This company experimented on its research and development capabilities, achieving a Uniform ROA of 8%, not 7%

Given the increasing significance of innovation, companies that capitalize on their research and development efforts are often successful in their crafts. This is the case for this company. However, as-reported metrics show that it is only generating modest returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Last April, we highlighted that almost 80% of Philippine businesses are family-controlled firms. These include SM Investments Corporation (SM:PHL) and Ayala Corporation (AC:PHL).

Another one in this roster of successful family-controlled businesses is D&L Industries, Inc. (DNL:PHL), a manufacturer of specialty food ingredients and chemicals that started out selling colorants to the plastic industry in the 1960s.

Through its affiliates and subsidiaries, the firm was able to solidify its growth and product development plans by strengthening its investments in research and development.

Specifically, in 2018, D&L Industries aimed to grow its export business large enough to contribute half of the company’s revenues by 2025.

As of 2021, D&L Industries’ export business has risen by 62% to PHP 10.2 billion, accounting for 33% of total revenues. This is mainly due to the high global demand for coconut-based products under its food and oleochemicals subsidiary, which is reasonable during the pandemic because coconuts are known for their perceived natural antiviral, antibacterial, and antifungal properties.

That same year, the company was able to successfully attain the PHP 5 billion maiden bond offering, enabling it to financially secure its Batangas expansion plan.

Named First Industrial Township, the new plant will play a crucial role in the company’s future growth once it is finished, supporting efforts to create more innovative products like high-value coconut-based goods and enter new international markets.

As for its focus on developing products based on market needs, D&L Industries has already been known for being an innovation powerhouse in the Philippines as it continues to ramp up its R&D throughout the years.

As an example, one of its subsidiaries—Aero-pack—has successfully developed and launched Solbac® Surface Disinfectant within three months of product formulation during the pandemic.

In 2021, the company introduced its most recent innovation, Laurin CocoMCT®. This product is made of the healthiest part of coconut oil and is advised to be taken in order to boost a person’s immunity.

Due to these successful initiatives, total revenues jumped 42% to PHP 30.9 billion in 2021, as compared to PHP 21.7 billion in 2020. This, in turn, exhibits strong development potential in both the domestic and global markets as D&L Industries currently exports to 28 different countries and is looking to further expand through continuous research and development.

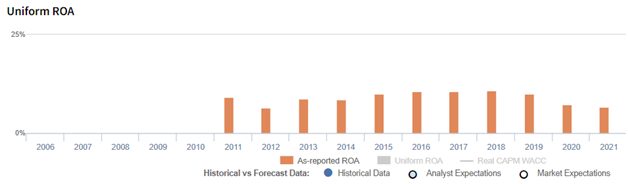

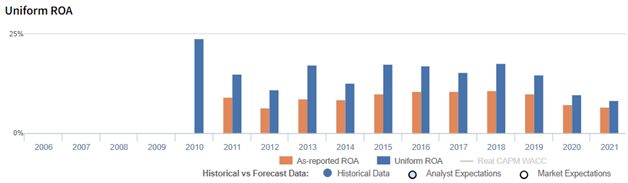

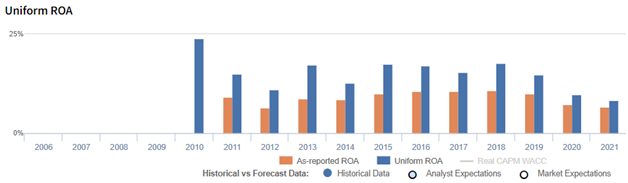

However, looking at as-reported metrics, it appears that D&L Industries is barely making a profit, with return on assets (ROAs) of just 7% in 2021.

In reality, Uniform Accounting shows that the company’s focus on its growth initiatives has generated better returns, with Uniform ROAs staying at a higher 8%.

One reason behind the distortion in the as-reported figures comes from the accounting treatment of goodwill. Since its acquisitions in 2014, D&L Industries has been recording PHP 3.4 billion worth of goodwill, representing 9% of its as-reported assets.

Goodwill is purely accounting-based and is not actually used in the company’s operations. This falsely inflates the asset base and makes D&L Industries appear to be a less profitable business.

If we remove PHP 3.4 billion goodwill from D&L Industries’ asset base and apply the many other necessary adjustments that Valens makes under Uniform Accounting, we arrive at a 8% Uniform ROA for 2021, greater than its 7% as-reported ROA.

D&L Industries’ earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think D&L Industries’ profitability has been weaker than real economic metrics have highlighted in the past eleven years.

Through Uniform Accounting, we can see that the company’s true ROAs have been understated. For example, as-reported ROA was 7% in 2021, but its Uniform ROA was higher at 8%.

D&L Industries’ Uniform asset turns are stronger than you think

For the past twelve years, as-reported metrics have understated D&L Industries’ asset turns, a key driver of profitability.

Moreover, since 2011, as-reported turns ranged from 0.5x-1.2x through 2021. Meanwhile, Uniform turns never went below 1.1x.

SUMMARY and D&L Industries, Inc. Tearsheet

As the Uniform Accounting tearsheet for D&L Industries (DNL:PHL) highlights, the company trades at a Uniform P/E of 25.3x, which is above the global corporate average of 18.4x, but below its historical P/E of 30.5x.

High P/Es require high EPS growth to sustain them. In the case of D&L Industries, the company has recently shown a 20% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, D&L Industries’ sell-side analyst-driven forecast calls for a 22% and a 23% Uniform EPS growth in 2022 and 2023, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify D&L Industries’ PHP 8.20 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 13% annually over the next three years. What sell-side analysts expect for D&L Industries’ earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power is 1x the long-run corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high dividend and credit risk.

Lastly, D&L Industries’ Uniform earnings growth is in line with peer averages in 2022, and the company is also trading in line with its peer average valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com