This airline is keeping its business at cruising altitudes through refinancing and refocusing strategies, sparking above cost-of-capital Uniform ROAs

A year ago, the pandemic severely disrupted the operations of airline companies all over the globe, raising bankruptcy fears across the industry.

This piso-fare company is doing its best to keep its business afloat by revitalizing its focus on its cargo fleet, refinancing its debt, and still launching piso-fare promos.

However, despite generating strong profitability in the past, many investors sold their shares due to the still-present uncertainties that the airline industry is experiencing.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In the early 20th century, air travel was a luxury few were able to afford on a regular basis. The cost of flying was expensive due to high jet fuel prices. Nowadays, with cheaper oil and jet fuel prices and increased competition in the airline industry, many have been offering low fares that can accommodate everyone who wants to travel by air.

That’s where the “Piso Fare” comes in.

In recent years, the “Piso Fare” offers have become one of the Philippines’ most anticipated and sought after sales promo in the airline industry. While we don’t really pay a peso for the entire trip, this deal can make it ridiculously cheap to travel 10,000 miles by plane.

Cebu Air, Inc. (CEB:PHL, aka Cebu Pacific), the creator of the piso fare promo, was established for this reason—to address the need for a budget airline in the Philippines.

As we discussed in our PMD article for Cebu Pacific last year, the company fashioned its business model after Southwest Airlines’ by keeping its costs and prices as low as possible by removing the nonessentials from the flight experience.

Passengers are instead charged extra for food, refreshments, and additional luggage. The airline also takes on shorter routes and lands on cheaper airports to minimize expenses.

This way, they attract the low-budget high frequency flyers, expecting that these customers will generate the same amount of revenue as the wealthier but low frequency passengers.

As a result, Cebu Pacific now has a substantially larger customer base than that of other traditional airlines.

However, offering cheaper fares is a double-edged sword. Numerous instances of air travel cancellations can quickly eat into the firm’s earnings, since they operate on such low margins.

This happened to Cebu Pacific a year ago when travel restrictions were imposed in the country due to coronavirus concerns. The firm does not have a choice but to issue refund and travel credits, negatively affecting the firm’s profitability and stock price.

With the refunds it issued, Cebu Pacific reported a loss of PHP 9 billion during the first half of 2020.

These events have influenced the market to become too bearish on the firm, exaggerating Cebu Pacific’s inability to bounce back.

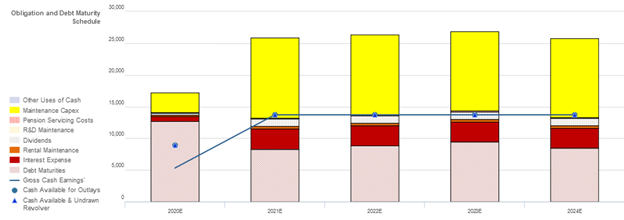

Many investors have speculated about Cebu Pacific’s potential bankruptcy, especially with the firm’s financial obligations and debt maturity of PHP 12.7 billion in 2020. Recently, it announced it would offer dollar-denominated convertible preferred shares from Feb. 26, 2021 to March 4, 2021 to refinance its debt.

Assuming the refinancing is a success, the company may need to inject new capital to be able to service its operational and debt obligations in the next few years.

Despite these recent headwinds due to the pandemic and its current credit profile, the company was able to adapt to the pandemic by recalibrating its business to focus more on its cargo fleet business.

With more people staying at home, online purchases have skyrocketed, which led to an increase in shipments globally.

As a result, Cebu Air has converted its ATR 72-500 aircraft into its second cargo freighter at a facility in Dinard, France, with the first freighter being remodified there too.

While travel sales remain uncertain, the company’s cargo business, which is around 7% of the company’s total revenue, is expected to flourish amidst the ongoing pandemic. This could possibly spark an opportunity for Cebu Pacific in the long term, beyond its commercial airline business.

