This company controls its business through partnership and innovation, reaching a Uniform ROA of 9%, not 7%

As one of the most successful family-controlled businesses in the Philippines, this company managed to push for growth through partnerships and innovation. However, as-reported metrics show that it is only generating modest returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In the Philippines, almost 80% of the businesses are family-controlled firms, consisting of big names such as the SM Investments Corporation (SM:PHL), Aboitiz Equity Ventures, Inc. (AEV:PHL), and Ayala Corporation (AC:PHL).

Another one that is included in this roster of successful family-controlled businesses is D&L Industries, Inc. (DNL:PHL), a manufacturer of specialty food ingredients and chemicals.

D&L Industries was founded by brothers Dean and Leon Lao in 1963, selling colorants to the plastic industry. The business was so successful that several years later, three other Lao brothers joined the company to grow the business.

Currently, it manufactures a variety of products, including food components, personal and home care chemicals, plastic raw materials, and aerosol products, all of which are fueled by investments in research and innovation.

So far, the company’s success has been mostly attributed to developing partnerships and carefully planning its strategies. It was able to sign a supply agreement with Ventura Foods back in 2014, allowing it to develop and manufacture specialized oils and specialty ingredients for the American company in the Asia-Pacific region.

To further strengthen its export business, D&L Industries decided to form more partnerships with other global food manufacturing businesses. One of which is through D&L Industries’ subsidiary, Oleo-Fats, sealing a deal with New York-based company, Bunge Ltd, a global agribusiness and food company in 2016.

Due to these collaborations, the company’s food ingredients divisions became the greatest contributor to its exports by the end of 2017, accounting for 45% of total export sales, which was up from 19% in 2016.

Moreover, in 2018, D&L Industries’ planned expansion of its food business came to life with the development of its Batangas facility. As of date, it has already fully secured finance for this plan after a successful maiden bond offering valued at PHP 5 billion.

According to the company, this facility is anticipated to be a world-class manufacturing plant with cutting-edge R&D capabilities that would boost exports, living up to its position as the Philippines’ innovation powerhouse.

Despite having a significant negative influence on other industries, the COVID-19 pandemic has actually had little impact on D&L Industries as its export business remained robust, with sales increasing by 70% in 2021.

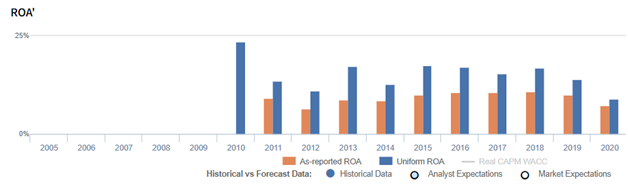

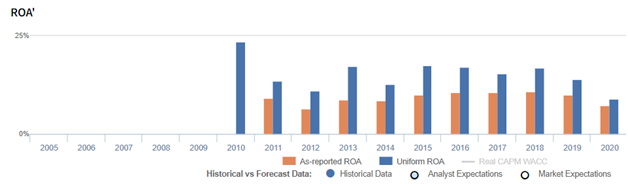

However, looking at as-reported metrics, it appears that D&L Industries’ drive for growth is not generating enough shareholder value, with return on assets (ROAs) only reaching a peak of 11%.

In reality, D&L Industries’ strength in its export business as well as its continued focus on expansion initiatives have actually proved that the company actually did much better than expected, with Uniform ROAs achieving a peak of 18% in the past ten years.

One reason behind the distortion in the as-reported figures comes from the accounting treatment of goodwill. Since its acquisitions in 2014, D&L Industries has been recording PHP 3.4 billion worth of goodwill, representing 15% of its as-reported assets.

Goodwill is purely accounting-based and is not actually used in the company’s operations. This falsely inflates the asset base and makes D&L Industries appear to be a less profitable business.

If we remove PHP 3.4 billion goodwill from D&L Industries’ asset base and apply the many other necessary adjustments that Valens makes under Uniform Accounting, we arrive at a 9% Uniform ROA for 2020, greater than its 7% as-reported ROA.

D&L Industries’ earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Through Uniform Accounting, we can see that D&L Industries’ true ROAs have been mostly understated in the past eleven years. For example, as-reported ROA was 7% in 2020, but its Uniform ROA was actually higher at 9%.

Looking at historical performance, from 2012-2018, we see that as-reported ROA improved from 6% to 11% levels, before declining to 7% in 2020.

On the other hand, after jumping from 11% in 2012 to 17% in 2013, Uniform ROA dropped to 13% in 2014. Thereafter, Uniform ROA rebounded to 15%-18% levels in 2015-2018, before slowly fading to 9% in 2020.

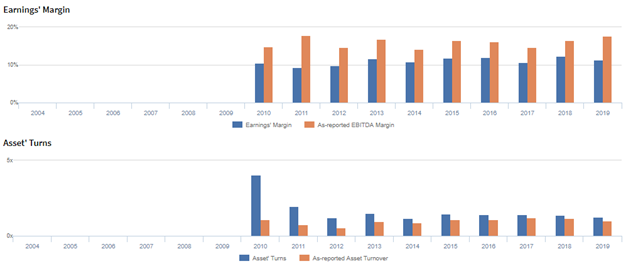

D&L Industries’ margins are weaker than you think, but its strong Uniform asset turns make up for it

Trends in Uniform ROA have been driven primarily by trends in Uniform asset turns, slightly offset by weaker Uniform earnings margins.

Uniform turns fell from 2.2x in 2010 to 1.1x in 2012, before recovering to 1.5x in 2013 and subsequently contracting back to 1.2x in 2014. Thereafter, Uniform turns improved to 1.5x in 2015, before gradually fading to 1.0x in 2020.

Meanwhile, from 2010-2011, Uniform margins dropped from 11% to 9%. Then, Uniform margins rebounded to 11%-12% levels in 2013-2019, before dropping to 9% in 2020.

SUMMARY and D&L Industries, Inc. Tearsheet

As our Uniform Accounting tearsheet for D&L Industries (DNL:PHL) highlights, the company trades at a Uniform P/E of 23.4x, which is around the global corporate average of 24.0x but below its historical P/E of 29.5x.

High P/Es require high EPS growth to sustain them. In the case of D&L Industries, the company has recently shown a 27% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, D&L Industries’ sell-side analyst-driven forecast calls for a 42% and a 15% Uniform EPS growth in 2021 and 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify D&L Industries’ PHP 8.01 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 10% annually over the next three years. What sell-side analysts expect for D&L Industries’ earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 1x the long-run corporate average. Also, cash flows and cash on hand are slightly above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low dividend and credit risk.

Lastly, D&L Industries’ Uniform earnings growth is above peer averages in 2021, and the company is also trading above its peer average valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com