PH Monday Macro: Don’t look at total sovereign debt, look at the debt service budget

In order to make up for the drop in economic activity in 2020, the Philippine government had to run a wide deficit. This deficit caused the national government debt to balloon.

Though it may seem that the 62% sovereign debt relative to GDP is a concern, this key metric tells us there is no reason to worry.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

Global markets have been worried about the U.S. debt ceiling. The U.S.’s high total public debt has investors spooked about its ability to service its current debt obligations and if, at this state, it would be able to borrow more.

However, we are not concerned. After all, the U.S. still remains a global superpower, and that is enough reason for it not to default.

What about the Philippines? Should we worry about our national debt?

The national debt, commonly referred to as public debt or sovereign debt, is the total debt owed to the country’s creditors and the sum of the past deficit, where a deficiency occurs when the government spends more than what they have earned.

Just like consumers and businesses, when the government revenue is inadequate to cover its expenses, to make up for the difference, the government borrows money.

Similar to a normal borrower, the country has multiple debt facilities, such as borrowing from other countries, multilateral agencies, or international securities issuance.

In 2020, national lockdowns that led to a plummet in economic activity pushed the government to borrow money and spend more than it earned from tax revenue. This caused a significant shortfall of the PHP 1.3 billion budget deficit for 2020.

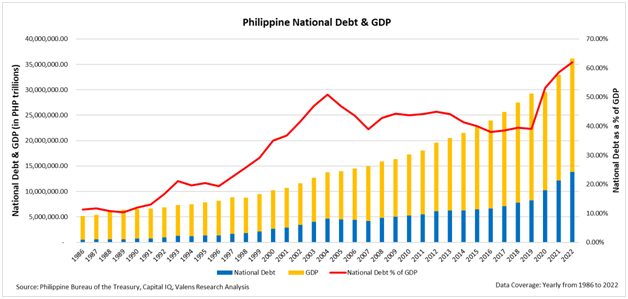

As a result, this has pushed the Philippine national debt to more than half of the 2022 annual GDP. Take a look…

The portion of debt relative to the value produced by the country ticked at 62%. To put this into perspective, imagine a person with a debt of 60% more than their net worth or a company having more than 60% of debt obligations relative to its intrinsic value.

Concerning how it sounds, modern economic theory suggests that debt as a percentage of GDP should not be considered an indicator. One reason for this is that, unlike an individual or business entity, countries are backed by the sovereign faith of the nation.

So, since the full faith of the Philippines backs national credit, the country can borrow infinite money in accordance with its credit risk. Such a theory eliminates the concern regarding the debt level the country can borrow.

Instead, what should be a concern is the level of money being paid to service the debt; in other words, the debt service. These are the interest payments and principal the country is paying to its lenders.

This measurement is more accurate for gauging the degree of risk because it shows how much capital the country is paying relative to the value that the country produces. When this figure increases, the government either raises taxes or lowers spending in other areas.

Both alternatives can mean lower productivity output because raising taxes will discourage spending due to the added cost, while lower spending in other areas will decrease the budget for operating the country and investments for more potential growth.

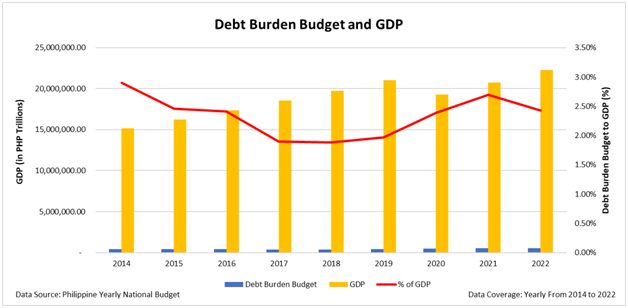

As shown above, we can see that debt service relative to GDP trends steadily. Between 2014 and 2022, the portion of the national budget allocated to pay the country’s debt ranged between 1.8% and 2.9% of total economic output.

In the last decade, the Philippine government and the past two presidential administrations did not significantly increase their yearly budget for debt service. Such cases suggest that the government maintains its capital issuance for debt throughout the years, not affecting long-run productivity caused by raising taxes or decreasing its investments for growth.

Overall, despite a 62% of total debt relative to the total economic output of the Philippines, investors should not be concerned as the interest payments to service the debt is at steady levels.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com