Shopping with rewards further boosted this company’s digitalization initiatives, launching a 10% Uniform ROA, not 4%

In the midst of a pandemic, one important lesson that retailers learned is that digitalization is a must to survive and thrive in the industry.

Today’s company is currently taking significant actions to turn its business around in the online space given the lower foot traffic in malls brought about by the stay-at-home protocols.

Though as-reported metrics make it look like this company is still generating the same historical profitability levels, Uniform Accounting shows that this company can generate higher returns partly thanks to its digitalization efforts.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In 2015, there were about 44 million active Internet users in the Philippines. As of 2020, over 73 million Filipino users are active online.

Though the number of online users–and presumably the number of e-commerce customers–increased, the Philippines has one of the lowest percentages of e-commerce users in Southeast Asia. This is largely because of how significant the mall culture is to Filipinos, as evidenced by our many sprawling malls in Metro Manila.

However, all that has changed because of the pandemic. With malls temporarily closed, Filipinos turned to online businesses. A study showed that online shoppers in the Philippines grew by 57% in the first half of 2020, the highest in the Southeast Asian region.

This rapid change in consumer behavior has led many to wonder if retailers will ever adapt and recover.

CEO and President of JG Summit Lance Gokongwei aimed to answer that question in his talk, “Navigating the New Normal,” on March 17 for the Penn-Wharton Club of the Philippines. Gokongwei stated that a lot of changes in customer behavior are permanent, and what would have taken five to ten years for digital transformation took only a year because of the pandemic.

To survive and thrive today, businesses should have an ecosystem that can adapt to quickly changing consumer buying behavior in the retail industry.

One company that had started building this ecosystem even before the pandemic is Robinsons Retail Holdings, Inc. (RRHI:PHL).

Robinsons Retail is a company that operates in almost every retail market. Among its many business lines, it owns department stores, toy stores, and drug stores, but the supermarkets are the most significant in terms of revenues.

Since 2010, the supermarket business has been the firm’s largest source of revenue, driven mostly by the Robinsons Supermarket brand, which makes up essentially half of Robinsons Retail’s sales.

Although the company started its digitalization initiatives in 2019, it wasn’t until the pandemic struck in 2020 that its development became even more important. In order to thrive in a competitive industry, Robinsons Retail decided to refocus its spending away from physical stores, cutting its capital expenditures budget to a maximum of PHP 4 billion in 2020 from a maximum of PHP 5 billion in 2019.

Robinsons Retail’s focus on going digital includes utilizing other big third party platforms, such as Lazada, Shopee, and GrabMart, in order to further strengthen its online presence. It also developed its own mobile app called gorobinsons.ph, which had six brands by the end of 2020. Three of those brands are supermarkets, namely Robinsons Supermarket, Shopwise, and The Marketplace, with the latter being a result of the company’s acquisition of Rustan Supercenters in 2019.

Aside from ramping up its omnichannel, the company also delved into its customer acquisition strategy to retain customers by launching the app for the firm’s Robinsons Rewards Card in 2019. Customers can shop online and track their points through the app, while the card helps the company understand their sales and marketing efforts.

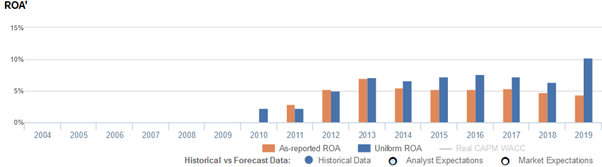

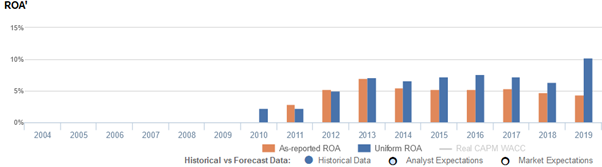

Robinsons Retail’s focus and success in its digitalization efforts and its recent supermarket acquisition may make investors think the company is generating higher profitability. However, looking at as-reported metrics, it appears that these strategies have not helped Robinsons Retail produce stellar returns, with return on assets (ROAs) falling below cost-of-capital levels in 2019.

In reality, Uniform Accounting shows that Robinsons Retail’s ability to capitalize on these initiatives has generated improving returns, with Uniform ROAs reaching a peak of 10% in 2019.

Similar to most mergers and acquisitions, management teams often pay a premium for the acquired assets, which increases the goodwill on the company’s balance sheet.

Although required to be reported on Philippine Financial Reporting Standards (PFRS), goodwill artificially inflates the company’s asset base. It is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating assets.

Therefore, goodwill should be removed from the company’s assets.

With the PHP 13.8 billion Rustan Supercenters acquisition in 2018, Robinsons Retail recognized an additional PHP 9.1 billion of goodwill. This led the company’s goodwill to balloon to PHP 12.5 billion, accounting for nearly 10% of its total as-reported assets in 2019.

Removing goodwill and applying other necessary adjustments, Robinsons Retail’s 4% as-reported ROA and PHP 137.9 billion asset base are adjusted to be only PHP 108.1 billion of Uniform assets, revealing a TRUE Uniform ROA of 10%.

Robinsons Retail’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Robinsons Retail’s profitability has been weaker than real economic metrics have highlighted.

In reality, Robinsons Retail’s true profitability has been lower than its as-reported ROA for the past six years. Specifically, as-reported ROA was 4% in 2019, but Uniform ROA was higher at 10%.

After expanding from 3% levels in 2011 to a high of 7% in 2013, as-reported ROA has since slowly faded to 4% in 2019.

Meanwhile, Uniform ROA rose from 2% levels in 2010-2011 to 7% in 2013, before compressing to 6% levels in 2018. Since then, Uniform ROA has jumped to a peak of 10% in 2019, following the Rustan Supercenters acquisition.

Robinsons Retail’s margins have been weaker than you thought

Improvements in Uniform ROA have been driven by improving Uniform earnings margins. However, Uniform margins were lower than as-reported EBITDA margins in each of the past nine years.

As-reported EBITDA margins improved from 4% levels in 2010-2011 to 8% in 2013, before stabilizing at 7%-8% levels all the way through 2019.

Meanwhile, after jumping from 1% levels in 2010-2011 to 6% levels in 2015-2016, Uniform ROA declined to 5% levels in 2017-2018. Since then, Uniform ROA has jumped to a peak of 7% in 2019.

Looking at the firm’s margins alone from 2010-2018, as-reported metrics make the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and Robinsons Retail Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for Robinsons Retail Holdings, Inc. (RRHI:PHL) highlights, it trades at a Uniform P/E of 12.4x, below the global corporate average of 25.2x, and its historical average of 17.7x.

Low P/Es require low EPS growth to sustain them. In the case of Robinsons Retail, the company has recently shown a 25% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Robinsons Retail’s sell-side analyst-driven forecast calls for a 4% and 13% Uniform EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Robinsons Retail’s PHP 52.20 stock price. These are often referred to as market embedded expectations.

Robinsons Retail is currently being valued as if Uniform earnings were to shrink 8% annually over the next three years. What sell-side analysts expect for Robinsons Retail’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is above the long-run corporate average. However, cash flows are almost 2x its total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 200bps above the risk free rate. Together, this signals a low dividend and credit risk.

To conclude, Robinsons Retail’s Uniform earnings growth is the highest among peers in 2020, and trades below its average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com