Although these factors might help the firm survive its current predicament, Cebu Pacific’s issue with its credit profile, along with the low demand for air travel, may still drag down its recovery.

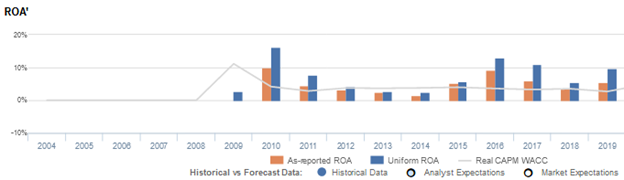

Moreover, as-reported metrics show that Cebu Pacific returns barely surpass the cost of capital at only 6%, making investors even more worried about the company’s recovery.

However, Uniform Accounting shows that Cebu Pacific’s profitability has never been below 6% in the last five years.

In 2019, Cebu Pacific’s as-reported ROA was at 6%, whereas its Uniform ROA was actually at 10%. What as-reported metrics missed here is in the accounting of interest expense.

Interest expense represents the costs of taking on debt, but Philippine Financial Reporting Standards (PFRS) allows the item to be classified as an operating cash flow. In reality, it is not part of the company’s operations and should always be classified as a financing cash flow.

As such, interest expense is added back to earnings to reflect the company’s true profitability. For Cebu Pacific, the company recognized an interest expense of PHP 3 billion in 2019.

Applying the interest adjustment to earnings, along with the many other necessary adjustments made, we arrive at a PHP 10.8 billion Uniform earnings and a 10% Uniform earning power for Cebu Pacific in 2019.

Cebu Pacific’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Cebu Pacific’s profitability has been weaker than real economic metrics have highlighted in the past fourteen years.

In reality, Cebu Pacific’s true profitability has been higher than as-reported ROA since 2010. Specifically, Uniform ROA was 10% in 2019, but as-reported ROA was only 6% that year.

After falling from 10% in 2010 to 2% in 2014, as-reported ROA improved to 9% in 2016. Then, as-reported ROA declined to 4% in 2018, before expanding to 6% in 2019.

In contrast, after declining from 16% in 2010 to 3% in 2014, Uniform ROA gradually improved to 13% in 2016, before compressing to 6% in 2018 and expanding to 10% in 2019.

Cebu Pacific’s earnings margin is weaker than you think

Cyclicality in Uniform ROA has been primarily driven by trends in Uniform earnings margin. In fact, as-reported margins have been higher than Uniform margins in each of the past eleven years.

As-reported margins improved from 22% in 2009 to 31% in 2010, before fading to a low of 13% in 2014 and subsequently recovering to 34% through 2016. Since then, as-reported margins declined to 28% in 2019.

Meanwhile, Uniform margins rose from a low of 3% in 2009 to a peak of 23% in 2010, before compressing back to 3% in 2014 and rebounding to 21% in 2016. Thereafter, Uniform margins regressed to 13% in 2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost efficient business than is accurate.

SUMMARY and Cebu Air, Inc. Tearsheet

As the Uniform Accounting tearsheet for Cebu Pacific (CEB:PHL) highlights, it trades at a Uniform P/E of -424.x, below the global corporate average of 25.2x and its historical average of 16.9x, excluding 2019 and 2020.

Low P/Es require low EPS growth to sustain them. In the case of Cebu Pacific, the company has shown a 72% Uniform EPS growth in 2019, before the pandemic-induced crisis.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Cebu Pacific’s sell-side analyst-driven forecast calls for a 287% and 81% Uniform EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cebu Pacific’s PHP 48 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 16% each year over the next three years and still justify current valuations. What sell-side analysts expect for Cebu Pacific’s earnings growth is below what the market requires in 2020 and 2021.

Furthermore, the company’s earning power is 2x the long-run corporate average, and cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high credit and dividend risk.

To conclude, Cebu Pacific’s Uniform earnings growth is below peer averages, and the company is also trading below peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com