uniform ROA, higher than PHP 4.5 billion as-reported net income and 4% as-reported ROA.

Manila Water’s earning power is more robust than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Manila Water’s profitability is weaker than what real economic metrics highlight.

In reality, Manila Water’s true profitability has generally been higher than its as-reported ROA for the past sixteen years.

Uniform ROA gradually declined from 27% in 2005 to 14% levels in 2011, before recovering to 15% in 2012-2013, but this improvement did not last as the company saw declining returns again, hitting an all-time low of 8% recently.

Meanwhile, as-reported metrics suggest that Manila Water has struggled to surpass 10% profitability historically, only ranging from 4% to 9% in the past sixteen years.

Manila Water’s asset turns are stronger than you think

The strength of their ROA lies on their asset turns. This implies that the company is more concerned about generating sales for every dollar spent in assets.

Beginning 2003, the difference between Manila Water’s Uniform and as-reported ROA was historically broader, similar to the difference between Uniform and as-reported asset turns.

For example, the as-reported asset turns for Manila Water have been in the range of 0.1x-0.3x historically, lower than Uniform asset turns of 0.2x-0.5x.

The as-reported numbers make Manila Water appear less efficient in churching revenue out of their asset base than real economic metrics highlight. It also distorts the market’s perception of the firm’s historical asset efficiency trends.

SUMMARY and Manila Water Company, Inc. Tearsheet

As the Uniform Accounting tearsheet Manila Water Company, Inc. (MWC:PHL) highlights, it trades at a Uniform P/E of 11.7x, below the global corporate average of 23.7x but around its historical average of 10.5x.

Low P/Es require low EPS growth to sustain them. In the case of Manila Water, the company has recently shown a 5% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Manila Water’s sell-side analyst-driven forecast calls for 9% and 6% EPS growth for 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Manila Water’s PHP 18.68 stock price. These are often referred to as market embedded expectations.

Manila Water is currently being valued as if Uniform earnings were to shrink by 8% annually over the next three years. What sell-side analysts expect for Uniform earnings growth is above what the current stock market valuation requires in 2021 and 2022.

The company’s earning power is above the long-run corporate average. On the other hand, cash flows and cash on hand are almost 2x its total obligations, with intrinsic credit risk of 730bps above the risk free rate. Together, this signals high credit risk.

To conclude, Manila Water’s Uniform earnings growth is in line with its peers, and the company currently trades below average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com