This cement company shows how the product isn’t the only stepping stone to profitability, generating TRUE returns 2x as-reported ROAs

In many industries, product differentiation is difficult to achieve. While many continue to pursue this endeavor, others opt to focus on other aspects of the business.

This cement manufacturer has been able to generate positive returns by focusing on a distribution strategy different from its peers. However, as-reported metrics think the company is barely economically profitable.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

To the untrained eye, cement comes in only one multifunctional form. Contrary to what the regular juan may know, there are actually a lot of different types of cement, depending on its use.

The most common is Ordinary Portland cement, which is used for general construction. Another is Pozzolana cement, which is better suited for structures heavily exposed to water.

While there are many other types, the Philippines is known to be the only producer of Type 1P cement, which is the combination of Portland and Pozzolana.

Despite the wide variety of cement choices, no company has a monopoly on a particular type. A competitor can always offer a product with the same properties. As such, it is difficult to utilize a product differentiation strategy in this industry.

The Philippines’ major cement companies instead rely on other parts of the business to create an advantage.

A while back, we talked about how Eagle Cement (EAGLE:PHL) managed to generate robust returns through its production strategy. Instead of building multiple factories in high-demand areas, Eagle Cement built the country’s largest factory right in the middle of its key markets.

Meanwhile, CEMEX Holdings Philippines, Inc. (CEMEX:PHL), another major player, is focusing on the distribution side of the business for its advantage.

Cement companies often derive most of their sales from institutional clients such as large construction companies, wholesalers, and the government. These customers buy in massive quantities, which is good for their top line. However, the concentration of sales to a single customer—or a few customers—has its own risks.

CEMEX Philippines, however, distributes more to the smaller retailers like the hardware stores. The sales per customer are significantly less, but fierce competition in this space is less likely.

Furthermore, most of the cement companies negotiate for some of their customers to pick up the product from the plant itself, while CEMEX Philippines mostly delivers its product directly to the customers.

As a result, CEMEX Philippines has a more extensive and optimized distribution network than many of its peers, owning 22 marine and land distribution centers across the country. Just for comparison, Eagle Cement only owns 4 distribution centers and uses more trucks.

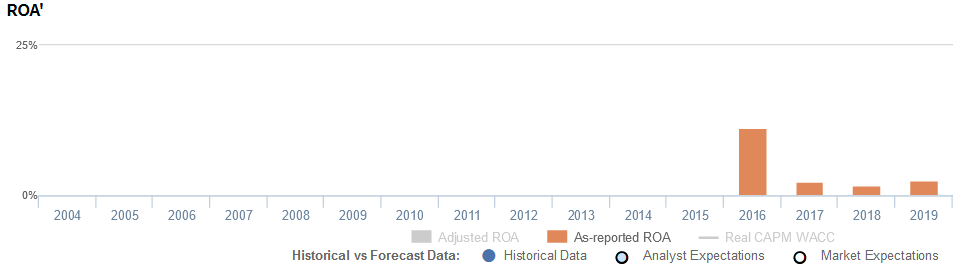

However, as-reported metrics aren’t accurately reflecting the benefits CEMEX Philippines’ distribution strategy brings. Since 2017, as-reported ROA has only hovered around 2%-3% levels, barely generating economic returns.

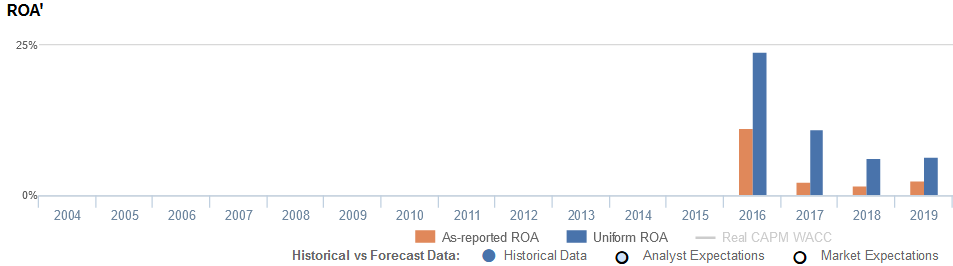

Looking at the Uniform metrics, we see the distribution strategy’s real value. As of 2019, CEMEX Philippines’ Uniform ROA is actually much higher, more than double as-reported at 7%.

As-reported metrics materially understate CEMEX Philippines’ profitability largely because of how goodwill, among many other accounting distortions, is treated.

As is the case with most mergers and acquisitions, management teams often pay a premium for the acquired assets, which increases the goodwill in the company’s balance sheet.

Although required by the Philippine Financial Reporting Standards (PFRS), goodwill artificially inflates the company’s asset base. It is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating assets.

Therefore, goodwill should be removed from the company’s assets.

Since 2016, CEMEX Philippines has been holding PHP 27.9 billion of goodwill in the balance sheet, making up nearly half of the company’s as-reported assets in 2019.

Removing goodwill from CEMEX Philippines’ assets, along with the many other necessary adjustments made, leads to a 7% Uniform ROA in 2019, significantly higher than as-reported ROA of 3%.

CEMEX Philippines’ earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think CEMEX Philippines’ profitability has been weaker than real economic metrics have highlighted in the past sixteen years.

In reality, CEMEX Philippines’ true profitability has been higher than as-reported ROA since 2016. Specifically, Uniform ROA was 7% in 2019, but as-reported ROA was only 3% that year.

After dropping from 11% in 2016 to 2% in 2017, as-reported ROA has since maintained 2%-3% levels through 2019. Meanwhile, Uniform ROA has been more robust, declining from 23% in 2016 to 11% in 2017 before sustaining 6%-7% levels through 2019.

CEMEX Philippines’ asset turns are stronger than you think

Strength in Uniform ROA has been driven primarily by strong Uniform asset turns. In fact, Uniform turns have been materially higher than as-reported turns in each of the past four years.

Since 2016, as-reported turns have remained at 0.4x-0.5x levels. Meanwhile, Uniform turns have been greater, ranging from 1.1x-1.7x levels over the same time period.

Looking at the firm’s turns alone, as-reported metrics are making the firm appear to be a less asset efficient business than is accurate.

SUMMARY and CEMEX Holdings Philippines, Inc. Tearsheet

As the Uniform Accounting tearsheet for CEMEX Holdings Philippines, Inc. (CHP:PHL) highlights, the Uniform P/E trades at a 45.2x, which is above global corporate averages and its own history.

High P/Es require high EPS growth to sustain them. That said, in the case of CEMEX Philippines, the company has recently shown a 7% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, CEMEX Philippines’ sell-side analyst-driven forecast calls for a 347% and 57% Uniform EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CEMEX Philippines’ PHP 1.45 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow by 8% each year over the next three years to justify current valuations. What sell-side analysts expect for CEMEX Philippines’ earnings growth is well below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is near the long-run corporate average, but cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high credit and dividend risk.

To conclude, CEMEX Philippines’ Uniform earnings growth is well below peer averages, but the company is trading well above peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com